Man GLG Gets Bullish on Junk Bonds Pricing In Record Defaults

Man GLG Gets Bullish on Junk Bonds Pricing In Record Defaults

(Bloomberg) -- Oil has collapsed. The economy has shut down. And whole industries are out of business. But to the fund managers at Man GLG, the riskiest corporate debt has rarely looked so good.

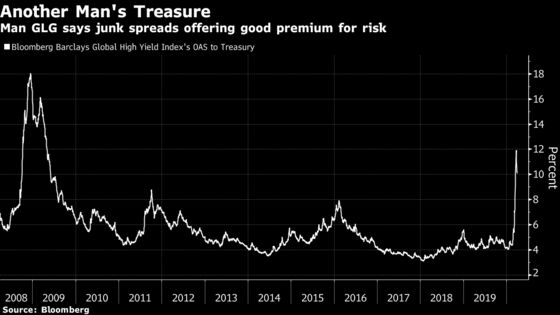

The $32 billion unit of the world’s largest listed hedge fund says junk bonds are pricing in a wave of defaults that beggars belief, even through a global recession.

“The market is now offering a rare value opportunity in HY,” fund manager Michael Scott and analyst Yves Blechner wrote in an April report. “We are now materially bullish on a longer-term horizon following the aggressive repricing of market spreads.”

Dollar junk bonds are implying a five-year cumulative default rate of more than 40% while those in euro are projecting 35%. That compares with the worst rate of 32% in all of history and a roughly 10% realized level expected by the GLG team.

“Spreads comfortably compensate investors for most, if not all, default rate outcomes,” they wrote.

Even after a Fed-induced risk rally cut that compensation by some 220 basis points, speculative-grade bonds in the U.S. pay average spreads of 880 basis points near financial-crisis levels. They’re even higher in a global index of sub-investment grade debt, at 1,000 basis points.

There are plenty reasons to shun junk credit now despite these valuations.

With the global economy shuttered to contain the spread of coronavirus, investors are fleeing corporate-debt funds across the spectrum to hunker in cash. Liquidity has proven unreliable in sell-offs.

Whole industries from retail to airlines are making almost no money with people forced to stay home.

But to Man GLG, it’s possible to be too bearish.

They acknowledge that a global recession will likely deliver a “large hit to corporate earnings,” but contend the shock will be short and sharp rather than deep and prolonged.

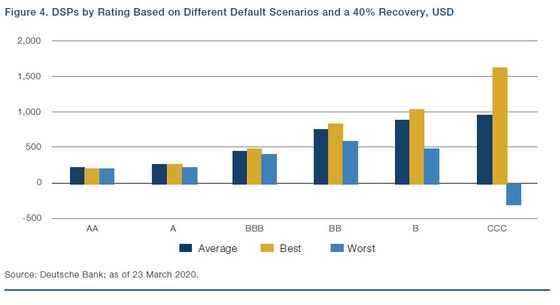

Based on a wide range of default scenarios, credit rated BB or B is offering a juicier reward than investment-grade counterparts. Even in the worst case where investors recover nothing, bonds rated B, BB or BBB still bear a premium.

And based on history, with spreads at current levels, high-yield bonds should return 15% over the next 12 months.

“Downside risks, in our view, should be limited from here,” Scott and Blechner said. “Even if we do encounter a deeper and more protracted recession than we expect, we think HY is already pricing in a substantial margin of safety and could be a cycle opportunity.”

©2020 Bloomberg L.P.