Looming U.S. Junk Bond Risk May Shrink With Fed’s Help

Looming U.S. Junk Bond Risk May Shrink With Fed’s Help

(Bloomberg) -- One of the biggest risks in the junk bond market is showing signs of diminishing, with help from the Federal Reserve.

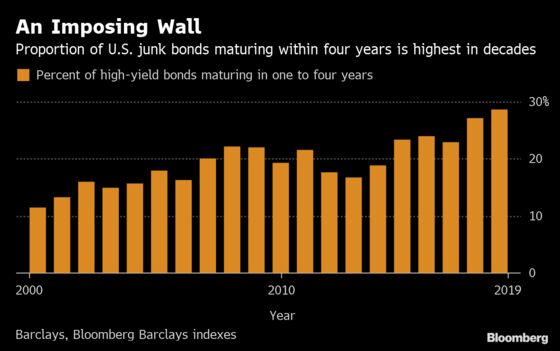

Nearly a third of the $1.2 trillion U.S. high-yield market matures in the next four years, a record high proportion, according to Barclays Plc strategists led by Bradley Rogoff. Junk-rated companies have to refinance that debt, pay it off, or face bankruptcy.

They have years to sort out that risk, but many are doing it now: companies have issued more than $80 billion of bonds this year that listed refinancing as one of the uses of proceeds, according to data compiled by Bloomberg, accounting for more than 70% of issuance this year.

“Companies are extending maturities out, and that’s healthy,” said Scott Roberts, head of high-yield debt at Invesco Ltd. Refinancing is a better use of debt than buying back shares, he added. “I’ve seen frothy before and this is not it.”

Corporations have ample incentive to deal with future debt maturities soon: on average they can reduce interest costs by issuing securities at current yields, the Barclays strategists said. Those relatively low borrowing costs are in part because of the Fed, which has paused its rate hikes, spurring money managers to pile into junk bonds in search of yield. Even with recent declines in high-yield securities, the debt has gained 8.3% this year through Friday, according to Bloomberg Barclays index data.

“I feel good about this high-yield market and we are trying to push issuers to take advantage of it,” said Richard Zogheb, global head of debt capital markets at Citigroup Inc. “Investors are so excited now that the underlying rate environment is more dovish, and that’s really good news for high-yield borrowers.”

Investment bankers say companies are taking notice of the opportunities to issue, and not just for refinancing. Corporations sold around $12 billion of U.S. junk bonds last week, the highest level in around 20 months, according to data compiled by Bloomberg. Sales in 2019 have risen by about 20% from the same time last year.

“We had half a dozen companies that were planning to go as early as nine or 10 months ago, then the market started weakening and we never got to the point where we could do those deals,” said John Gregory, head of leveraged-finance syndicate at Wells Fargo & Co., referring to when junk bond prices fell late last year. “Now we’re finally getting to that point.”

Three Reasons

There are at least three factors that can support refinancing activity now, according to the strategists at Barclays. First is the big wall of maturing bonds that companies face: about 29% of the index comes due in the next four years, well above the post-2000 average of 20%.

Second is that the current index yield is a little more than 6%, while in seven of the next eight years the weighted average coupon of maturing bonds is higher. The exception is 2020, a year in which only 3% of the index matures. And the third is refinancing activity tends to pick up in periods of lower yields, especially when the gap between short- and longer-term yields is relatively narrow, known as a flat yield curve.

Last week, high-yield companies weren’t deterred from issuing by trade war talk and the resulting slumping equities. On Thursday for example, Bausch Health Cos. sold $1.5 billion of notes maturing in 2028 and 2029, planning to use proceeds to buy back notes due in 2023. Talen Energy sold $750 million of notes due 2027, and plans to use the money raised to buy back notes maturing through 2024. On Tuesday alone, companies sold $5.4 billion of bonds.

“I can’t remember when $5 billion worth of deals came in one day,” said Matt Eagan, a portfolio manager at Loomis Sayles & Co.

Demand has been strong enough for junk bonds that companies have been borrowing in that market instead of leveraged loans. With the Fed on hold, demand for floating-rate debt like bonds has been waning. Investors have been pulling money from loan funds for 25 weeks, but have added to their junk bond funds for much of the year, according to Lipper data.

Bankers are telling companies to take notice.

“The market is generally wide open for issuers,” said Jenny Lee, co-head of leveraged loan and high-yield capital markets at JPMorgan Chase & Co. “We’re advising issuer clients to look harder at doing high-yield bonds.”

--With assistance from Boris Korby.

To contact the reporter on this story: Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Dawn McCarty

©2019 Bloomberg L.P.