Longtime Bond Bull Hoisington Sees MMT as a Risk for Treasuries

Longtime Bond Bull Hoisington Sees MMT as a Risk for Treasuries

(Bloomberg) -- Hoisington Investment Management Co., famous for its bullish view on Treasuries over the past three decades, is warning about potential risks to bonds if the Federal Reserve follows in the footsteps of other central banks that fund government deficits.

Should the Fed undertake an array of measures that some peers have begun in an attempt to boost growth, it “would bring a rising inflationary dynamic into the picture” that “would make Treasury bills and inflation-adjusted Treasury securities far more preferable compared to longer dated Treasury bonds,” the Austin, Texas-based company said in a quarterly letter to clients.

The measures include, but aren’t limited to, Modern Monetary Theory, or MMT, Hoisington’s chief economist Lacy Hunt said in an interview Friday. Generally, he said, they are forms of “monetary financing” in which governments run deficits without issuing bonds, by authorizing their central banks to pay the bills. The U.K. and New Zealand have taken steps in that direction by temporarily increasing overdraft limits at their central banks. Historical precedents also include Weimar Germany a century ago and China in the 1930s, Hunt said.

Such a change isn’t likely to occur under the current leadership since Fed Chair Jerome Powell has repeated the mantra that the central bank’s powers are limited to lending, not spending. Still, “it’s a risk that’s entered the system, and is clearly rising because it’s going to become increasingly clear that borrowing more and spending it will not work,” Hunt said.

“If the Fed’s liabilities were made a medium of exchange,” Hoisington’s third-quarter report to clients said, “the inflation rate would rise and inflationary expectations would move ahead of actual inflation,” unleashing a surge in demand. “That would be a major game-changer,” Hunt said.

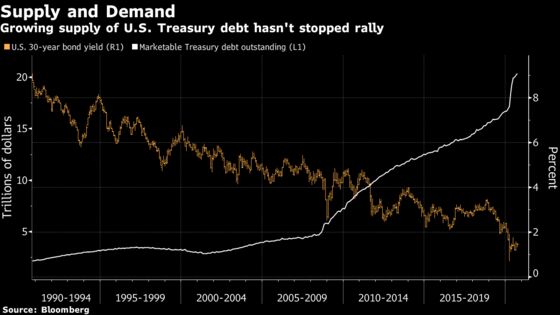

For years, Hoisington’s quarterly letters have served up variations on the contrarian -- and largely correct -- view that inflation and long-term U.S. yields were likely to continue to decline despite an increasing supply of Treasury securities, because high debt levels are a drag on economic growth.

While they’ve acknowledged developments that could temporarily interrupt the bull market that drove the 30-year bond’s yield to a record low of 0.70% in March from more than 9% in 1990, “I don’t think we’ve ever spelled out the tail risks in a fashion that we did in this letter,” Hunt said.

Hoisington manages about $5 billion in Treasuries, including the Wasatch-Hoisington Treasury Fund, which has returned 21% this year, more than any other actively-managed U.S. government bond fund, according to Bloomberg data. It’s had an annual average return of 8.2% since its 1986 inception.

Bearing the name of its chief executive officer and founder Van R. Hoisington, the company strives to outperform by predicting the direction of interest rates, a strategy many other bond managers avoid in favor of lower-risk gambles. Its bullish stance since 1990 has meant that the funds hold a changing mix of regular Treasury securities and STRIPS, which are zero-coupon bonds that deliver maximum interest-rate risk.

A shift to bills -- cash equivalents with almost no interest-rate risk -- and Treasury inflation-protected securities would be a new chapter for the firm’s main strategy, which hasn’t used bills since the late 1980s and has never included TIPS, Hunt said. TIPS debuted in 1997.

“There’s a possibility the rules of the game are changing,” he said. “We wanted to alert our clients we’re aware the rules are changing and we’d be responsive.”

©2020 Bloomberg L.P.