Longer Is Better in Emerging-Market Bonds in Low-Rate World

Longer Is Better in Emerging-Market Bonds in Low-Rate World

(Bloomberg) -- As the global bond rally intensifies, buying up emerging market long-duration debt is proving to be a winning strategy.

The reason is simple. The greater the duration, the greater the sensitivity to interest rates which are falling across the world as global central banks join the Federal Reserve in their dovish stance. That extra profit is important in a world where the stockpile of negative-yielding debt has risen 53% this year to about $13 trillion, according to a Bloomberg Barclays index.

“It makes sense to take duration risks in this backdrop,” said Eugene Leow, a fixed-income strategist at DBS Group Holdings Ltd. in Singapore. “Emerging markets offer high nominal and real yields and look especially attractive in the yield-starved world.”

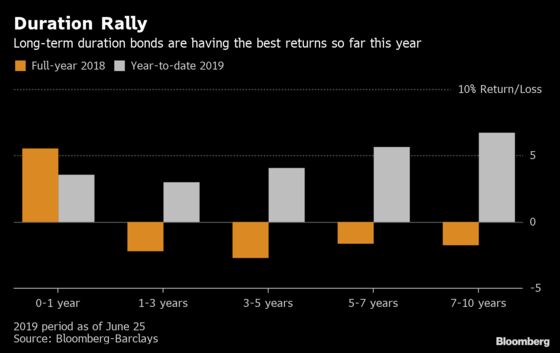

Holding unhedged emerging-market local bonds with a duration of seven to 10 years has handed investors a return of 6.7% in dollars this year, compared with 3.5% for 0-1 year equivalents, according to a Bloomberg Barclays index. That’s a turnaround from last year when the higher duration basket fell 1.7% as yields climbed and the Federal Reserve raised rates four times.

Securities with longer duration typically gain more when rates drop. Conversely, they suffer stiffer losses when they climb.

It’s not just in the emerging-market world that long-duration bonds are attracting investors. Dovish monetary bets, relentless demand for safe assets and conviction the lowflation era will last are spurring money managers worldwide to gorge on long-maturity bonds, or duration risk.

Trend

For Pictet Asset Management, the trend for longer-duration bonds will probably continue as it’s “less optimistic” about a sharp turnaround in growth and the Fed is unlikely to re-embark on a tightening cycle, according to London-based head of EM local-currency debt Alper Gocer.

“In EMs, we believe there is scope for policy to be adjusted to the reality of slower growth and inflation,” he said. Pictet has looked at investment opportunities in Russia, Mexico and Indonesia, and Gocer began to move to an overweight duration position in late 2018, he said.

Emso Asset Management extended its duration exposure around April and May, in particular in Central Europe, according to Jens Nystedt, a senior portfolio manager in New York. The $6 billion emerging-market focused investment manager sees opportunity in local bonds where exchange rates are still weak relative to fundamentals such as Brazil, Argentina, Indonesia, and possibly Turkey, he said.

“In such a world with decent global growth, a Fed modestly easing and capped U.S. Treasury yields, those EM assets that underperformed in the duration rally can outperform significantly,” Nystedt said. “Those assets are predominantly sovereign high yield and select EM currencies.”

Israel is seeking to tap investor appetite for long-duration bonds, selling debt maturing in 50 years for the first time.

The spread on emerging-market sovereign dollar bonds with maturities of over 10 years were headed to a 30 basis point tightening in June, reversing the widening seen during the May selloff.

Risks

The major risk to the duration rally, some investors say, is that central banks in developing economies don’t meet investor expectations for easing. If rate cuts fall short of what is anticipated, yields could go up, trimming gains from long-duration positions.

“The risk is that market prices already reflect a material easing to come,” said Steven Oh, head of fixed income at PineBridge Investments in Los Angeles. “And to the extent that central banks ultimately deliver much less than what is being priced, the yield curve may move upward from current levels.”

Bertrand Delgado, a strategist at Societe Generale SA in New York, says duration is likely to continue playing out well in the near term, driven by easing global rates. But when global rates stabilize, performance should be more mixed as it moves to reflect country-specific issues and the risks of a U.S. slowdown.

“Enjoy the party while it lasts until we get into the recession risks mode in the U.S., most likely by year-end or early 2020,” he said.

--With assistance from Anchalee Worrachate, Liz Capo McCormick and Netty Ismail.

To contact the reporters on this story: Lilian Karunungan in Singapore at lkarunungan@bloomberg.net;Aline Oyamada in Sao Paulo at aoyamada3@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, Philip Sanders, Cormac Mullen

©2019 Bloomberg L.P.