Yield Plunge Stirs Thoughts of 1% Treasuries on Delta Variant

Delta variant's spread sees long-term U.S. Treasury yields spiral lower amid economic-growth concerns

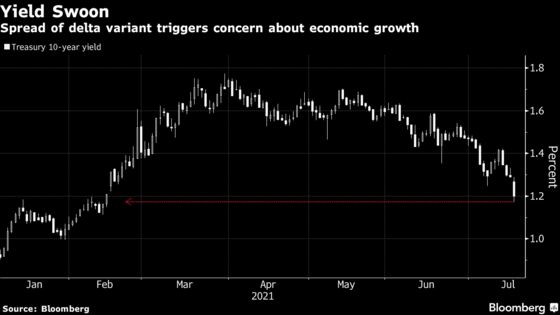

(Bloomberg) -- Long-term Treasury rates tumbled to the lowest levels in months on Monday as the spread of the delta coronavirus variant called into question optimistic assumptions about economic recovery, also touching off a global stock market slump.

Market-implied expectations for a Federal Reserve rate increase were pushed further into the future amid stronger-than-normal debt-market volumes, and the rally in bonds drove benchmark 10-year yields down as much as 12 basis points to 1.17% on Monday. That’s a level unseen since early February and well below the 14-month high of 1.77% it reached in March. Some traders are now likely to begin looking toward 1%, a mark that hasn’t been breached since late January.

The resurgence of virus cases despite widespread vaccination induced investors to dial back risk-taking, anticipating a fresh wave of restrictions on economic activity. The 10-year rate ended below its 200-day moving average for the first time since November, while the 30-year yield also hit a five-month nadir and the gap between two- and 10-year yields narrowed to less than 100 basis points for the first time since February.

The latest wave of demand for Treasuries is based on “the forward-looking reemergence of Covid risks coupled with both fiscal and monetary policy that can’t step up as aggressively,” said Stefan Dannibale, head of U.S. Treasury trading and sales at StoneX Group Inc. “The market is looking at those challenges and re-rating growth lower ahead.”

The move started in Asia with rising cases fueling speculation that a lockdown in Sydney could be extended, providing a lift for domestic bonds. Moves unfolded further in European trading hours, before gathering pace when the U.S. session day began, accompanied by heavy volume in Treasury futures. By 3 p.m. in New York, volume in the 10-year note contract was near 2 million, compared with a daily average of 1.55 million over the past 30 days. Bonds were little changed during the Asian session on Tuesday.

“Even if we do get through this latest growth scare for well vaccination countries, going forward it will still be a different story for non-vaccination countries, so even if in vaccinated nations the concerns pass, in others it will not,” NatWest Markets’ global head of desk strategy John Briggs wrote in a client note.

However, the bond rally also draw strengths from widespread positioning for an inflationary economic recovery, traders and strategists said. Such positioning has been unprofitable since the end of March, and mounting losses are said to have driven people to take them off.

“The best explanation for recent price action in Treasuries is positioning and flows, rather than any fundamental change in the outlook for the economy,” Morgan Stanley strategist Guneet Dhingra said in a July 16 report.

| Related Stories |

|---|

Treasury Strategists Pin Rally on Positioning: Research Roundup Spiraling Treasury Yields Poised to Roil Tranquil Credit Markets Traders Voice Fresh Covid Worry: ‘The Broad Public Is Waking Up’ U.S. Futures Surge Suggests Capitulation as Fed-Hike Bets Dumped |

“Given the momentum in the market, it’s not apparent to me that trade has exhausted itself,” StoneX’s Dannibale said.

The plunge in 10-year yields Monday was the biggest intra-day drop since a sharp decline on Feb. 26 -- a move that followed a rout in prices the previous day.

With the 10-year nominal rate breaking the 1.21%-1.22% area, it will likely continue to about 1.05%, Tony Rodriguez, head of fixed income strategy at Nuveen, said on Bloomberg television.

“The global central banks are going to continue to be uber-dovish,” Rodriguez said.

Money-market derivative traders pushed out to March 2023 when they foresee the Fed lifting its near zero policy rate, from about January of that year on Friday. A second hike is now expected around September 2024. With short-term Treasury yields constrained from falling by proximity to the Fed’s target, the curve flattened, narrowing the gap between 5- and 30-year yields to 110 basis points, the smallest in a month.

The European Central Bank will meet on Thursday. Policy makers are expected to tweak forward guidance following the strategy review outcome this month, while decisions on future bond-buying are anticipated to be left until the economic outlook clears, according to a Bloomberg survey of economists.

Ten-year Treasury yields stripped of inflationary effects slid Monday amid growing concerns about economic growth and as share prices tumbled. So called real-yields are viewed as a more pure bond-market gauge of the pace of future economic growth. The yield on the 10-year Treasury inflation-protected security fell 6 basis points to about minus 1.11%.

“The economic outlook brings uncertainty with respect to both growth and inflation,” BMO strategist Dan Krieter wrote in a note.

©2021 Bloomberg L.P.