Past Debts Come Due for U.S. Stocks as Credit Stress Swells

The sell-off in equities has deepened after the biggest weekly deterioration in U.S. investment grade spreads since 2016.

(Bloomberg) -- The stock market has a debt problem.

Drill into the S&P 500 and it’s evident that the swoon that began in September isn’t just a tale of formerly high-flying tech heavyweights cast down. Equally, it’s a story of highly levered firms sinking under the weight of their debts.

The sell-off in equities has deepened after the biggest weekly deterioration in U.S. investment grade spreads since 2016 and the longest losing streak for high-yield debt in more than a year. More and more, stocks and bonds are both being whipped around by creeping concern about the creditworthiness of American businesses as the expansion grows ever longer and credit conditions tighten.

“The recent rise in SPX beta to credit spread suggests equity investors are finally awakening to its implication,” writes Rebecca Cheong, head of equity derivatives strategy at UBS Securities. “The S&P 500 has more room to fall on the back of the current weak credit market.”

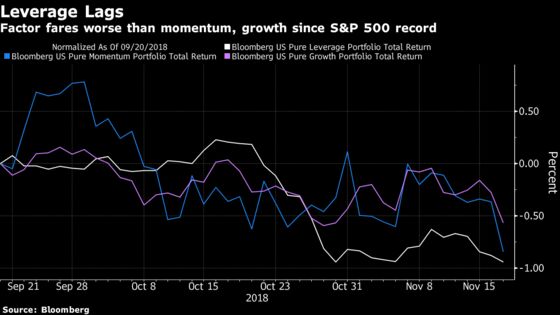

Since the September all-time high in U.S. stocks, a portfolio of companies with the most leverage has fared even worse than momentum shares, the group usually identified as ground zero of the meltdown. The factor is heading for its eighth consecutive negative quarter and closed at its lowest level since 2009 on Monday.

Under the hood, the sorting effect in equities is evident. Since the S&P 500 peaked in September, shares of AAA-rated and AA-rated companies have held up much better than their less creditworthy peers. A basket of stocks compiled by Goldman Sachs with strong balance sheets is also still up 2 percent year-to-date, besting a group of competitors with weaker financials by more than five percentage points.

“Over time, these volatility shocks may heighten concern over an asset class sought out, and still priced, for its purported safety,” said Daniel Sorid of Citigroup Global Markets. “Hedge funds will increasingly challenge the disconnect that has emerged between leverage and credit ratings, and we think the market is less prepared for this scrutiny of issuers with at least one BBB+ or higher rating.”

For corporate executives, it’s all about avoiding General Electric’s fate. Shares of the once-mighty conglomerate have fallen more than 50 percent this year. Its bonds are already trading like they’re junk-rated, with Chief Executive Officer Larry Culp citing a “sense of urgency” in cutting debt and selling assets.

Rising rates coupled with a slowdown in global growth have changed the calculus of what investors are looking for in a prospective stock.

“We’ve kind of shifted from the eighth or ninth inning of this game, where companies are able to use their balance sheet to enhance shareholder returns, and we’re starting to shift maybe to the first inning where some of the weaker companies, companies under a little bit more pressure, actually have to take care of their balance sheet to protect shareholders,” Peter Tchir, head of Macro Strategy at Academy Securities, said in an interview on Bloomberg TV. “We’ve seen a shift in psychology that will see reduced leverage just naturally occurring.”

There are many signs that corporates are getting proactive in a bid to avoid the same treatment GE got from credit traders, Tchir added. Even if those steps might not be so shareholder-friendly in the short term.

Comcast CEO Brian Roberts said his company’s “plate is full” following the acquisition of Sky Plc, and that it will be “pausing the share buyback and focusing on the balance sheet.”

Anheuser-Bush InBev announced plans to repurchase up to $2.5 billion in debt after halving its dividend. Newell Brands bought back some of its debt in October, too.

Sorting Hat

Christopher Harvey, head of equity strategy at Wells Fargo Securities, highlighted net debt to a measure of operating earnings as an important variable for relative equity performance in 2018.

“As credit spreads widen, we would expect debt-laden companies to underperform, partly because they’re reliant on capital markets and also there’s a repricing of that type of risk,” he said in a telephone interview. “Traditionally, higher quality outperforms in that kind of environment.”

The strategist suggested that smaller-cap energy companies as well as California-based utilities were pockets of acute credit stress, and that the damage in industrials was very idiosyncratic.

The good news: For companies that have been able to access the bond market, time is mostly on their side. Less than 0.5 percent of debt in U.S. investment grade and high-yield indexes comes due over the next 12 months.

Small-cap companies don’t share that same good fortune. Not only does this group have higher net indebtedness, as Citigroup chief U.S. equity strategist Tobias Levkovich highlighted, but a higher share of their obligations are floating-rate, translating into higher servicing costs more quickly.

“Russell 2000 net debt/Ebitda is at rather elevated levels,” according to David Bianco, Americas chief investment officer at Deutsche Asset Management. “84 percent of the Russell 2000 with a credit rating is junk-rated.”

--With assistance from Sebastian Boyd.

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Andrew Dunn, Chris Nagi

©2018 Bloomberg L.P.