LME's Copper Dominance Tested as Rivals' Options Trading Jumps

LME's Copper Dominance Tested as Rivals' Options Trading Jumps

(Bloomberg) -- Metals bourses trying to muscle into a copper market dominated by the LME are getting a helping hand from options.

As is the case for copper futures, the London Metal Exchange has been the go-to marketplace for options since starting them decades ago. While the bourse is by far still the biggest venue for trading the products, competition is rising. Options volumes have jumped almost 10-fold on Comex in New York since January 2017 and trading got off to a fast start in Shanghai last month.

Rival bourses have found it easier to lure new investors attracted by rebounding prices in recent years, partly because of simpler monthly structures for contracts, LME chief Matthew Chamberlain said. Options offer a cheaper way to bet on metals than trading futures, and Comex contracts are also proving popular with investors already familiar with owner CME Group Inc.’s products spanning interest rates, equities, currencies and commodities.

“Comex is becoming more and more relevant for copper options,” Francois Combes, head of metals at Societe Generale SA, said in an interview in London. “For pricing and hedging, you can’t ignore what is happening.”

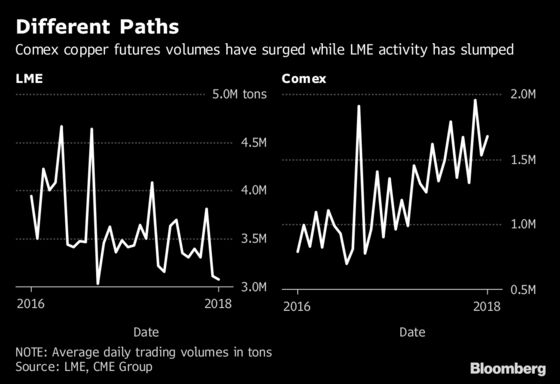

While Comex options trading is still tiny compared with the LME, the recent growth is bolstering CME’s campaign to grab a greater share of the global market. Copper futures volumes have also climbed on the New York bourse in the past few years and stockpiles at its depots swelled, closing the gap with LME inventories.

Market Interest

“Four years ago, when we set out to boost our presence in the copper market, we put a lot of focus initially on futures, because we knew that if we wanted to build our standing in the physical market, that’s where we needed to start,” said Young-Jin Chang, global head of metals products at CME. “Over the past two years, the copper options contract has been on an amazing journey too.”

That’s happened as activity on the LME slowed as users revolted over high fees. Under former chief executive officer, Garry Jones, the LME used a raft of incentives to lure high-frequency traders that are more active on rival bourses. But criticism from the LME’s traditional users prompted his successor to switch back to a path more aligned with the needs of the physical industry.

“Somebody who wants to go and put on copper trades for the first time, who trades in other commodities and asset classes, is probably not going to trade with us, because we’re not the market that’s the most easy for them,” Chamberlain said in an interview.

Still, options may help the LME attract new users and boost volumes, Chamberlain said, adding that the bourse will work on developing those products next year to make them more appealing.

“Unlike the futures market, where I don’t think there’s much we could do without angering as many people as we advantaged, with options I think there are some quite easy wins that would benefit everyone,” he said.

It’s looking good early on for Shanghai Futures Exchange options. More than 57,000 metric tons of contracts changed hands on average in the first five days after trading started Sept. 21. That’s more than double September’s daily average on Comex and about a quarter of the amount dealt each day on the LME.

Industrial firms and investment funds in top copper user China have so far been highly active users of LME options contracts, but the SHFE’s foray into that market poses a challenge to the LME’s dominance, said Keith Wildie, head of commodities volatility at Vantage Capital Markets Ltd.

--With assistance from Martin Ritchie.

To contact the reporters on this story: Mark Burton in London at mburton51@bloomberg.net;Jack Farchy in London at jfarchy@bloomberg.net

To contact the editors responsible for this story: Lynn Thomasson at lthomasson@bloomberg.net, Nicholas Larkin, Dylan Griffiths

©2018 Bloomberg L.P.