Liquidity Risk Debate Pits CrossBorder Against JPMorgan, Goldman

Liquidity Risk Debate Pits CrossBorder Against JPMorgan, Goldman

(Bloomberg) -- JPMorgan Chase & Co. and Goldman Sachs Group Inc. are among those expressing concerns about market liquidity. Investment research firm CrossBorder Capital Ltd. sees a more reassuring scenario.

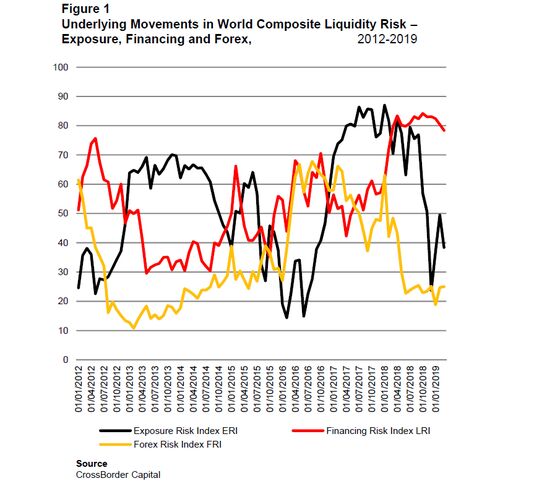

“Liquidity risks over the next six to 12 months continue to fall away, according to our latest assessment from a deep dive into global liquidity data,” the London-based firm that tracks global capital flows wrote in a recent note. “The three factors we closely watch: exposure risk, financing risk and forex risk, appear to have already peaked or at least are in the process of peaking.”

CrossBorder’s report comes after a stream of concerns expressed about the impact of falling liquidity. Goldman strategists have said it may be responsible for the dislocation between equity volatility and economic fundamentals, while JPMorgan’s Marko Kolanovic said a volatility-liquidity loop can create “violent” markets. Morgan Stanley’s Andrew Sheets cited low liquidity as potentially exacerbating any sell-offs, in a recent interview.

While financing risk still seems elevated, it appears to have peaked amid signs that some major central banks are about to re-start quantitative easing policies, the CrossBorder report said.

The research firm favors a risk-on approach from investors, with the caveat that central banks must return to a “permanent state” of QE, it said. While the latter “is a big ask,” it is “dictated by the changed nature of the financial system,” according to CrossBorder.

Investors should hedge high equity and corporate-bond exposure with securities with greater convexity, a measure of sensitivity to interest rate changes, according to the firm.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Andreea Papuc, Cormac Mullen

©2019 Bloomberg L.P.