Liquidity Fears Have the Likes of Pimco Sheltering in Credit Swaps

Liquidity Fears Have the Likes of Pimco Sheltering in Credit Swaps

(Bloomberg) -- In the worst year for global credit in a decade, nimble-footed traders like Dan Ivascyn are boosting defenses against an imminent liquidity crunch.

The group chief investment officer of Pacific Investment Management Co. said he’s turning to credit-default swaps to stay flexible “as market conditions change.” He’s among U.S. investors who’ve pushed CDS trading volumes up 43 percent while bond turnover stagnates. In Europe, credit derivatives trading has surged 22 percent this year through November while trading of corporate notes slipped 5 percent, based on data from MarketAxess.

“Some of these diversified indexes that trade out there in the marketplace can typically offer liquidity up to 20 times greater than a portfolio of cash bonds,” Ivascyn said in an interview for Bloomberg Radio. “If we’re expressing a view on credit spreads more broadly in a portfolio, we try to do that in the most liquid way possible.”

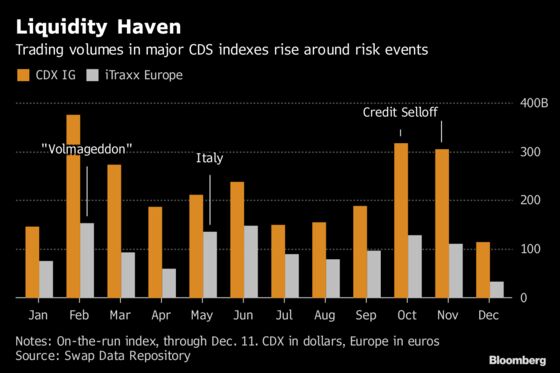

Trading of CDS -- both indexes and single-name contracts -- has jumped because it is easier to buy and sell standardized swaps rather than finding a buyer for one of thousands of corporate bonds all offering different terms, risks and maturities. That flexibility has become even more prized as investors face annual losses in investment-grade and high-yield bonds on both sides of the Atlantic.

“People’s reaction is to reach for CDS when they’re looking to put on more defensive positions,” said Alex Eventon, a fund manager at Resco Asset Management who favors the swaps for his absolute-return strategy. “Long-only and buy-and-hold strategies just haven’t been as lucrative as they have in prior years.”

A string of credit-market blow-ups this year has highlighted how difficult it can be to trade bonds in a crisis. Liquidity in General Electric Co. debt -- as measured by the bid-ask spread -- shrank as the industrial icon scrambled to sell assets to cope with debt of more than $100 billion. The gap between bid and ask prices for Italian bank bonds similarly blew out this year as the populist government challenges EU budget rules.

Such difficulties have helped fan a 10 percent jump this year in global trading of credit-default swaps on individual companies and governments, based on the latest data from the International Swaps & Derivatives Association. It showed average weekly trading of $52 billion as of Nov. 2.

Basis Trades

“There’s more liquidity in single-name credit swaps than there has been in years,” said Luke Hickmore, a senior investment manager at Aberdeen Standard Investments, the U.K.’s largest active fund firm. “They’re especially useful when there are dislocations in the market.”

Hickmore has been adding CDS exposure, including through basis trades --- a way of arbitraging the difference between bonds and credit swaps -- on Heathrow Airport and engineering firm GKN.

Credit risks are growing globally because central banks are tightening monetary conditions and ending years of easy money that boosted corporate bonds almost uniformly. The Federal Reserve has raised borrowing costs in the U.S., while the European Central Bank may lift rates in the second half of 2019. The ECB confirmed yesterday it will stop buying new bonds this month, though it will continue to reinvest maturing debt “for an extended period of time.”

“The peak of trading activity in CDS indexes is when you have risk events,” said Olivier Debat, senior investment specialist at Union Bancaire Privee SA. His global high-yield fund holds no corporate bonds and takes all its credit exposure through CDS indexes.

Still, investors aren’t snubbing cash-bond trading altogether. This year’s volume drop is partly due to new-bond sales cooling off after a hectic 2017. That slowdown means investors have less need to sell old notes to make room for new investments.

Even if primary sales do pick up, CDS may still have an edge in terms of ease of trading. That’s one reason why Hermes Investment Management uses “a lot of derivatives” among its 36 billion pounds ($46 billion) of assets, according to Fraser Lundie, its co-head of credit.

“If you’ve got a mandate that only allows you to buy bonds, you’re going to miss out on a lot of liquidity in the credit market,” he said.

--With assistance from Samuel Potter.

To contact the reporters on this story: Tasos Vossos in London at tvossos@bloomberg.net;Katie Linsell in London at klinsell@bloomberg.net;Lisa Abramowicz in New York at labramowicz@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Cecile Gutscher, Neil Denslow

©2018 Bloomberg L.P.