Liquidity Breakdown Is Biggest Fear in JPMorgan Quant Survey

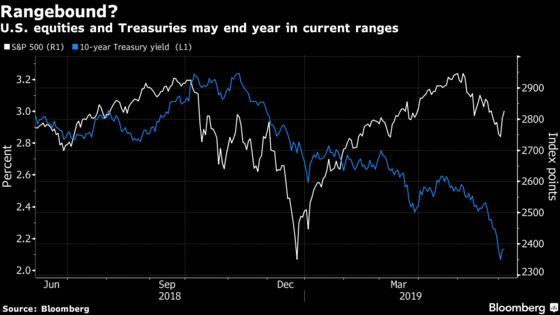

About 59% of those answering saw the 10-year Treasury yield between 2.0%-2.5% at year-end

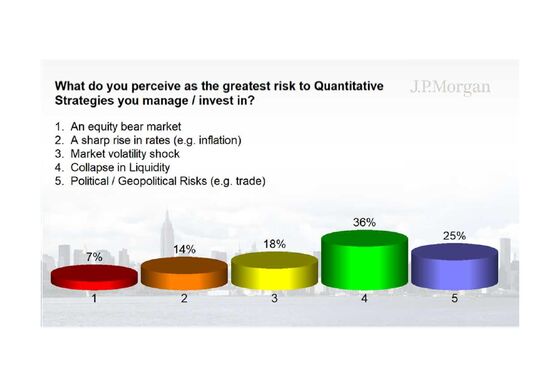

(Bloomberg) -- The greatest risk to quantitative strategies wouldn’t be an equity-bear market or a sharp increase in rates. It would be a collapse in liquidity.

That’s the result from a survey of investors at JPMorgan Chase & Co.’s U.S. Macro Quantitative and Derivatives Conference in New York on May 17, with 36% of respondents picking a liquidity plunge and 25% fearing political or geopolitical risks most, according to the conference summary from strategists Marko Kolanovic and Dubravko Lakos-Bujas.

About 59% of those answering saw the 10-year Treasury yield between 2.0%-2.5% at year-end, while 39% expected the S&P 500 between 2,800 and 3,000. A full 23% expect the next recession after 2021, though 33% see it in 2020 and 37% in 2021.

In terms of which quantitative approach has the best outlook, 27% of respondents said it was Equity Multi-Factors, with 22% choosing Statistical Arbitrage/High-Frequency, according to the survey of conference attendees that garnered between 150 and 270 responses per question.

“People remain quite positive on the outlook for quant investing,” Lakos-Bujas said in an interview May 30.

There were other discussions in addition to the survey, including a study showing that market-maker profitability may predict the subsequent month’s liquidity and volatility, as well as the trend lower in liquidity overall in recent years.

“People know this is happening,” Kolanovic said in an interview about the decline in liquidity. “It’s not just a theory.”

Meanwhile, about 80% of attendees responding to questions about volatility targeting said they do employ that method. And when surveyed about signals based on alternative data and machine learning that participants had researched, 59% of the conference’s respondents said none were actually yielding alpha, or excess returns. And 31% said between one and three did.

“It’s not easy to identify sources of alpha, but it’s the future,” Lakos-Bujas said.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Dave Liedtka, Rita Nazareth

©2019 Bloomberg L.P.