Lilley's New Hedge Fund Bets on U.S. Metals After Red Kite Split

Lilley Bets on U.S. Metals Revival After Splitting From Red Kite

(Bloomberg) -- For the past three decades, David Lilley has been one half of the best-known trading duo in global metals markets. Now he’s branching out alone, with bets on a revival of two unloved corners of the industry: the U.S. manufacturing sector and specialist commodity hedge funds.

In a wide-ranging interview with Bloomberg News, Lilley for the first time publicly explained why he split with long-time business partner Michael Farmer a year ago.

He set out his plans to build a new metals empire, investing in U.S. copper plants that make everything from heating units to trombone slides. He’s also hiring traders for a new hedge fund, Drakewood Capital Management.

“Hopefully we’ll get active at the same time the markets get active,” Lilley said of Drakewood. “I think we’re coming into a period where the markets are going to be a lot more helpful, in terms of the role that fundamentals like inventories will play.”

God Squad

The Lilley-Farmer team has been a fixture of metal markets for more than 30 years, starting at commodities merchants Philipp Brothers and Metallgesellschaft, at the time the world’s largest copper-trading company. The two went on to found hedge fund Red Kite together with Oskar Lewnowski in 2005, and soon became known both for their aggressive bets on the London Metal Exchange -- the fund returned 188 percent in 2006 -- and their evangelical Christianity, acquiring the nickname “the God squad.”

Lilley says he remains on good terms with Red Kite, and they’re still contesting a high-profile lawsuit into alleged market manipulation against Barclays Plc together. The split came about primarily because Farmer -- now Baron Farmer of Bishopsgate -- didn’t share Lilley’s enthusiasm for investing in downstream industrial assets, he said.

"Michael remains a much-respected friend, but we wanted to drive the business in different ways," he said.

Drakewood, which is awaiting full regulatory approval, is running investments carried over from Red Kite and recruiting traders from rival funds and banks, Lilley said.

Within the past few months, Lilley has hired former Macquarie Group Ltd. and BHP Billiton Ltd. ferrous metals trader Joel Parsons, and Tim Watkin, who joins from Ruffer LLP to cover base metals strategy and mining equities. Greg Buechele, who has traded precious and base metals at Carlyle Commodity Management and Balyasny Asset Management, has also joined as a consultant.

Fundamentals Return

The appointments come as Lilley positions Drakewood to profit from an expected resurgence in volatility as fundamentals return to the fore in metals markets, having been buffeted this year by macroeconomic anxiety over the U.S.-China trade war.

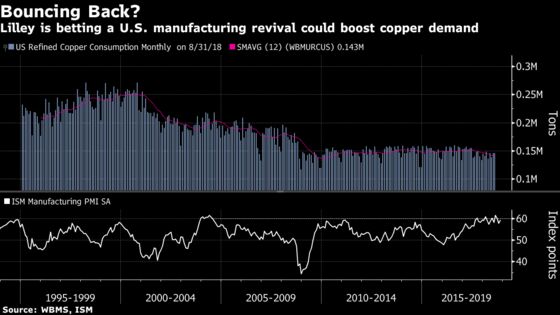

Lilley is also investing in the physical copper industry. Last month he teamed up with fellow fund manager Dwight Anderson to buy a copper and aluminum tubing business in the U.S., betting that the fortunes of such companies could get a boost from a revival in the country’s manufacturing sector.

On the surface, his two-pronged approach looks similar to the way Red Kite traded metal in its early years. Lilley and Farmer took big and often contrarian bets in futures markets that were informed by the real-time snapshot of global copper demand available to Red Kite as one of the world’s largest physical metals traders.

Chinese Adventure

In their first year of operation, that approach pitted Red Kite against the Chinese government. The fund wagered that the country would be forced to buy large volumes of copper to cover wrong-way bets by a rogue government trader. Having ridden prices to a record high, Red Kite doubled its money the next year by shorting copper on the view that the market had spiked too far.

But Lilley notes that the markets have changed a lot since then. While Red Kite still trades physical copper into China, Lilley is less convinced of the value of doing so in an industry where supply-and-demand data is widely available and macroeconomic and algorithmic investors are more influential.

"It’s a very competitive market and it’s hard to say that there’s a whole heap of money to be picked up there, in the way that there was when the market was new and dynamic,” he said.

U.S. Revival

The main rationale for investing in the U.S. plants is that they look primed to benefit from the country’s manufacturing revival, having survived a torrid period marked by overproduction and shrinking demand.

“These are companies that have been keeping belts tight and focusing hard on the bottom line, so you’re not buying into over-exuberant companies with corporate jets,” he said. The investment would make sense even if the U.S. suffers a recession in the next five years, he said, and the pair of investors might ultimately look to float it in an initial public offering.

Having an up-to-the-minute insight into copper usage trends continues to offer advantages.

“The real-time insight into how the U.S. is doing is certainly very valuable,” he said. “Demand is still very good, and you might expect it would be worse if you just looked at the newspapers.”

To contact the reporters on this story: Mark Burton in London at mburton51@bloomberg.net;Jack Farchy in London at jfarchy@bloomberg.net

To contact the editors responsible for this story: Lynn Thomasson at lthomasson@bloomberg.net, Alex Devine, Dylan Griffiths

©2018 Bloomberg L.P.