Libor Proving Hard to Kill in $200 Trillion Derivatives Market

It’s one of the most confounding questions facing regulators in the fight to phase out the London interbank offered rate.

(Bloomberg) -- It’s one of the most confounding questions facing regulators in the fight to phase out the London interbank offered rate.

How do you wean everyone from asset managers and traders to corporate treasurers off derivatives that are so ubiquitous, they’ve become part of the fabric of the financial system?

For the better part of three years, U.S. officials have been preaching patience. Libor-based interest-rate swaps, futures and options, among the most liquid markets in the world, would gradually give way to new securities tied to new benchmarks, they said, including the Secured Overnight Financing Rate, dollar Libor’s anointed successor.

Yet activity in those markets isn’t disappearing. What’s more, acceptance of alternative products has been slow. While some headway has been made, average open interest in three-month SOFR futures barely topped 5% that of eurodollar contracts last month. And recent high-profile milestones in the Libor transition that were expected to jump-start trading in the new instruments have delivered relatively modest boosts so far.

As the Federal Reserve’s year-end deadline to halt new Libor contracts creeps closer, some are beginning to express concern that the slow pace of progress could undermine efforts to ensure a smooth transition, posing a risk to financial stability. While few expect a delay similar to the one announced in November for legacy contracts that can’t be shifted to SOFR, it’s another example of the difficulties regulators have had in getting critical corners of the financial world on board.

“We’re in this classic chicken-and-egg scenario, where participants don’t want to trade because liquidity is low, but there’s not going to be enough liquidity unless people trade it,” Thomas Pluta, global head of linear rates at JPMorgan Securities, said of SOFR derivatives. “It’s increasing, but quite frankly there’s an awful lot more that needs to be done for this transition to happen.”

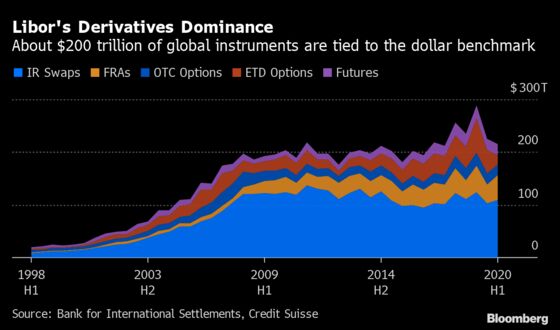

More than $200 trillion of financial instruments globally are tied to dollar Libor, with the vast bulk of that exposure in the form of derivative contracts, according to the Bank for International Settlements. The products are used by money managers to bet on the direction of monetary policy and corporations to hedge their interest-rate exposure.

Some market watchers predict the shift to SOFR derivatives will ramp up in the coming months after the Fed made clear late last year that it still expects banks and other regulated firms to stop entering into new Libor-based transactions by the end of 2021.

“That will force the issue quite a bit,” said Tyler Wellensiek, a managing director in rates sales at Barclays Plc. Nonetheless, she acknowledged that “there’s definitely a lot more work to do in SOFR liquidity.”

Officials at the Alternative Reference Rates Committee -- the Fed-backed group tasked with overseeing the Libor transition in the U.S. -- point to the gradual increase in SOFR activity across the swaps curve since the middle of last year as evidence that the benchmark is gaining traction among derivatives traders.

“The depth of liquidity has improved a lot,” said Tom Wipf, ARRC chair and a vice chairman of institutional securities at Morgan Stanley.

Add to that another potential boost in activity in the coming months with the setting of the International Swaps and Derivatives Association’s spread adjustment -- used to determine fallback rates for Libor contracts maturing after the benchmark is phased out -- and SOFR’s proponents see reasons to be encouraged.

Curve Delay

Still, there’s no guarantee the fixing of the spread adjustment will spark a surge in trading.

Other recent milestones in the Libor transition, including the so-called big bang shift by derivatives exchanges to SOFR for calculating the value swaps, and ISDA’s publication of a highly anticipated legal protocol to help convert Libor-linked contracts to SOFR, have produced relatively fleeting boosts so far.

Just 5.6% of all U.S. dollar risk in cleared over-the-counter and exchanged-traded interest-rate derivative transactions was tied to SOFR in November, according to data from ISDA and Clarus Financial Technology. While that’s almost double the 3% of trading activity that referenced the rate in June, it’s well off the record 9.7% reached in October, when global clearing houses made the shift to SOFR.

JPMorgan’s Pluta said he had expected the big bang to be “a catalyst for lots of different market participants to start trading SOFR actively,” but “many participants just did what they needed to do, and then reverted for the most part to Libor.”

Should the shift to SOFR derivatives struggle to gain pace in 2021, it could delay the ARRC’s ability to develop a forward-looking term reference rate, according to Marcus Burnett, the director of SOFR Academy, an education technology firm whose clients include banks and asset managers.

That may in turn discourage underwriters and issuers in the loan market from pricing new deals based off of the alternative benchmark.

“Without that, it’s less likely that we’re going to have a robust liquid and institutional-sized lending market based on SOFR,” Burnett said. “Without the lending market, we can’t have a broad-based transition.”

Some are already concerned that it could threaten the orderly functioning of markets.

“On some level it has to have implications for financial stability because of the uncertainty it generates,” Anne Beaumont, a partner at law firm Friedman Kaplan Seiler & Adelman in New York, said of SOFR’s modest progress so far. “You’re already going to have this fragmented world of new instruments linked to SOFR and legacy ones that rely on fallbacks.”

While recent jumps in SOFR trading that coincided with transition milestones have proven that banks can scale up their execution, the data suggest many likely aren’t seeing significant demand from clients for SOFR transactions and risk management, according to Chris Barnes, a senior vice president at Clarus.

SOFR still needs to gain significant traction to ensure a smooth transition, he said, especially with the possibility looming that the Fed will limit trading of Libor-linked derivatives in less than a year.

“Twelve months is an incredibly short period of time to try and change the precise product that people are trading,” Barnes said. But “if we as a market, as an industry can’t get behind a change in four years, that’s not a great sign.”

©2021 Bloomberg L.P.