Leveraged Loan Demand Fuels Payday for Company Owners in Europe

Leveraged Loan Demand Fuels Payday for Company Owners in Europe

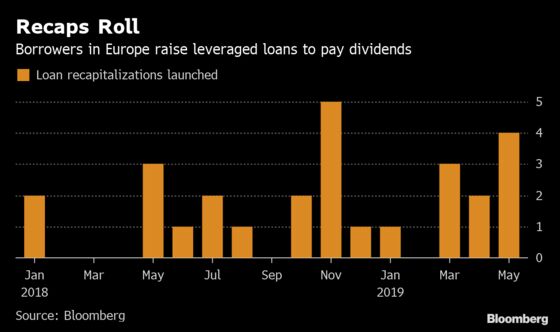

(Bloomberg) -- This month’s issuance pick-up in European leveraged lending brings a clutch of companies that want to raise debt to pay dividends to their shareholders.

German building materials firm Xella International GmbH and Nordic security systems provider Sector Alarm AB launched to syndication this week with plans to make payouts from the proceeds of new loan facilities. They join two other loan issuers seeking dividend-linked debt this week, plus two more via the bond market.

Companies coming to market now want to take advantage of stable market conditions that mean lenders should be in a broadly receptive mood. Primary loan issuance is about 30% down on the same period of last year, according to data compiled by Bloomberg, so there is pent-up demand for assets.

Despite this appetite, investors can be uncomfortable when they see companies upping their leverage to make payments to shareholders, and will be considering whether now is the right time to provide additional financing.

For their part, borrowers will have one eye on the possibility that market conditions beyond the summer break could be less accommodating, so it makes sense to come whenever there appears to be a clear path to getting an opportunistic deal done.

Tread Carefully

Although fund managers are often willing to lend additional money for a dividend to a known borrower that has delevered and is performing well, companies from cyclical sectors or that have complex credit stories still have to tread carefully.

In the case of Xella, Moody’s Investors Services said Tuesday that the borrower’s credit metrics are “already fairly stretched” for its B2 rating and its proposed dividend comes “late in the cycle” when Xella might be expected to be preparing to “weather a potential deterioration” in market conditions from next year.

Separately, software and services firm ION Investment Group Ltd. had to abandon plans this month to upstream $250 million from subsidiary ION Corporates, with the proceeds earmarked for an acquisition. Lenders objected to this element of a refinancing that was eventually withdrawn.

Timing can also go wrong. Last year, the loan market returned from the summer break in ebullient form. Come November, a batch of borrowers decided to make the most of keen demand and tight pricing to ask for dividends.

But conditions turned sharply against them as volatility struck. Kiwa NV increased its margin before wrapping up. Schur Flexibles GmbH eventually paid a margin of 600 basis points and offered a six point discount to par for its underwritten recapitalization.

Dividend Hunters

This month, further dividend recapitalizations via the loan market come from eyewear maker Rodenstock GmbH and advisory firm AlixPartners LLP. The latter is a newcomer to the European market but is well-known in the U.S.

On the bond side, autoparts firm Novem Beteiligungs GmbH is set to issue floating rate notes to refinance debt and repay shareholder loans. The company has a backstory in the loan market but is new to high-yield bonds. Norske Skog AS is also out with a bond issue to refinance loans from its shareholders.

Some of the dividend loans that came to market earlier this year saw large sums paid out. Hotelbeds raised 400 million euros ($447 million) from lenders in March toward a 500 million euro dividend payment, and in April Eircom Finco Sarl raised 400 million euros from a combined loan and bond transaction.

Sums raised in the U.S. recently have been even bigger. Sycamore Partners pulled off a $5.4 billion refinancing of Staples Inc. last month that funded a $1 billion dividend to the private equity firm. More recently, sponsors sold payment-in-kind notes to part finance a payout worth as much as $1.1 billion for drug research company Pharmaceutical Product Development LLC.

(Ruth McGavin is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

To contact the reporter on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Charles Daly, V. Ramakrishnan

©2019 Bloomberg L.P.