Leveraged Lenders Locked Into a Sisyphean Struggle on Loan Terms

Leveraged Lenders Locked Into a Sisyphean Struggle on Loan Terms

(Bloomberg) -- Time and again, lenders have demanded better protection from documentation in Europe’s leveraged loan market. They’ve frequently won changes this year--only to see the next deal appear at same borrower-friendly starting point.

Investors consistently object to loan documentation that gives private equity firms extensive freedom to pay dividends, to choose how they use proceeds from asset sales, to limit who can buy the loan in the secondary market, and more.

Anticipating that these terms could be valuable in the future, especially if economic conditions weaken, PE firms and their lawyers keep on driving for maximum flexibility despite repeated pushback. That’s leading to a gradual but continued weakening of lender protection in today’s yield-hungry market.

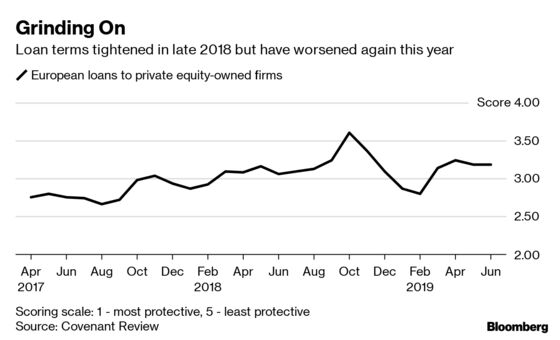

“If every time a deal comes to market with all the bells and whistles, even if there is pushback, the result is that documentation is still incrementally getting looser,” said Jane Gray, head of European research at credit research firm Covenant Review. “It’s a race to the bottom.”

Puzzling Process

If there’s any kind of bright spot for investors, it’s that they have got better at demanding improvements.

It’s become normal even on popular deals to see adjustments to initial terms, although lenders do sometimes let favored credits through with comparatively weak controls. On trickier credits, large investors will sometimes refuse to tell arrangers how much they’re willing to commit until the documentation is tightened, putting the onus on private equity sponsors to revise the terms.

In recent weeks, fund managers pressured Nestle Skin Health to improve terms relating to dividends and sale proceeds, while catering services firm Areas had to lighten secondary trading restrictions among other things. Those are just two instances out of a slew of borrowers that have amended terms after lender feedback, many doing so before the formal launch of syndication.

Terms were changed in favor of lenders on 59% of this year’s deals reviewed by Covenant Review in the "early-bird" phase of sell-down, and on 40% of those reviewed in syndication. Of those changed at "early-bird", 90% saw changes to the amount of additional debt the borrower can raise, and 70% changed terms relating to dividend payments and adjustments to earnings.

"Investors are far more engaged and knowledgeable, and far more wary. There is a lot more understanding and analysis than there was in late 2017 and through most of 2018," said Covenant Review’s Gray.

Meanwhile arranging banks have got used to the fact that private equity sponsors ask them to launch deals to syndication with documentation that they know won’t be accepted by lenders, before going through a negotiation to reach a point where the deal will sell.

One London-based banker said the firm’s credit committee doesn’t like this process on documentation and has been "puzzled" by it, but has understood that it’s how the market now operates.

Running Risks

More engagement and experience among investors and underwriting banks may make the process of negotiation feel familiar and normal, but it doesn’t negate the risk both sides are running. A difficult credit can become even harder to syndicate if loose opening documentation feeds into negative sentiment against the deal.

That’s especially true as investors become more cautious about which credits they want to support, now that 12 years have passed since the previous boom in leveraged lending imploded.

Spells of heavy loan issuance or volatile market conditions such as in late 2018 can help lenders in pushing for tighter terms. But any gains made by investors last year have largely dissipated and lenders’ perception is that terms continue to move against them, albeit slowly.

“Global documentation standards are the worst they’ve ever been," said Jonathan Butler, head of European leveraged finance at PGIM Fixed Income. "We’re seeing very high leverage and heavy adjustments to Ebitda, and the combination means that there are some very risky transactions.”

(Ruth McGavin is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

To contact the reporter on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, V. Ramakrishnan

©2019 Bloomberg L.P.