Leverage Is Exploding in the Fine-Art World

Leverage Is Exploding in the Fine-Art World

(Bloomberg) -- A $28 million Warhol. A $35 million Basquiat. A $70 million Twombly.

Hedge-fund manager Daniel Sundheim has acquired all these works — and more — while wielding one of the most powerful tools in finance: leverage.

Time was, art aficionados rarely talked openly about borrowing money against their paintings to build collections, make investments or just pay the bills.

But Sundheim, 42, is part of a new breed of collectors who are eagerly pledging artworks in exchange for lines of credit and, in the process, leveraging the $67 billion art market as never before.

In a few short years, Sundheim has emerged as a major trophy hunter, gaining entry to the board of the Museum of Modern Art alongside New York’s elite. As he built his collection, he pledged the top works against a credit line from JPMorgan Chase & Co., according to regulatory filings with the New York Department of State.

As of April, his collateral pool included 29 artworks, valued at an estimated $300 million based mainly on public prices paid, according to Beverly Schreiber Jacoby, president of BSJ Fine Art, a New York-based consulting firm with 30 years of experience with borrowers and lenders.

Like corporations and consumers, many top-end art collectors have been borrowing like crazy given this era’s ultra-low interest rates. Art-secured loans have jumped 40% since 2016, to at least $21 billion globally, according to Art & Finance Report 2019 by Deloitte.

Sundheim is hardly the only Wall Streeter to get in on the action. Money managers Steve Cohen and Michael Steinhardt also have pledged art as collateral against cheap credit lines, according to the regulatory filings.

“The collector base tends to come from credit-savvy, market-driven industries: private equity, hedge funds, tech, big data,” said Evan Beard, art-services executive at Bank of America Corp. “They built their companies using debt, and now they apply the same methodology to building art collections.”

Art bankers are happy to oblige. Often these specialists are part of broader wealth-management teams that target the very rich. Banks use the client’s total assets to determine the credit line and typically lend as much as 50% of the collateral value. They also allow billionaires to keep their art and offer 1% interest loans to a select few. For the rest, boutique lenders offer quicker turnaround and charge higher rates.

Some collectors are looking for arbitrage opportunities: They use art-backed loans to make other types of investments, including real estate, hoping to generate fatter returns. And some want access to dry powder on short notice to purchase another artwork or even a stake in a sports team.

“It’s exactly the same as why people have a mortgage against their house,” said Freya Stewart, who heads financial services at The Fine Art Group, an art adviser and boutique lender. “They are not necessarily buying another house. They are using the money to do something else.”

A spokesman for Sundheim declined to discuss the size of the credit facility backed by his art or how he uses the funds, but a person familiar with his thinking said he keeps the collateral as a working-capital line.

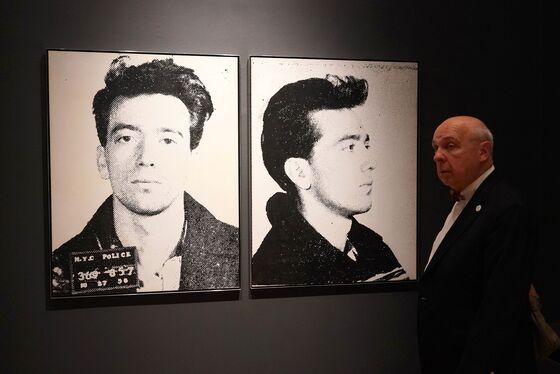

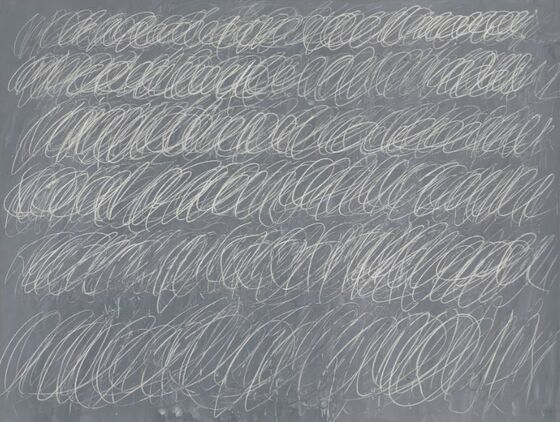

His collateral pool has grown 10-fold from about $30 million in 2013, according to appraisers who reviewed the list of art that backs his line. The pieces include Cy Twombly’s signature blackboard canvas “Untitled (New York City)” and “Leda and the Swan” as well as Andy Warhol’s “Most Wanted Men No. 11, John Joseph H, Jr.,” which fetched a total of more than $150 million at Christie’s and Sotheby’s auctions.

Sundheim started buying art around 2010 and opened his credit line with JPMorgan in 2013. He works with art adviser Sandy Heller, whose other clients have included Cohen and the Russian tycoons Roman Abramovich and Dmitry Rybolovlev.

The filings suggest Sundheim has become an active player at the top end of the art market, trading out of lesser works to make more significant blue-chip purchases. He owns a 1977 Willem de Kooning “Untitled XXXI,” which he bought for $21.2 million at Christie’s in 2014. The following year, he pledged a group of seven works to Sotheby’s to pay for Twombly’s “Untitled (New York City),” which sold for $70.5 million.

His Basquiats include “Dustheads” (1982), which he bought in 2016 at a steep discount from the price paid by Malaysian fugitive Jho Low three years earlier. Sundheim also owns a 1981 Basquiat self-portrait as a warrior king, brandishing a sword. That piece fetched $34.9 million in 2014, and Sundheim later purchased it in a private transaction.

The money manager has slowed his acquisitions since the launch of his hedge fund, D1 Capital Partners, in July 2018, according to a person familiar with his activities. The fund more than tripled in size since the launch to $9.3 billion in November, a rare blockbuster debut at a challenging time for the industry.

Still, Sundheim has jumped on some opportunities. In the fall of 2018, he picked up a drawing by Basquiat for $4.6 million at Phillips and a new Mark Grotjahn canvas from the artist’s solo show at Gagosian Gallery, where prices ranged from $3 million to $5 million. The two works were among 11 new pieces of collateral backing Sundheim’s credit line with JPMorgan, according to the latest filing in April.

Getting access to cheap money has become so popular that even old-school collectors are jumping into the fray.

Suzanne Gyorgy, head of art advisory and finance at Citi Private Bank, said a client who long opposed using art for collateral recently raised the subject.

“Why now?” Gyorgy recalled asking.

The client’s answer: “I’m at a dinner party with my friends — everyone has it but me.”

--With assistance from Miles Weiss.

To contact the editor responsible for this story: Pierre Paulden at ppaulden@bloomberg.net, David GillenMelinda Grenier

©2020 Bloomberg L.P.