Let's Hope We Don't Get Another August 2015

Let's Hope We Don't Get Another August 2015

(Bloomberg) --

Markets like a good pattern. The current set-up is no exception, and is looking increasingly like 2015: a good first half, a Chinese slowdown, PMIs not picking up, late-cycle signs with central banks set to ease to boost growth. There are a few differences of course, and one of them is the trade war. This could go either way, and while there’s no panic yet, investors should be cautious as we test the market’s resilience.

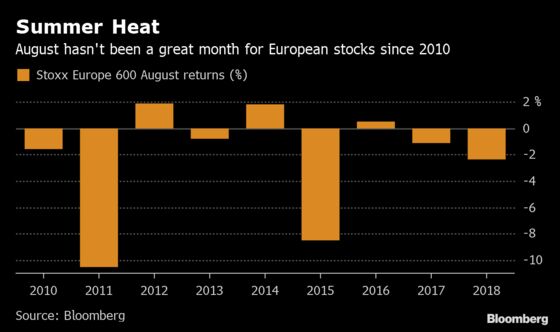

August hasn’t been a great month for European shares since the start of the decade. In 2011 and 2015 the month was particularly tough, with the Stoxx 600 falling 11% and 8.5% respectively. The index is down 2% so far this month.

“A market correction on trade-war escalation is always one tweet away,” says Oddo-BHF strategist Sylvain Goyon, arguing that investors got a wake-up call after the recent complacency. With earnings growth and macro indicators heading south, the equity risk premium cannot deflate and it would not be surprising to see the Stoxx 600 falling back towards the 370 level, Goyon says.

Looking at charts, the technical set-up is starting to look ugly. The European gauge is testing its upward technical trend started last December, after breaking its 50- and 100-day moving averages last week. The last time the index broke below its uptrend channel, back in April, we got a month-long 7% downside move. Granted, the uptrend back then was significantly steeper than now.

Last month, the Euro Stoxx 50 index failed to break above the 3,540 points resistance after some disappointment from central bank policies. The index is now facing the danger of continued profit taking, according to DZ Bank analyst Dirk Oppermann.

That said, there is no sign of panic just yet. The implied volatility of the Euro Stoxx 50 rose last week, but didn’t surpass the highs seen last May. Continuous volatility selling flow from structured-product desks may be capping the move, and proper panic-selling might be needed before we see higher volatility levels.

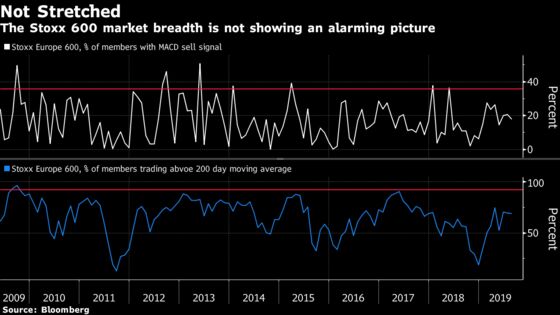

Looking at market breadth, the signals aren’t too alarming either. The amount of members triggering a momentum sell signal is not elevated and same goes for stocks trading above their 200-day moving average.

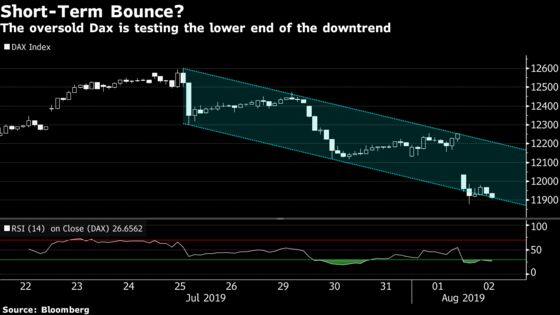

The very short-term view offers some positives as the downtrend initiated after July’s ECB meeting has now reached the lower end again, particularly on the exporters-rich DAX index. Technical indicators like the Relative Strength Index (RSI) also show an oversold signal, which could trigger a bounce in markets at some point.

With China letting the yuan tumble to the weakest level in more than a decade on Monday and asking state-owned companies to suspend imports of U.S. agricultural products, the ball is now back in President Trump’s camp. In the meantime, Euro Stoxx 50 futures are down 1.1% ahead of the open, while S&P 500 futures are down 1%.

SECTORS IN FOCUS TODAY:

- Mining stocks are likely to take a hit as increased U.S.-China trade tensions sour sentiment and hit copper prices, while the rout in iron ore is also gathering pace.

- Car stocks will be in focus following comments from Fiat Chrysler’s CEO in which he hinted he could be open to deals and a report that the collapsed talks between Renault and Fiat could restart.

- Oil stocks may drop, tracking crude lower as demand fears deepened after U.S. President Donald Trump threatened to slap more tariffs on China.

COMMENT:

- “European funds are largely underweight on value sectors,” Goldman Sachs strategists write in a note. “Banks is the largest underweight and other key ’Value’ sectors of MSCI Value, such as autos, energy, miners and utilities, are all underweights. However, portfolio managers have reduced the size of their short YTD, and banks are no longer the largest consensual short.”

NOTES FROM THE SELL SIDE:

- AB InBev upgraded to hold from underperform at Jefferies, with broker highlighting an improving growth picture, a more balanced approach and supportive macro.

- Metro Bank continues to have weak earnings momentum, but is upgraded to neutral with risk/reward seen more balanced and 2H mainly guided for, Citi says in note.

COMPANY NEWS AND M&A:

- Takeaway.com, Just Eat agree on all-share combination

- HSBC CEO John Flint Steps Down, Noel Quinn Named Interim CEO

- HSBC 2Q Adj. Pretax Profit Rises 4% Y/y; Plans Buyback

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 383.5 (50-DMA); 397.9; 395.1 (July high)

- Support at 374.5 (61.8% Fibo); 370.3 (200-DMA)

- RSI: 34.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,403 (61.8% Fibo); 3,445 (50-DMA)

- Support at 3,308.76 (50% Fibo); 3,293 (200-DMA)

- RSI: 33.1

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- AB InBev upgraded to hold at Jefferies; PT 85 Euros

- Gerresheimer upgraded to buy at HSBC; PT 85 Euros

- IAG upgraded to hold at HSBC; PT 4.60 Pounds

- Iberdrola upgraded to buy at Goldman; PT 9.90 Euros

- Metro Bank upgraded to neutral at Citi

- PGS ASA upgraded to buy at ABG; PT 20 Kroner

DOWNGRADES:

- BMW downgraded to sell at AlphaValue

- Bureau Veritas cut to equal-weight at Morgan Stanley

- Cobham downgraded to equal-weight at Barclays; PT 1.65 Pounds

- Daimler downgraded to underperform at Jefferies; PT 40 Euros

- Ferrexpo downgraded to neutral at Citi

- Fuchs Petrolub downgraded to hold at HSBC; PT 39 Euros

- Intertek cut to underweight at Morgan Stanley; PT 52.50 Pounds

- Pirelli downgraded to add at AlphaValue

- Renault downgraded to underperform at Jefferies; PT 42 Euros

INITIATIONS:

- Marks & Spencer resumed equal-weight at Morgan Stanley

- Ocado resumed equal-weight at Morgan Stanley; PT 13.20 Pounds

- PVA TePla rated new buy at Bankhaus Lampe; PT 16 Euros

- Shearwater Group rated new buy at Berenberg; PT 5 Pence

- Unite Group rated new overweight at Barclays; PT 12 Pounds

MARKETS:

- MSCI Asia Pacific down 2%, Nikkei 225 down 2.1%

- S&P 500 down 0.7%, Dow down 0.4%, Nasdaq down 1.3%

- Euro up 0.19% at $1.1129

- Dollar Index down 0.16% at 97.92

- Yen up 0.61% at 105.94

- Brent down 1.1% at $61.2/bbl, WTI down 0.9% to $55.1/bbl

- LME 3m Copper down 0.8% at $5682/MT

- Gold spot up 0.9% at $1453.1/oz

- US 10Yr yield down 7bps at 1.78%

ECONOMIC DATA (All times CET):

- 9:15am: (SP) July Markit Spain Composite PMI, est. 52, prior 52.1

- 9:15am: (SP) July Markit Spain Services PMI, est. 53.6, prior 53.6

- 9:45am: (IT) July Markit Italy Services PMI, est. 50.6, prior 50.5

- 9:45am: (IT) July Markit Italy Composite PMI, est. 50.1, prior 50.1

- 9:50am: (FR) July Markit France Services PMI, est. 52.2, prior 52.2

- 9:50am: (FR) July Markit France Composite PMI, est. 51.7, prior 51.7

- 9:55am: (GE) July Markit Germany Services PMI, est. 55.4, prior 55.4

- 9:55am: (GE) July Markit/BME Germany Composite PMI, est. 51.4, prior 51.4

- 10am: (EC) July Markit Eurozone Services PMI, est. 53.3, prior 53.3

- 10am: (EC) July Markit Eurozone Composite PMI, est. 51.5, prior 51.5

- 10:30am: (EC) Aug. Sentix Investor Confidence, est. -7, prior -5.8

- 10:30am: (UK) July Markit/CIPS UK Services PMI, est. 50.3, prior 50.2

- 10:30am: (UK) July Markit/CIPS UK Composite PMI, est. 49.8, prior 49.7

* For a wrap on developments in Europe’s equity capital markets, click here.

To contact the reporters on this story: Blaise Robinson in Paris at brobinson58@bloomberg.net;Michael Msika in London at mmsika4@bloomberg.net;Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editor responsible for this story: Celeste Perri at cperri@bloomberg.net

©2019 Bloomberg L.P.