Europe's Loan Spreads Reach 18-Month High in Flood of Issuance

Lenders Take Charge in July's European Leveraged Deal Crush

(Bloomberg) -- Companies raising debt in Europe’s leveraged loan market have crowded the room and spoiled their own party.

After raising more than 55 billion euros ($63.4 billion) through the end of July, already 70 percent of last year’s total, they have overwhelmed appetite from previously compliant lenders. July alone brought loans worth 7.1 billion euros to market, empowering investors to become more fussy and demand better terms.

Numerous issuers have been forced to pay more for their debt and to stomach tighter restrictions on loan documentation.

Despite the resistance, fund managers expect keen demand for loans as investment flows in via CLOs and other funds in the autumn, and are relying on new-issue supply to sustain the richer pricing levels set this summer.

"If supply is good, then regardless of flows pricing will at least stay steady. If supply outstrips it will widen a bit more," said Martin Horne, head of global high yield investments at Barings.

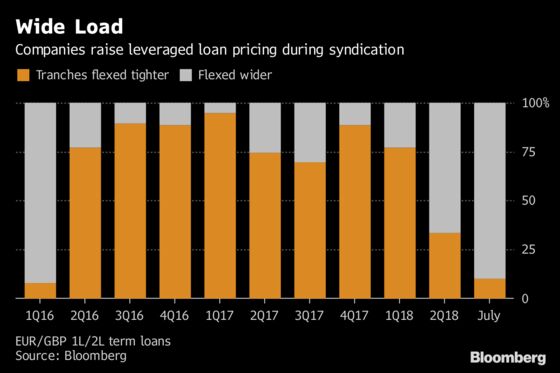

Spreads Rise

Heavy loan supply arrived at the same time as rising liability costs for CLOs -- the core buyers of leveraged loans -- as well as a repricing in the high-yield bond market as rate rises begin to loom.

Under these combined influences, average loan pricing hit an 18-month high at the end of July. Strong credits that might a year ago have tapped the market at 300-325 basis points over Euribor are now paying around 375 basis points, and middle of the road names are paying more than 400 basis points.

Beyond ensuring that risk is better reflected in pricing levels, lenders have turned the tide on documentation, which had become highly favorable to borrowers and sponsors in 2016 and 2017 as demand outran supply.

During June and July, some 25 companies made their deals more palatable to lenders by scaling back their freedom to pay dividends, trimming adjustments to Ebitda, improving fees and consenting to a host of other changes.

Some borrowers had to make more substantial changes. Coveris Rigid Deutschland GmbH and Imerys Roofing both added second-lien facilities to reduce senior secured leverage after lenders rejected initial terms.

Impala Joins Handful of Borrowers Making Deeper Cuts to Loans

Marlink AS, looking for a best-efforts dividend recap, abandoned its deal when lenders proved unwilling, sticking with its existing unitranche financing. And by the end of July there was still no sign of allocations on the LBO loan for Alexander Mann Solutions Ltd, nearly two weeks after commitments were due.

Supply-centric

The timing of the change in lenders’ behavior, from grudging acceptance of aggressive deals a year ago to this summer’s firm resistance, makes it tempting to attribute the shift to the same factors that have repriced the high-yield market.

That is: investors are getting more nervous as Europe moves toward the end of a 10-year credit cycle; the ECB’s bond buying program is ending and rates rises are looming; buyers are no longer reaching down the credit spectrum in search of yield.

But many loan market participants say these broader, macro factors are felt only indirectly, usually via the relative value play versus high-yield bond returns, while loan supply/demand remains the key driver.

"I don’t think the increase in loan pricing has been informed by worry over where we are in the credit cycle," said Dominic Ashcroft, co-head leveraged finance capital markets EMEA at Goldman Sachs.

Barings’ Horne notes no discernible increase in default rates, and doesn’t interpret the push and pull around documentation as a signal of the top of the market.

"There is no clear evidence that the credit cycle is ending. Deal structuring had got looser but now there is a merry-go-round of negotiations with arrangers so there is a counter move," said Horne.

- European speculative grade default rate fell to 1.94 percent in July from 1.95 percent in June, according to Standard & Poor’s data, published Aug. 1. The rate is forecast to rise to 2.5 percent at year-end, the rating firm said.

The market looks set for a busy September of new deals, which should help investors retain a grip on their new-found power. Refinitiv, the re-named financial and risk division sold to Blackstone Group LP by Thomson Reuters Corp, will raise a jumbo cross-border buyout financing, while more M&A transactions are lining up in its shadow. Thursday’s news that Cinven Ltd is in exclusive talks to buy Axa Life Europe continues the M&A issuance that has dominated the year so far.

- July M&A leveraged loan volume was 6 billion euros; 2018 year-to-date M&A volume now 41.8 billion euros, just ahead of full year 2017

- July’s largest loan was a 2.34 billion euro TLB for German metering services business Techem GmbH, the second largest euro-denominated TLB of the year

If new issuance does ease off after a September rush, as was the case in 2017, pricing isn’t expected to snap right back to the tightest levels seen last year, given the latent influence of the bond market.

"When supply and demand reverses, we will see a tightening in loans, but at some point relative value will be relevant because most loan managers can also buy bonds," says Ashcroft.

(Ruth McGavin is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

--With assistance from Gianluca Ansaldi.

To contact the reporter on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, V. Ramakrishnan, Charles Daly

©2018 Bloomberg L.P.