Korean Exotic Notes to Face Losses as Europe Banks Plunge

Korean Exotic Notes to Face Losses as Europe Bank Shares Plunge

(Bloomberg) --

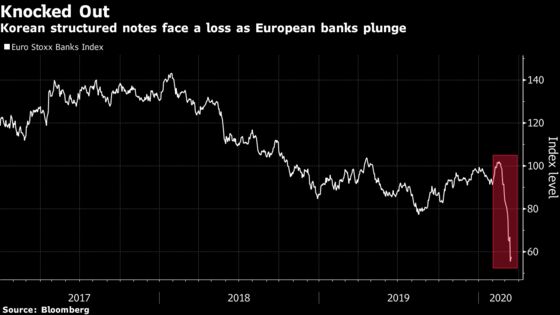

South Korean structured notes, favored by local retail investors, could face massive losses after European banking shares plunged more than 40% in the past month.

At least four Korean products linked to the Euro Stoxx Banks Index are likely to record losses of more than 50% if the underlying gauge stays at around the current level until their maturity, according to terms compiled by Bloomberg. The gauge has fallen 45% since a mid-February high on disappointment over European Central Bank stimulus measures.

Korea Investment & Securities Co. is one of the nation’s top 10 issuers of structured notes, and one of the products it offers is among those that could yield losses: a three-year note that guarantees a 7.8% annual return if none of three underlying indexes -- the Hang Seng Index, Euro Stoxx Banks Index, and Kosdaq 150 Index -- falls more than 50% from their closing levels on Sept. 28, 2017 and fails to recover. The Euro Stoxx Banks Index has dropped 58% since then, so the product will incur a loss unless the gauge bounces above the buying price by its maturity in September. The maximum loss can be 100%, according to the terms of the notes.

South Korean investors are known for their appetite for esoteric financial products fueled by a hunt for yield amid record-low domestic interest rates. The nation’s regulators have stepped up scrutiny over the improper sale of derivative products at local brokerages to retail investors, many of whom are elderly people seeking a stable yield for retirement.

In January and February, before the coronavirus hit global shares, Korean brokerages sold equity-linked notes with riskier conditions such as loss-making barriers of 35% or 40% rather than 50% or 55% previously, according to a report from DB Financial Investment. Among equity gauges, the Euro Stoxx 50 Index, the favored one for Korean notes, is also the most dangerous one, given that it’s already tumbled 33% from a high, DB said.

“The real risk for institutional investors like us is how those kinds of products could spark an unexpected crisis in financial markets,” said Jeon Kyung-dae, chief investment officer for equities at Macquarie Investment Management Korea. “No one had expected the so-called ‘KIKO crisis’ in 2008 -- when currency-linked derivatives sparked defaults at Korean small- and medium-sized companies. No one knows whether such derivatives can trigger a crisis this time, too.”

To contact the reporter on this story: Heejin Kim in Seoul at hkim579@bloomberg.net

To contact the editors responsible for this story: Lianting Tu at ltu4@bloomberg.net, Cecile Vannucci

©2020 Bloomberg L.P.