Kolanovic Says Risk Appetite Is Back in Stocks, Get Used to It

Kolanovic Says Risk Appetite Is Back in Stocks, Get Used to It

(Bloomberg) -- It’s time to embrace the nascent rally in the riskier part of the stock market, according to JPMorgan Chase & Co.’s strategist Marko Kolanovic, who says the economy is about to pick up and threats to the rally are overstated.

With central banks easing in sync, the firm’s macro indicators point to emerging signs of an economic recovery, particularly in Asia. For professional investors who have cut net equity exposure to extreme lows while boosting defensive holdings like low-volatility shares to record highs, it’s time to consider buying cyclical sectors such as energy, Kolanovic said.

“Investors are crowded in defensives and duration, and underweight or outright short cyclicals and value,” the strategist wrote in a note to clients. “Any increase of net exposure or paring down of gross exposure in the coming months (e.g. year-end) will drive rotation towards value and cyclicals.”

Kolanovic was echoing his JPMorgan colleagues, who earlier said the S&P 500 would climb to 3,200, bolstered by a rebound in corporate earnings. It’s advice investors have largely ignored. They’ve sought safety in dividend stocks or companies with growth perceived as resilient amid a worsening economy, such as software makers.

Stocks advanced for a fourth day Monday, closing at a record for the first time since July. Cyclical shares are poised to beat defensive for the second month in a row as financial firms supplanted utilities and real estate as market leaders.

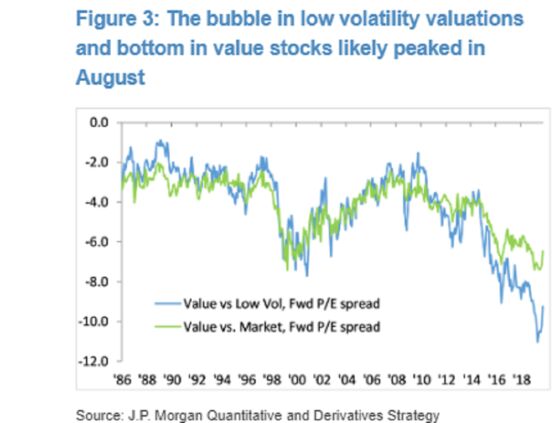

Persistent recession fears have prompted investors to shun cyclical shares such as banks and energy producers. As a result, many of those companies are now viewed as value investments, trading cheaper relative to earnings or sales. In August, value shares sat at the lowest discount in decades relative to low volatility, JPMorgan data showed. While the gap has narrowed in the past two months, it’s still nowhere near the average.

“The bubble in low volatility valuations and bottom in value stocks likely peaked this August,” Kolanovic wrote. “To hedge against a crash in low volatility stocks, investors should increase allocation towards value.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Chris Nagi, Richard Richtmyer

©2019 Bloomberg L.P.