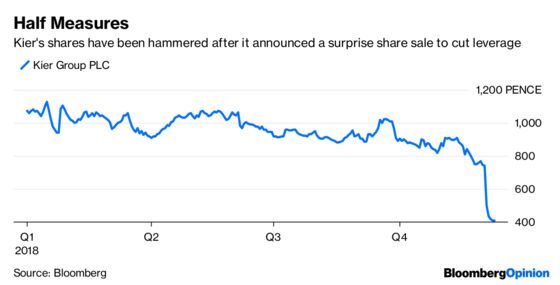

(Bloomberg Opinion) -- A British construction company launches a shock share sale to strengthen its balance sheet, pointing out that this is a preemptive move against business headwinds in 2019 and beyond. The market is having none of it. The collapse in Kier Group Plc’s shares over recent days points to fears that this won’t be its last capital increase. Its dire warnings about the industry have whacked peers too.

Kier is raising 264 million pounds ($336 million) in a rights offering to cut its net debt, targeting an annualized average level that doesn’t exceed its Ebitda. It says customers are paying more attention to contractors’ reported leverage when awarding contracts. Hence the need to raise funds before its next results.

The snag is that Kier has created the impression that it is raising as much as it can, which creates doubts about whether this is as much as it wants. The issue is equivalent to two-thirds of the current share count, the maximum new stock it can create without having to hold a shareholder meeting. As such, this is the biggest fundraising it can do before the end of the year. The two-week timetable is as fast as it can be.

Kier shares have dropped in recent days below the rights offer price of 409 pence, suggesting a high chance that its underwriters will be left with stock after certain shareholders follow through on their commitment to take their portion. Meanwhile, the so-called nil-paid securities, which confer the right to buy part of a share at the issue price, have been trading at between 5 pence and 10 pence. That only makes sense if people think the market share price will be just above the issue price when the offer closes the week after next.

It looks like a tense game of chicken. Doubtless there will be some hedge funds, having made a big gain from shorting the stock when it was priced above 800 pence, that can afford to wager on it falling further. For bulls, the nil-paids give them a chance to punt on a recovery at a fraction of the outlay of buying the shares outright.

And there is a bull case, of sorts. Kier is going for broke on the rights issue, but it hasn’t taken other available cash preservation measures. The full-year dividend was paid, and next year’s payout will be cut rather than scrapped. What's more, Kier has issued a profit forecast to give investors some sense of security.

For the short-sellers, the U.K. political backdrop has rarely been worse, which is important for a construction company. The rights offer will have drained the market of demand for the shares. The memory of Carillion Plc’s collapse is still fresh.

Meanwhile, sentiment in the sector is shot. A warning from Kier about tighter credit conditions has hurt the share price of rivals Costain Group Plc and Balfour Beatty Plc, which have reported net cash, as well as Keller Group Plc, which provides services to the sector but isn’t itself a construction group. That looks indiscriminate.

The market may be overestimating the industry’s need, as a whole, for fresh equity. What’s sure is that in any game of chicken someone has to lose.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2018 Bloomberg L.P.