Just as Traders Eye $100 Oil, Cracks Form in Bull Market

Just as Traders Eye $100 Oil, Cracks Form in Bull Market

(Bloomberg) -- No sooner had global oil prices rallied to nearly four-year highs and calls for $100-a-barrel crude resounded across the energy industry, than signs of weakness began to appear from Oklahoma to the Mediterranean.

Signs of a tight market are clear: global spare production capacity is shrinking, while major economies are humming and Asian refiners seeking an alternative to sanctioned Iranian barrels are drawing more cargoes of crude from the North Sea, West Africa and Texas.

At the Oil & Money conference last week in London, a gathering of several hundred industry executives, traders and bankers, the mood was relatively bullish on oil over the short-term, particularly for November, as Iranian and Venezuelan production slide.

Brent crude fell almost $6 a barrel since closing above $86 a barrel on Oct. 3, as a selloff in Treasuries and equities spread to commodities.

So where are the signs of weakness?

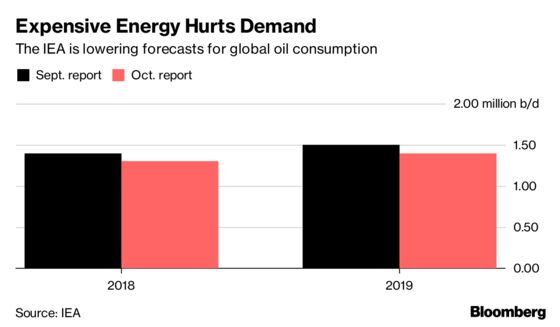

Demand

In London, the tone was more cautious for early 2019, when high prices are expected to dent demand growth.

"At $85 a barrel, and higher, you start to see quite a lot of stress in demand in emerging markets," said Alex Beard, head of oil at Glencore Plc.

After the International Monetary Fund last week cut its forecast for global growth and OPEC warned of lower demand for its crude next year, the International Energy Agency slashed its demand outlook for next year by 300,000 barrels a day, and warned that there could be further reductions ahead.

"The key factor that the market is not fully taking account of is on the demand side," Andrew Dodson, founder of Philipp Oil hedge fund, said in a September letter to investors. "Outside of the U.S., global economic activity has cyclically decelerated over the past six months, particularly in emerging markets but also in Europe, and this slowdown is likely to continue in our view."

Those sentiments were similar to those at the annual S&P Global Platts Analytics client event in New York in early October, where even with calls for $100 a barrel oil echoed by larger traders and macro hedge funds, some expressed concern over demand.

Refining Margins

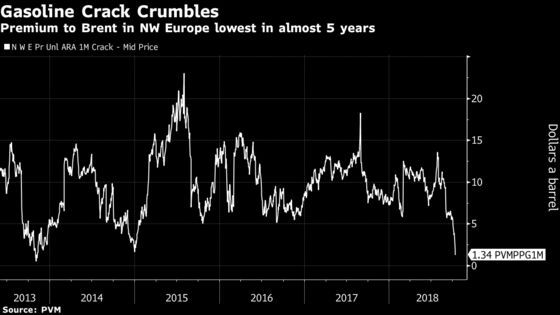

The combination of tight crude supply and slower gasoline demand growth is weighing on refining margins on both sides of the Atlantic.

In Europe, margins have been hit by the gasoline crack spread, or premium to crude, dropping last week to its lowest level since 2013, according to PVM data.

Both the Northwest Europe and the Mediterranean have seen poor margins recently, said Jonathan Leitch, analyst at Wood Mackenzie Ltd, citing rising crude prices and an increase in Russian diesel exports to Europe this month, in addition to the impact from gasoline.

"It’s difficult to see any bright spots for the rest of this year," Leitch said, citing refineries returning from maintenance, high gasoline stocks and seasonally weaker demand from industry and drivers as holidays approach and the weather worsens.

In the U.S., East Coast gasoline inventories are rising, unusual during peak refinery maintenance. Stocks are the highest since March 2017, and the highest ever for this time of year. That’s pressured crack spreads on the New York Mercantile Exchange to the lowest in more than a year.

Cushing Stockpiles

Inventories at the key U.S. storage hub of Cushing, Oklahoma, may accelerate this month. The expansion of Seaway pipeline, a key route for oil out of the hub, has been delayed. Fast-growing production from West Texas shale fields is filling pipelines in all directions, while refinery maintenance has reduced demand by about 1.7 million barrels a day.

Citigroup Inc. analysts forecast that Cushing inventories could touch 70 million barrels by April, pushing U.S. oil benchmarks even further below global levels than the current $10 a barrel.

Industry executives at the London conference highlighted that at $70-to-$80 a barrel, the U.S. shale industry would grow, even if the Permian Basin struggles with pipeline bottlenecks.

The weakness is illustrated by the so-called forward curve, or the price difference between various futures contracts.

The premium for first-month U.S. crude futures over the next-month contract settled at 8 cents a barrel Oct. 4, the lowest in almost four months. On Sept. 20, the spread was 48 cents.

Looking further out, the WTI December 2018-December 2019 spread Oct. 11 was the flattest in nearly a year, while the similar Brent spread narrowed by about $1.70 since the beginning of October.

Some of the flattening of the curve could be related to a lack of producer hedging in further-out contracts, according to John Saucer, vice president of research and analysis at Mobius Risk Group. Still, given how quickly the market has rallied in recent weeks, a "correction or at least a consolidation phase could happen," he said.

--With assistance from Mike Jeffers.

To contact the reporters on this story: Catherine Ngai in New York at cngai16@bloomberg.net;Javier Blas in London at jblas3@bloomberg.net;Jack Wittels in London at jwittels1@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Jessica Summers

©2018 Bloomberg L.P.