Junk Munis See Best Run Since 2009 With Pandemic Panic a Memory

Junk Munis See Best Run Since 2009 With Pandemic Panic a Memory

(Bloomberg) -- Since the middle of May, mutual funds that buy the riskiest state and local government bonds have received hundreds of millions of dollars of new cash from investors hunting for higher returns.

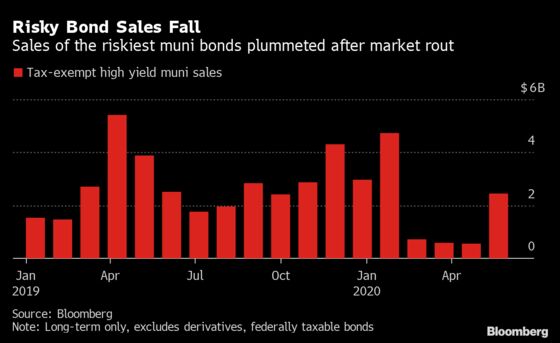

At the same time, the economic chaos unleashed by the coronavirus has put many speculative projects on hold, causing sales of junk and unrated municipal bonds to slow to a trickle.

That mismatch between supply and demand had a predictable effect: Prices of high-yield securities have rallied, driving them to a more than 8% gain from May through June. That marks the best two-month period since 2009, according to the Bloomberg Barclays indexes.

“The muni market has shown time and time again technicals are an extremely powerful force and can override fundamental trends,” said Gabe Diederich, a portfolio manager with Wells Fargo Asset Management. “What’s happening in the high-yield market is it’s the same bonds out there but more money is chasing them.”

The gains show the optimism that’s taken hold in segments of the financial markets despite broad uncertainty about the direction of the economy with the pandemic surging through Sunbelt states that were among the first to reopen. On Thursday, stocks rose after the Labor Department reported that 4.8 million jobs were added to payrolls last month as employees were called back to work, cutting the unemployment rate to 11.1%.

While the economic slowdown has left states and cities contending with massive budget shortfalls, the market is factoring in little risk, driving yields back to the lowest in more than six decades. That’s in part because governments have broad latitude to raise taxes and cut spending, minimizing the odds of default.

But there are signs of mounting distress in the riskiest corner of the municipal market, where speculative projects like nursing homes, factories and tourist attractions are often financed. This year, at least 104 borrowers have skipped debt payments, violated financial clauses in their contracts or drawn on emergency funds to cover what they owe, the most since 2012, according to Municipal Market Analytics.

Yet the $4 billion of bonds that have defaulted still represent a small fraction of the $3.9 trillion municipal market, underscoring the extent to which it acts as a haven during times of economic stress.

Fears to the contrary set off a record-setting pullback from municipal-bond funds in March, before the Federal Reserve’s interventions restored investors’ confidence. That has since reversed: since mid-May, high-yield municipal funds have received an average of $311 million of new cash each week from investors, according to Refinitive Lipper US Fund Flows data.

The influx of money, at a time when benchmark yields are so low, has driven big jumps in the prices of some high-yield bonds that tumbled the most during the March selloff. Puerto Rico bonds and those backed by state tobacco-settlemt payments -- which are among those most traded by mutual-fund managers who need to raise cash or invest it -- have both returned more than 12% since the start of May, according to Bloomberg Barclays indexes.

“It’s a lot more calm and technicals are a lot better,” said John Miller, the head of state and local government bond investing for Nuveen and manager of the biggest high-yield muni fund.

“People are shifting. They are no longer in panic mode,” he said. “Some of what you are seeing simply is oversold conditions in the first quarter and hence creating a precondition for a nice bounce back.”

©2020 Bloomberg L.P.