Junk to Drive 2022 Muni Supply to Record $500 Billion: Joe Mysak

Junk to Drive 2022 Muni Supply to Record $500 Billion: Joe Mysak

(Bloomberg) -- Here’s my call for 2022: U.S. states and local governments will borrow more than $500 billion in the municipal-bond market for the first time. You can credit investors’ taste for junk.

I am presuming here that any new coronavirus variants don’t prove to be dangerous enough to trigger further economic restrictions and the kind of severe market volatility that leads governments to rethink borrowing plans.

This year, issuers have sold $425 billion of long-term municipal debt, and my rough calculation places them on track to sell about $450 billion, just shy of the record of over $455 billion in 2020, data compiled by Bloomberg show.

Wall Street forecasts compiled by my colleague Danielle Moran show the average estimate is for about $470 billion of muni issuance in 2022, although projections range from $420 billion to $550 billion. I predict we’ll top $500 billion, and I expect muni junk will move the needle -- unrated, speculative deals sold only to qualified investors in minimum denominations of $100,000, $250,000 and $500,000.

The key reason I anticipate this boom is because the municipal market is becoming more professional, and those buyers hunger for yield. In 2022, I expect supply to catch up with demand. Again, this assumes the new variant doesn’t suppress issuance, a risk Municipal Market Analytics laid out this week.

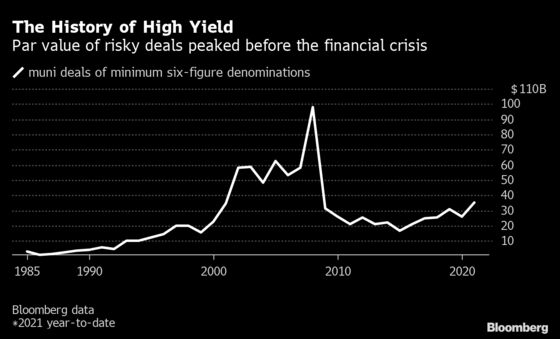

To get a sense of where we’re going, it’s useful to see where we’ve been. The chart above shows the history of the junk muni market through the annual volume of high-denomination transactions. Issuance didn’t hit the double-digit billions until the 1990s, and exploded in the 2000s, reaching $98.2 billion in 2008, or around 27% of the $362.8 billion in munis sold that year.

The financial crisis quashed demand for risky stuff. Junk issuance ultimately dropped to about $17 billion in 2015. It started to rebound the next year, and the 2021 tally stands at about $35 billion. If it finishes the year at $37 billion, -- the most since the 2008 boom -- that’s only 8% of the total of the $450 billion that I estimate we were on pace to achieve before the latest market turbulence.

So I expect the market to continue on the current trajectory, assuming no interruption to the present cycle of easy credit, which is emboldening developers to take on all manner of endeavors.

These kinds of deals typically finance risky projects like charter schools, recyclers, hangar operators at airports, minor-league stadiums, hotels, museums, theme parks and real estate projects that are way out there.

Pro Shift

And developers can typically have confidence that they’ll find funding in the muni market. As I say, the junk resurgence is happening in large part as the market is becoming more professional.

As Patrick Luby of CreditSights wrote, “individuals have shifted from direct ownership of individual bonds to indirect ownership via mutual funds, ETFs and CEFS,” referring to exchange-traded and closed-end funds. He continued, “The nearly stagnant level of individual bond holdings implies that some (perhaps most) growth in muni Separately Managed Accounts has come from the conversion of self-directed portfolios.”

Federal Reserve data show that the household sector owned $1.88 trillion of municipal securities in the second quarter, down from $1.92 trillion at the end of 2020. Cumberland Advisors this month cited a Citigroup Inc. estimate that separately managed accounts may comprise almost $800 billion of this.

Meanwhile, of course, mutual funds continue to grow, controlling $952 billion of the $4 trillion in outstanding munis, according to Fed data. Closed-end funds account for $97 billion and ETFs $76 billion.

Seeking Yield

These are the customers who want yield, and they’re not finding it in the plain-vanilla tax-backed munis so beloved by Mom and Pop investors. The BVAL 10-year top-rated benchmark yields around 1.05%, well below its five-year average.

Professional buyers want quirky, idiosyncratic deals that offer a big yield premium. High-minimum denomination deals offer yields hundreds of basis points over triple-A. The question is: For how long? The offering documents on junk deals usually warn buyers that their entire investment is at stake.

A couple more caveats to my $500 billion prediction. I’m not counting on tax-exempt advance refundings or a new version of Build America Bonds being restored to the Build Back Better legislation. Nor am I including munis sold with corporate cusips in my total.

(Joe Mysak is a municipal market columnist who writes for Bloomberg. His opinions do not necessarily reflect those of Bloomberg LP and its owner, and his observations are not intended as investment advice.)

©2021 Bloomberg L.P.