JPMorgan Sees Less Need for Hedges in Volatility Bear Market

JPMorgan Sees Lower Need for Hedges Amid Volatility Bear Market

(Bloomberg) -- Volatility is probably lower than it should be, but that doesn’t mean investors should turn defensive, according to JPMorgan Chase & Co.

Expectations of price movement across assets appear to be underestimated by about as much as they were in 2013 before the taper tantrum and in 2014 before the Federal Reserve began tightening, JPMorgan strategists led by John Normand wrote in a note March 15. That’s because volatility has drifted lower without a corresponding improvement in the macro environment, they said.

“Growth would need to return to early 2018’s pace to justify these levels of volatility,” the strategists said. However, they “are hesitant to turn defensive on this signal alone” as investor positioning doesn’t look overly cyclical apart from in emerging markets, previous undershoots lasted between nine months and two years amid a lack of catalysts higher, and most “wild cards” that could send it upward don’t appear imminent.

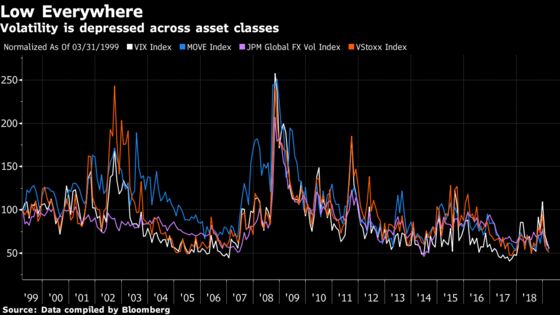

Volatility across assets has fallen to lows this year as the Fed, the European Central Bank and the Bank of Japan have all been relatively clear on their policy trajectories, while global economic growth slows but doesn’t collapse, and as China loosens fiscal and monetary reins. And while there’s still concern about issues like U.S.-China trade tensions and Brexit, so far those factors haven’t yet hurt worldwide markets as much as some feared.

The VIX fell 4.6 percent on Friday to 12.88, the lowest close since October, and Europe’s VStoxx ended the week at 12.92, the lowest since September. JPMorgan noted that implied volatility levels for rates in the U.S., Europe and Japan, as well as gold, fell to all-time lows in March. The JPMorgan Global FX Volatility Index is near its lowest level in more than four years.

“How much this rolling bear market in vols extends to riskier asset classes depends on whether central banks can lift the business cycle and make it more stable,” JPMorgan said in the report. “The good news is that policymakers can. The bad news is that vols seem to already price this outcome given an undershoot of fundamental and technical drivers.”

The mispricing suggests complacency, the report said -- but positioning, which isn’t overly cyclical, doesn’t echo that. Also, JPMorgan’s list of potential causes for a return to higher volatility, including failed U.S.-China trade talks triggering a tariff increase, U.S. auto tariffs on the EU and a destabilizing spike of Brent crude above $80 a barrel, don’t seem particularly immediate and most are of low to moderate probability, they said.

“Catalysts for mean reversion do not look imminent,” the strategists said. “Hence our lack of broad defensive hedges.”

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Ryan Lovdahl, John McCluskey

©2019 Bloomberg L.P.