JPMorgan Says Yield-Curve Message Distorted But Risk Remains

JPMorgan Says Yield-Curve Message Distorted But Risk Remains

(Bloomberg) -- Distortions in the Treasury yield curve mean it’s not necessarily signaling the risk of recession, according to JPMorgan Chase & Co. -- but the money-market curve still is.

A surge in the stockpile of negative-yielding debt across the world has warped the pricing of U.S. duration and credit risk as foreign investors are forced into Treasuries and U.S. corporate bonds, JPMorgan strategists including Nikolaos Panigirtzoglou wrote in a note Friday. That means the U.S. sovereign and credit-spread yield curves are losing their information content, making the less-affected money-market curve a better place to look for an economic signal, they said.

“U.S. recession risks are elevated in our mind by the inversion at the front end of U.S. money market curves which are less distorted by foreign flows,” the strategists wrote. Treasury inversions are “less of a reflection of U.S. recession risks and more of a reflection of the desperation for yield by foreign investors flocking into U.S. dollar-denominated bonds as bond yields turned more negative in Europe and Japan.”

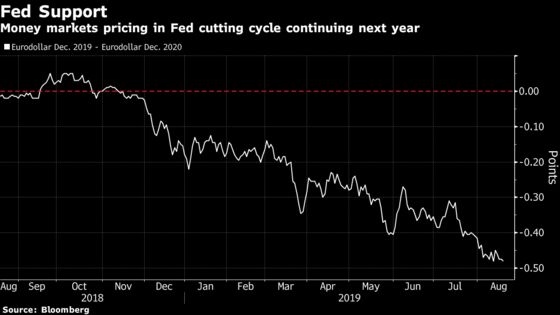

Negative-yielding debt hit a record $16 trillion last week after the key U.S. 2-year and 10-year yield curve inverted for the first time 2007 -- a move often considered a harbinger of an economic downturn. Money-market traders are expecting an increasing dovish policy path from the Federal Reserve, with Eurodollar contracts pricing in a cutting cycle until the end of 2020.

--With assistance from Stephen Spratt.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen, Andreea Papuc

©2019 Bloomberg L.P.