JPMorgan Says Major Assets ‘Overbought’ on Eve of Fed Easing

JPMorgan Says Major Assets ‘Overbought’ on Eve of Fed Easing

(Bloomberg) -- Investors betting the U.S. Federal Reserve is set to extend the market bonanza with a rate cut may have overplayed their hand.

JPMorgan Chase & Co. strategists are warning that a slew of risk markets are flashing “overbought” signals, with combined asset-manager positioning in U.S. equity futures the most extended in years. Aberdeen Standard Investments’ multi-asset team is preparing for disappointment as it lightens up on equity and emerging-market debt holdings ahead of the Fed’s meeting this week.

Central banks this year made a U-turn on their plans to tighten monetary policy, spurring an “everything rally” in both risk-on and risk-off assets. Fed funds futures indicate policy makers will lower rates about 80 basis points by the end of the year, starting with a quarter-percentage point reduction on July 31.

“This is an environment where there could be swings in sentiment, and we need to position ourselves for that,” said Ken Adams, head of tactical asset allocation at Aberdeen Standard Investments. “Maybe we won’t see the extent of monetary policy easing that’s now priced in. Investor expectations have become a bit too upbeat.”

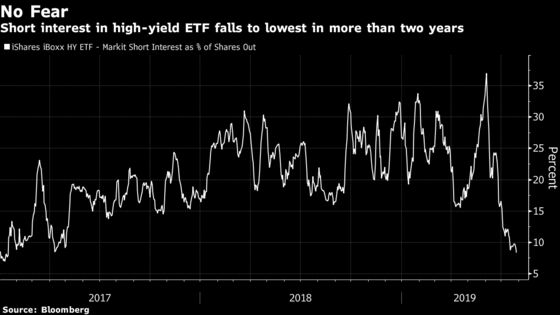

Bullish bets in U.S. equity futures come as the short interest in tech has tumbled while the biggest junk-bond ETF shows bearish options at a two-year low. Overweight positions in emerging-market sovereign debt are near a 2005 high, according to JPMorgan’s survey of its clients’ holdings.

“Assets that have benefited from the low yield environment are vulnerable to retrenchment if central banks fail to validate market expectations of easing over the coming months,” the strategists led by Nikolaos Panigirtzoglou wrote in a July 26 report.

In Europe, JPMorgan is worried about long positions in government bonds being at 2016 highs. The rally in European assets came to a halt last week after the European Central Bank provided scant detail on the size and timing of easing measures.

JPMorgan has a counter to the oft-quoted There Is No Alternative argument to buying risk, suggesting investors bulk up on U.S.-dollar cash via one-month Treasury bills yielding more than 2%. Aberdeen, on the other hand, has been adding to junk-bond holdings in recent months.

“We’re reducing our reliance on equity risk and shifting some of that risk into credit spread risk,” said Adams. “In an environment of sluggish growth, with central bank policy being supportive, it makes sense to harvest a spread.”

--With assistance from Luke Kawa.

To contact the reporter on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Cecile Gutscher, Sid Verma

©2019 Bloomberg L.P.