JPMorgan Says ETFs Won't Be the Biggest Victims If Credit Blows Up

JPMorgan Says ETFs Won't Be the Biggest Victims If Credit Blows Up

(Bloomberg) -- Working on ways to position for a potential collapse in corporate bonds? JPMorgan Chase & Co. has an idea: the exchange-traded funds that track the market.

While ETFs would experience collateral damage if a “credit bomb” were to go off, their greater liquidity through the secondary market might leave them less damaged than other alternatives, JPMorgan strategists including Bram Kaplan and Marko Kolanovic wrote in a note Friday. The Bloomberg Barclays US Corporate Bond Index is down 3.7 percent for the year, compared with a gain of around 6 percent in 2017.

“In the hypothesized scenario where credit markets freeze, every fund holding these securities will be hit hard and find it difficult to sell portfolio holdings,” the JPMorgan strategists wrote. “However, ETFs have the advantage of offering a secondary market, which provides holders with another avenue to liquidate (without needing to trade the underlying bonds), and may also provide a price-discovery function if the underlying assets aren’t trading.”

Assets in credit ETFs are about 10 percent of the size of credit mutual funds, so the latter would probably put more stress on the underlying market from any fund liquidations or redemptions, according to Kaplan and Kolanovic.

Furthermore, in extreme circumstances where the market for corporate bonds becomes distressed and illiquid, an ETF manager would be likely to keep the redemption basket as a representative sampling of the portfolio -- including some illiquid securities -- or temporarily freeze redemptions, the strategists wrote.

The report comes the same week that Adam Schwartz, a former director at Fir Tree Partners who runs his own hedge fund, said that he was shorting bond ETFs because their “structure isn’t really designed for a large market sell-off.” Specifically, he asserted that the funds would have to give away their most liquid securities, leaving their portfolios clogged with distressed and illiquid notes.

READ: Fund Manager Stakes Own Cash Betting Against Credit ETFs (Nov. 5)

ETFs and mutual funds have different redemption processes, but they produce the same result in that they usually require the liquidation of part of the portfolio, JPMorgan noted.

“Is shorting credit ETFs a good way to position for a possible collapse of corporate bonds?” the strategists posited. “Maybe (if you believe such an event is likely), but no more so than shorting the underlying index (e.g. via swap), and it’s a costly proposition in the meantime.”

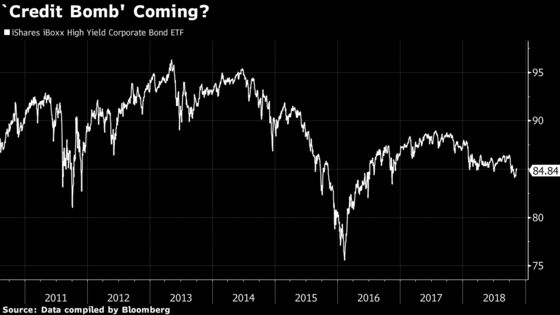

Shorting the iShares iBoxx High Yield Corporate Bond ETF, ticker HYG, currently costs more than 8 percent a year on a carry basis since it involves paying the approximately 6.75 percent bond yield plus a borrow cost of about 2 percent, minus the 0.49 percent management fee, Kaplan and Kolanovic wrote.

That said, the strategists acknowledged that there’s still a chance that credit ETFs could cause problems.

“We also can’t dismiss the very small probability that if enough investors believe the story that these ETFs are a ‘ticking bomb,’ their shorting activity could become a self-fulfilling prophecy, even if their views are misguided or self-serving,” they wrote.

To contact the reporter on this story: Joanna Ossinger in New York at jossinger@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Eric J. Weiner, Dave Liedtka

©2018 Bloomberg L.P.