JPMorgan’s Kolanovic Says Oil at $80 Is Where S&P 500 Breaks

JPMorgan’s Kolanovic Says Oil at $80 Is Where S&P 500 Breaks

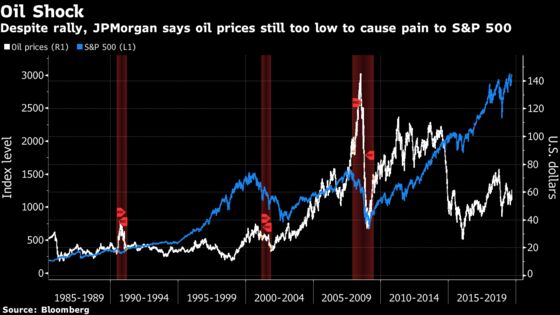

(Bloomberg) -- A surge in oil prices following a strike on Saudi Arabia’s crude production will have to get a lot bigger to cause serious trouble for the stock market, according to JPMorgan Chase & Co. strategists led by Marko Kolanovic.

The S&P 500 Index may start experiencing a “negative impact” only when oil prices reach a range of $80 to $85 a barrel, Kolanovic said after studying the historic relationship between the two assets. That’s about 30% above from crude’s recent levels around $62.

Higher oil prices can bolster energy profits and employment in the industry, but a rapid gain can hurt consumer spending, a key support in the U.S. economy. While Monday’s 15% surge was one of the fastest on record, crude still trades at less than half the peak level seen in 2008. Moreover, intensifying clashes in the Middle East may prompt China and the U.S. to reach a trade deal to remove uncertainty over the global economy, Kolanovic pointed out.

“Where is the break-even point when oil starts hurting the S&P 500?” he wrote in a note to clients. “This is still far away.”

That’s not to say oil has no impact on stocks at current levels. Energy shares rallied 3.3% Monday along with crude prices, offsetting losses in consumer stocks. To Kolanovic, the outperformance will accelerate a rotation from momentum and low-volatility stocks to value, a process that has bolstered previously unloved industries like energy and caused pain for many traders this month.

The reversal came after valuations in low-volatility and momentum stocks increased to unprecedented levels relative to value. So much money has flowed to the long low-vol, short value trade that it’s reminiscent of the 2018 vol-pocalypse to Kolanovic.

In 2017, market calm lured investors to a sense of complacency with bets on a decline in volatility reaching a record. That trade went bust in February 2018, leading to the closure of VelocityShares Daily Inverse VIX Short-Term ETN, or known as its ticker XIV.

Since then, investors have sought safety in low-vol and shunned risky assets such as energy, pushing the risk-off trade to extremes that Kolanovic sees at the cusp of collapsing like XIV.

“These trades worked well until the rotation started, and now are in the early stages of a collapse,” he said. “The recent spike in oil will just accelerate this unwind and eventually lead to a capitulation of the short value/beta trade.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Chris Nagi, Richard Richtmyer

©2019 Bloomberg L.P.