JPMorgan’s $50 Billion Fund Is Selling Stocks on Dovish Fed

JPMorgan’s strategy comes as the Fed signaled that it’s done raising interest rates until inflation accelerates in the U.S.

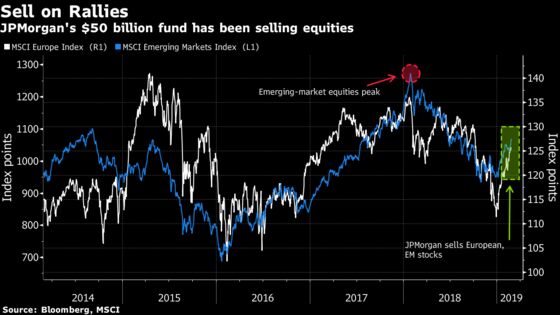

(Bloomberg) -- One of JPMorgan Asset Management’s largest mutual funds is selling stocks on wagers a dovish Federal Reserve is signaling burgeoning risks to global economic growth.

Eric Bernbaum, co-portfolio manager of the firm’s $50 billion Global Income Fund, has cut European and emerging-market stock exposure to about 27 percent in February from 31 percent in October. He continues to favor junk bonds, though has also loaded up on low-risk, highly liquid money-market investments -- an asset class he didn’t own this time last year -- as a buffer.

The Fed’s “more dovish pivot should be recognized that it was taken because they had a less favorable view of both markets and economic growth,” New York-based Bernbaum said in a telephone interview. “The risk reward trade-off -- both from a return perspective and certainly from a yield perspective -- is more attractive in corporate credit today than it is in equities.”

The risk of a U.S. recession in the next 12 to 18 months is still “pretty low,” and the central bank action is likely to to push out the economic cycle “a bit further,” he added.

In testimony before Congress Tuesday, Federal Reserve Chairman Jerome Powell said a healthy U.S. economy has faced some “crosscurrents and conflicting signals” that officials in January decided warranted taking a patient approach to future interest-rate changes.

Bernbaum’s strategy comes as the Fed signaled that it’s done raising interest rates until inflation accelerates in the world’s biggest economy, switching from last year’s expectation of further gradual hikes. After nine increases since 2015, economists including those from Goldman Sachs Group Inc. have pared back their calls for rate hikes, citing a higher bar for the central bank to ratchet up borrowing costs in 2019.

The $1.7 trillion money manager is still positive on risk assets, but sees junk bonds as a safer avenue to play the dovish Fed-induced rally, according to Bernbaum. Low default rates and sound fundamentals make riskier corporate debt attractive, and the fund is likely to continue adding money into the asset class, he said.

U.S. junk bonds comprised 27 percent of the fund, while about 9 percent was invested in European junk, according to JPMorgan. The Bloomberg Barclays U.S. Corporate High Yield Index has risen about 6 percent year-to-date, versus a near 12 percent gain in the S&P 500 Index.

Below are edited comments on his views on other asset classes:

Short Duration Buffer

Agency mortgages and short-duration fixed-income instruments comprise 12 to 13 percent of the portfolio today -- a mix of money-market type assets as well as very high quality corporate credit and asset backed-securities. This makes us very comfortable with our meaningful weight in high-yield credit, where we know at times liquidity can be restricted.

Range-Bound Treasuries

Our expectations on yields have come down moderately -- we see fair value for 10-year Treasury yields by the end of the year in a range of 2.5 to 3 percent. If we start to see yields creep up toward 3 percent it might become an entry point to add a bit more high quality duration assets to the portfolio.

Rich Dollar

The greenback will remain relatively range-bound this year, although from a longer-term valuation perspective, the dollar looks a bit rich. We expect there to be a bit more nuance in how the dollar moves relative to emerging-market currencies.

China Risk

We do recognize that there are some upside risks to China should there be resolutions to discussions between the U.S. and China on trade. In the near term though, some of the structural and important issues -- things like cyber security or intellectual property rights -- are going to be hard to resolve.

To contact the reporter on this story: Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen, Joanna Ossinger

©2019 Bloomberg L.P.