JPMorgan Asset Says It’s Way Too Soon for Negative U.S. Rates

JPMorgan Asset Says It’s Way Too Soon for Negative U.S. Rates

(Bloomberg) -- Traders are getting ahead of themselves pricing in negative U.S. rates next year, according to JPMorgan Asset Management.

“Three, four years down the line if the economy is still in a very weak state, then perhaps the Federal Reserve could consider negative rates,” said Seamus Mac Gorain, head of global rates in London at the $1.7 trillion investment manager. “For now, they’re much more focused on the balance sheet, on their tools rather than on negative rates.”

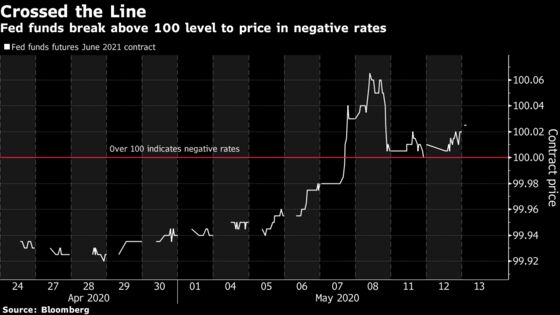

Fed Chair Jerome Powell and his colleagues have pushed back against the need for negative rates, questioning its usefulness as investors weighed the possibility. Futures markets are pricing for that to happen, with contracts on Fed funds rate showing bets for the move in the second quarter of 2021.

The positions are showing up as companies and funds weigh how long the U.S. economy could take to recover from the coronavirus pandemic amid a constant drumbeat of negative economic data.

Stories on Negative Rates |

|---|

Negative Rates Are the Only Game in Town for U.S. Option Traders Barclays Sees Risk of Yield Shock as Main Street Lights Go Out Negative Rates Bets Are Going Global to Ire of Central Banks (1) Traders Bet U.K. Will Have Negative Interest Rates by Year End |

Powell said in a television interview with CBS that a recovery could stretch through until the end of next year, and depend on the delivery of a vaccine. He also noted that negative rates were “probably not an appropriate or useful policy,” with the distortions to markets offsetting benefits.

For a related story on Powell interview, click here.

“They’ve seen the cost of negative rates now at these levels, in terms of the impact on the banking sector,” JPMorgan Asset’s Mac Gorain said. “On the whole, the shift is a little bit away from negative rates.”

While it “makes sense” to price the tail risk of negative rates, most central bank signals suggest the opposite may be true for now, he said. The European Central Bank had “several opportunities to cut rates again and they haven’t done it,” and the same could be said of the Bank of Japan, he added.

Bond Bets

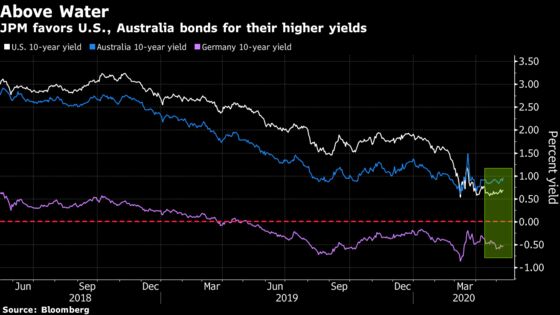

JPMorgan Asset favors 10-year Treasuries as the looming global recession pumps up demand for the safest sovereign debt, Mac Gorain added. Benchmark Treasury yields are likely to fluctuate between 0.5% and 1% this year, with any movements toward the top end of the range a signal to buy, he said. The rate was around 0.68% in New York morning trading Monday.

The asset manager is also buying government bonds from Australia, which sold a record A$19 billion ($12.3 billion) in 10-year notes last week.

“The long-end in Australia is another market that stands out” for its high quality and yield, he said.

Here are some more edited comments from Mac Gorain:

Dollar Weakness

The medium-term outlook for the dollar is a decline against its major peers. Its yield advantage has been eroded and while there was a big squeeze in the dollar funding market in March, the Fed has addressed that through its domestic bond operations and commercial paper programs.

Global Economy

Asia, the U.S. then Europe may lead a post-virus recovery. It does seem that the virus hasn’t affected Asia quite as much, but at the same time, the global economy is very integrated. It is difficult to see very strong growth in any region when the rest of the world is so weak.

Debt Monetization

At this point there’s no conflict whatsoever between central bank mandates and their government bond purchases. Inflation was already quite limited before the crisis, and is likely to be very weak for a while. The fall in oil prices also helps.

Bond Supply

The biggest driver in bond markets this year is the unprecedented supply and demand for debt. It’s true in the U.S., it’s true in the rest of the world. To a greater-or-lesser extent, most of the central banks are absorbing the unprecedented supply.

©2020 Bloomberg L.P.