Japanese Investors Chase 15% Yields All the Way to Turkey

A 15% yield buys you a lot of patience in a world with $14 trillion of negative-yielding debt.

(Bloomberg) -- A 15% yield buys you a lot of patience in a world with $15 trillion of negative-yielding debt.

That explains why Japanese investors are willing to set aside a host of concerns when it comes to Turkey -- everything from worries about its monetary policy to geopolitical tensions with the U.S. and a deteriorating credit rating.

“I like Turkey not because of great fundamentals,” said Takeshi Yokouchi, a senior fund manager at Sumitomo Mitsui DS Asset Management Co. in Tokyo. “They offer very attractive yields.”

Yokouchi has bumped up Turkish lira investments to 14% in the portfolios he oversees, the highest it’s been in recent years. Holdings of Turkish assets among Japanese mutual funds more broadly climbed to 106 billion yen ($1 billion) in June, compared with 61 billion yen a year ago, according to data from Japan’s Investment Trusts Association.

The fund manager is unfazed by the risk-off sentiment triggered by President Donald Trump’s announcement of new tariffs on China last week and the Chinese currency’s decline beyond 7 per dollar as investors’ search for yield has been quite strong, Yokouchi said. “So, I plan to continue to hold this overweight position on Turkey for now,” he said.

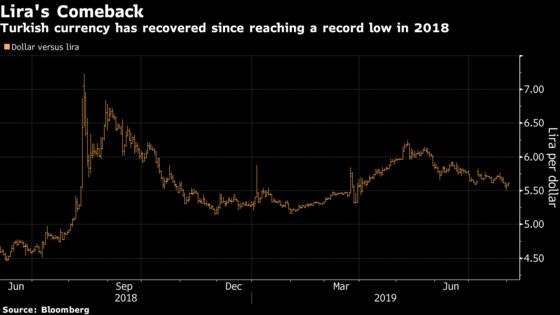

Japan’s retail investors are among those confronting the challenge of negative interest rates that has spread across the globe. Their increase in Turkish holdings covered a period that saw a slide in the lira to a record low, pressure from President Recep Tayyip Erdogan for interest-rate cuts and the threat of U.S. sanctions over Turkey’s purchase of a Russian missile-defense system.

Rating Risks

Yokouchi highlights that he’s not blind to the risks. He’s keeping watch on Turkey’s credit ratings, given the possibility that any further deterioration could trigger mandated liquidation of positions in his funds. Moody’s Investors Service in June cut the local-currency credit rating deeper into junk territory. S&P Global Ratings on Friday left its grade unchanged.

For now, he’s sitting tight. His High Yield Currency Open fund returned 2.5% in the month through the end of June, according to his firm, which had assets under management worth about $160 billion as of Jan. 1.

There might have been more gains last month. For all the worries about Erdogan’s surprise replacement of his central bank chief, the lira ended up climbing after newly installed Murat Uysal delivered the biggest rate cut in at least 17 years on July 25. It’s up about 2% against the dollar since then, the top performer among 22 emerging-market currencies tracked by Bloomberg.

“Turkish notes give outstandingly higher yields compared with many other emerging-market assets, making it popular,” said Tsutomu Soma, general manager of investment trust and fixed-income securities at SBI Securities Co. in Tokyo. Falling U.S. rates encourages investors to buy Turkish assets despite some negative factors surrounding the nation, he said.

--With assistance from Constantine Courcoulas and Karl Lester M. Yap.

To contact the reporters on this story: Yumi Teso in Bangkok at yteso1@bloomberg.net;Tomoko Yamazaki in Singapore at tyamazaki@bloomberg.net

To contact the editors responsible for this story: Justin Carrigan at jcarrigan@bloomberg.net, Christopher Anstey

©2019 Bloomberg L.P.