Japan Stocks Can Be the Haven in a Bleak World

Japan Stocks Can Be the Haven in a Bleak World

(Bloomberg Opinion) -- Global equity investors have reason to be concerned: The economic outlook is worsening, interest rates are rising and tensions in the U.S.-China relationship could further harm growth. But all is not bleak. Japan provides a measure of certainty and promise, with a stable government, expanding economy, improving return on equity and booming tourism.

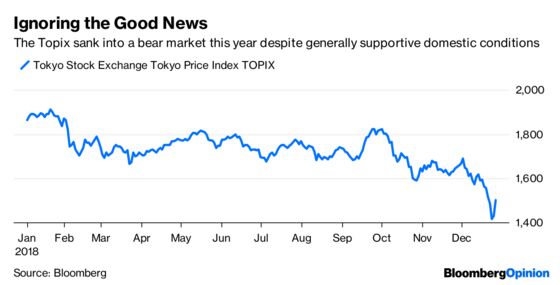

Japanese stocks aren’t reflecting these positive factors. The Topix entered a bear market in 2018, dropping more than 22 percent from its January peak to a two-year low. The index closed out its worst December performance in 59 years on Friday. Year to date, international investors have sold more than $48 billion of shares.

Yet the country remains on track to record the longest period of economic growth, at 74 consecutive months, in the post-war era, according to a report in the Nikkei that cited the government’s monthly economic report.

Granted, risks to the outlook are increasing. Bank of Japan Governor Haruhiko Kuroda has noted, in particular, dim prospects for overseas economic development and diminishing demand for Japanese exports. Meanwhile, an increase in the sales tax to 10 percent from 8 percent scheduled to take effect in October 2019 will weigh on domestic consumption. Still, Kuroda has promised to keep close watch and respond if needed by cutting interest rates, boosting asset buying and accelerating the pace of money printing.

The political environment is supportive. Prime Minister Shinzo Abe won the ruling party leadership election in September, empowering him to implement pro-growth structural reforms with little opposition. The so-called “Third Arrow” of his Abenomics program is designed to promote expansion of Japan’s economic output by improving workforce diversity, adjusting corporate taxation, and reforming heavily protected industries such as agriculture and healthcare.

Many Japanese companies have reported record profits in recent quarters. Return on equity for the MSCI Japan Index has doubled to 9.8 percent from 4.4 percent in 2012, according to a report by Morgan Stanley. Improvements came from better operating margins and a reduction in taxes, interest, and non-operating expenses. ROE could reach 12 percent by 2025, the New York-based investment bank predicts.

Though Japan’s long-term prospects seem relatively clear-cut, declining fertility rates remain problematic. The current population of more than 127 million is expected to shrink by a third in less than 50 years. This doesn’t deter Jesper Koll, chief executive officer of fund manager WisdomTree Japan Inc., who told me recently: “Look on the bright side. The older generation will pass its wealth to the next, and along with it, substantial newfound purchasing power.”

Notwithstanding declining fertility, other areas of Japan’s economy continue to show improvement, such as tourism. Fifteen years ago, the total number of foreign visitors to Japan was roughly 5 million. This year, the country welcomed 30 million tourists, and with an anticipated 40 million planning to visit in 2020 ahead of the Olympics, the government is upgrading the country’s infrastructure to help businesses deliver products and services.

Those who choose to invest in Japan in the New Year should focus on companies exposed to domestic consumption such as Matsumotokiyoshi Holdings Co., one of the country’s largest drugstore chains, and Bic Camera Inc., a one-stop shop for all things electronic. Local companies with international appeal may also be worthwhile investments, such as athletic shoemaker Asics Corp. and confectionery producer Morinaga & Co.

Those adverse to individual stock-picking can consider acquiring broad exposure to the Topix. The forward price-earnings ratio for the index is at 11.8 times, its lowest level in the past five years. In fact, fewer than 60 days in the past decade saw the Topix trading lower than the current multiple.

In sum, Japan is ready for thoughtful increased international investing, though keep an eye on political and economic factors.

(Ronald W. Chan and his firm, Chartwell Capital, do not hold positions in the companies he writes about for Bloomberg Opinion.)

Dec. 31 is a public holiday in Japan.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ronald W. Chan is the founder and CIO of Chartwell Capital in Hong Kong. He is the author of “The Value Investors” and “Behind the Berkshire Hathaway Curtain.”

©2018 Bloomberg L.P.