Jane Street Defends ETFs From Claims They Cause Market Stress

Jane Street Defends ETFs From Claims They Cause Market Stress

(Bloomberg) -- Investors looking for potential causes of volatility in the debt markets have nothing to fear from exchange-traded funds, according to one of the industry’s largest market makers.

“While credit ETFs will become more costly to trade in a stressed market, they don’t pose a systemic risk,” Andrew Upward, an ETF strategist at the firm, wrote in a paper dated July 23. “Nothing about the structure of credit ETFs per se suggests they will be the cause of disorderly trading in the underlyings.”

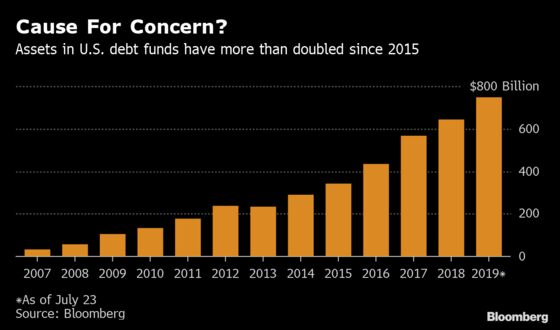

ETFs have been decried over the years as everything from a Marxist subversion of capitalism to a weapon of mass financial destruction that will bring on the next crisis. But while debt investors’ anxiety has typically revolved around how these funds will respond to large, sudden withdrawals, skeptics are now homing in on secondary trading in the $750 billion market for U.S. bond ETFs, and questioning whether users fully understand how the securities behave in times of stress.

In that respect, Jane Street’s full-throated defense is hardly surprising; the company trades $1.6 billion of debt ETFs every day, according to a letter to the U.S. Securities and Exchange Commission last year. But competition between electronic brokers for those trades is one reason why debt ETFs aren’t a serious threat, according to Upward.

When ETF sellers push the price of a fund below the value of its holdings, market makers like Jane Street buy the ETF shares and swap them with the ETF manager for the underlying bonds. Known as a redemption, the market makers can then sell the securities for their higher price, booking a small profit.

Specialist traders have built entire businesses on this arbitrage, using superior speed and technology to edge out many of the banks that used to dominate. So if prices of either the funds or bonds look to have fallen too far, too fast, market makers may calculate that it makes sense to hold onto them and look to sell when prices recover, wrote Upward. Put simply, they have an incentive to stay in the game, rather than blindly feeding a slump.

Instead, ETFs could actually rein in a bond rout, as market makers facing a less liquid credit market will pass on their higher costs of trading to investors wanting to sell. While that could take some by surprise, it also discourages excessive selling, wrote Upward.

“If selling the underlying bonds is difficult or expensive, selling ETFs will become expensive, too,” Upward said. “By lowering their ETF bid prices, market makers discourage further ETF selling. One can think of it as the ETF market’s last-resort mechanism for resolving the liquidity mismatch problem. Meanwhile, ETF investors who very urgently need to sell can still do so.”

To contact the reporter on this story: Rachel Evans in New York at revans43@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh, Rita Nazareth

©2019 Bloomberg L.P.