Jaguar Land Rover Needs to Get Out of This Rut

Tata Motors’ luxury unit will have to move more quickly to restore profitability, especially in China.

(Bloomberg Opinion) -- Tata Motors Ltd.’s Jaguar Land Rover unit can’t seem to get back in the right lane.

The Indian automaker’s luxury arm dropped into the red in the quarter ended Sept. 30, posting a pretax loss of 90 million pounds ($116 million), with Ebit margins below breakeven and volumes down. Sales in China, where the high-end market is still growing, tanked. JLR has long been a profit center for the whole company. This time it took the domestic Indian business down with it, reversing recent signs of recovery there.

Not only was JLR’s performance dismal, there were few indications of a brighter future. The maker of Range Rovers and the E-Pace SUV ran more than 600 million pounds of negative free cash flow in the quarter, making a 2.3 billion-pound cash burn for the first half of the year – almost double the amount in the same 2017 period. Kenneth Gregor, chief financial officer of the U.K.-based unit, said he expected negative free cash flow for the full year.

To show it’s trying to fix things, JLR announced Project Charge, a two- to three-year plan to boost profitability and cash flow. The aim is to bring in as much as 2.5 billion pounds over the next 18 months. Investment plans were cut from 4.5 billion pounds a year to 4 billion pounds for this year and the next, saving about 1 billion pounds overall – half of the six-month cash burn. In the latest quarter alone, though, total investment outlays were 1 billion pounds. Further reductions will be tough, because much of this spending isn’t variable.

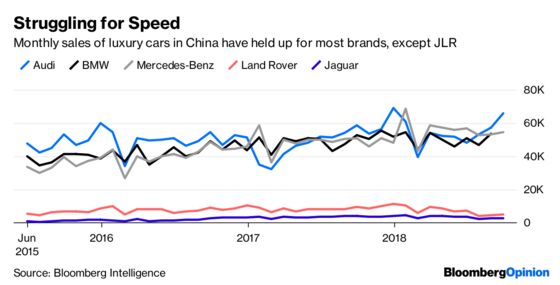

JLR blamed China, pointing to sagging consumer confidence in the world’s biggest car market. That’s true, though not necessarily for the high-end segment that JLR occupies. Even its American peer General Motors Co., which has lost overall market share in China, reported a sales pop for its luxury Cadillac models. Brands such as BMW, Mercedes and Audi increased sales there by 5 percent to 15 percent in the first nine months of the year. (JLR also cited generic factors like slowing Chinese economic growth, Brexit, trade tensions and higher tariffs.)

Moreover, while the wider China market generally struck a balance between inventory, production and sales, JLR was unable to manage inventories for locally made and imported cars.

And the debt burden is increasing, both in total terms and relative to Ebitda. Liquidity was bolstered by borrowings: JLR took out another $1 billion loan in September, which it drew down in October. The ratio of free cash flow to debt (the amount of debt that could be paid in a year if all free cash flow were used) is well below peers.

The unit sold 500 million euros ($567 million) of bonds in September, though unlike previous issues, these didn’t contain a covenant capping dividends payable to Tata Motors. How far JLR can move at this pace is unclear: As of June, its quarterly ratio of liquid assets to all current liabilities had dropped to the lowest level since 2011. The parent was down, too, on that basis.

JLR did report some cost improvements, but far too few to move the needle. Management needs to do more, and sooner, to get the carmaker back on course.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2018 Bloomberg L.P.