It's Hedge Funds Against Long-Term Players in Japan Stock Market

It's Hedge Funds Against Long-Term Players in Japan Stock Market

(Bloomberg) -- The rally that’s pushed Japanese equities to a three-month high hides a different story when it comes to the cash market.

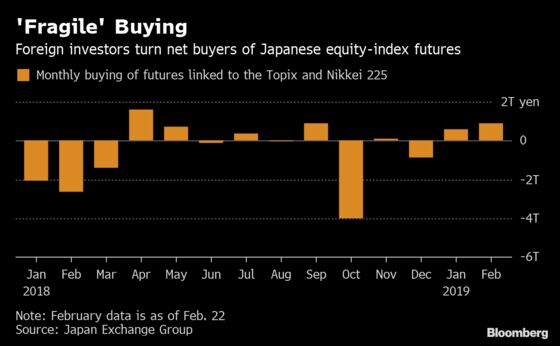

While foreigners have bought 1.48 trillion yen ($13.2 billion) of futures linked to the Topix index and the Nikkei 225 Stock Average since January, propelling the gauges higher, they’ve also offloaded 785 billion yen of cash equities, according to data from the Japan Exchange Group through Feb. 22. They were net sellers of both the contracts and stocks last year.

“What we’re seeing is a bit of an extreme scenario at play, with foreigners only buying up futures,” said Norihiro Fujito, the chief investment strategist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo.

Those buyers are short-term traders, namely hedge funds, while long-term players including pension and mutual funds keep selling, he said. This means the purchasing force is “fragile,” he added.

Which is understandable: Economic data haven’t been good lately -- the nation’s manufacturing sector contracted in February for the first time in two and a half years, while exports in January fell more than forecast. On top of that, companies including Sony Corp. and Toyota Motor Corp. have reported disappointing results, keeping appetite for Japan’s stocks at bay.

“To long-term investors, Japanese equities aren’t attractive, with fundamentals looking downwards and finances not looking good,” Fujito said. “They’re thinking it’s better to invest in the U.S. or emerging markets.”

The Topix index slipped 0.5 percent at the close in Tokyo, while the Nikkei 225 dropped 0.4 percent.

Tomochika Kitaoka, the chief equity strategist at Citigroup Global Markets Japan Inc., also views Japanese equities as “unpopular” among foreign investors these days. Instead, they are increasingly interested in other areas, adding money to China and emerging markets, he said.

“The strength of near-term reversals is coming to be seen as part of the ‘rules of the game,’ with some hedge funds actively harnessing this trend,” he wrote in a March 3 report.

Kitaoka doesn’t expect foreign selling in cash equities to be as bad it’s been, estimating it will reach roughly a third of last year’s 5.7 trillion yen. Huge buybacks from Japanese companies could support the market, while valuations are cheap, he noted. But for long-term investors, he said uncertainty will persist until Prime Minister Shinzo Abe’s term ends in 2021.

Some are more optimistic, citing the latest developments in U.S.-China trade negotiations.

A resolution to their discord would be positive for equities around the world, and “particularly for high-surplus exporting nations such as Japan, which also has a high beta to China,” said Jeffrey Halley, a senior market strategist at Oanda Corp. in Singapore. “With confidence returning in the short and medium term if an acceptable deal gets over the line, we should see foreign buyers returning to Japan’s equities in force.”

While Fujito acknowledges positive trade developments could help equities, a convincing return of foreign appetite is yet to be seen. The buying in futures “is something that takes place in a very speedy fashion, but something that can’t be sustained,” Fujito said.

To contact the reporter on this story: Min Jeong Lee in Tokyo at mlee754@bloomberg.net

To contact the editors responsible for this story: Divya Balji at dbalji1@bloomberg.net, Cecile Vannucci, Teo Chian Wei

©2019 Bloomberg L.P.