It’s ‘Game On’ for Hedge Fund Bets That Blew Up in Treasury Rout

It’s ‘Game On’ for Hedge Fund Bets That Blew Up in Treasury Rout

(Bloomberg) -- The swift arrival of the Federal Reserve on the scene as the dealer of last resort stopped a spiral in the Treasury market from turning systemic in March.

The question now is whether a gradual retreat by the central bank would create inviting conditions for the return of leveraged strategies that helped tip coronavirus-ravaged markets into chaos.

“Basis trades are game on” after recent changes to the Fed bond-buying program, according to UBS Group AG strategists including Michael Cloherty.

Such long-short styles profit from small differences in the yield between cash Treasuries and the corresponding futures, which usually move together -- except in last month’s explosion of volatility.

The breakdown of the leveraged bets contributed to a wider dislocation that sent Treasury yields climbing at exactly the time investors needed them for protection, according to regulators and dealers.

So-called basis trades seek out the cheapest-to-deliver (CTD) cash security associated with a futures contract.

But contained in the New York Fed’s weekly purchase schedule on Friday was the news that it would no longer buy these CTDs -- and that could leave the door open to a return of destabilizing basis trades.

Hedge funds burned on basis trades in March may also be drawn back into the strategy as repo markets they use to finance the transactions return to normal.

“We will be watching the futures positioning data for signs that positions are getting crowded,” Cloherty and his colleagues wrote in an April 17 note.

For now, CFTC data analyzed by JPMorgan Chase & Co. show short positions on Treasury futures -- which had swelled to almost $2 trillion at one point -- are returning to a level near their medium-term average using the z-score, a statistical measurement of the value of a data point relative to its average.

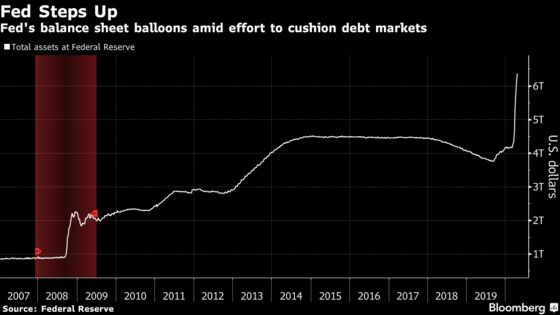

With the Fed balance sheet of more than $6 trillion ready to backstop the crisis, the central bank has been tapering weekly Treasury purchases and shifting market-making back to dealers. Tamer volatility has also expanded dealers’ balance sheet capacity by curbing risk.

“The liquidations have largely run their course,” said Jay Barry, a strategist at JPMorgan. “There’s greater dealer capacity to intermediate than there was prior to March.”

That makes a replay of last month remote despite the toll the coronavirus pandemic claims on lives and the global economy.

LTCM Echoes

It’s an open question whether relative-value strategies, which famously led to the downfall of Long-Term Capital Management in 1998, pose a risk in normal markets.

But sentiment remains fragile after the haven status of Treasuries has been tarnished in a market where fast-money quants are raising their profile. Some $1 trillion of $9 trillion in hedge fund assets are tied up in systematic strategies, according to a Bank for International Settlements report this month.

Before the Fed stepped in, the safest government debt wasn’t liquid enough to be used for margin calls, according to Bob Treue, founder and the chief executive officer at Barnegat Fund Management, a New Jersey-based hedge fund.

“In mid-March, converting Treasuries to cash became difficult,” he said.

Two-way flows are back and the Fed has put itself firmly in the role of market guardian, but that doesn’t mean it can see off every threat facing investors.

“Given things are so unprecedented now, there’s always some uncertainty that makes it hard to assume things are all better,” said Kevin McPartland, director of market structure at Greenwich Associates LLC.

©2020 Bloomberg L.P.