Wall Street Math Says This Is the Worst Quarter to Miss Earnings

It's a Mistake to Expect Earnings to Cure Market, One Model Says

(Bloomberg) -- Markets, the saying goes, hate uncertainty. But what happens when everyone thinks they know exactly what’s going to happen?

It’s a question resonating now as half of Wall Street sits waiting for earnings season to calm what has become one of the worst equity routs in two years. And while complacency is a familiar concept for crowds, there are signs lately it is showing up at a more microscopic scale.

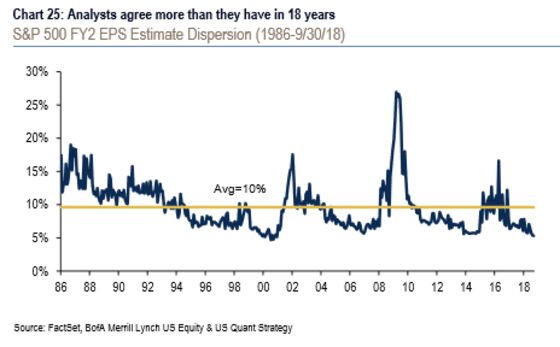

The latest concern, buried deep in the Street’s data banks, relates to high levels of unanimity around the profit forecasts for individual companies proffered by equity analysts. It’s a quantity known as estimate dispersion -- how much the highest and lowest per-share forecast varies from stock to stock. At an average of 5 percent, it’s the lowest since 2000, data compiled by Bank of America Corp. shows.

The homogenization sets stocks up for bigger swings when earnings surprise, maybe more than any time since the dot-com era, BofA predicts. With everybody expecting one thing, it will be worse when a company says something else, the logic goes.

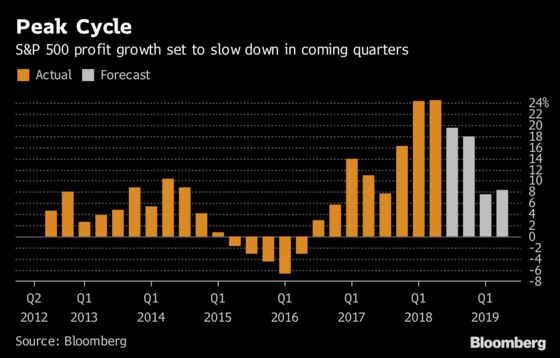

To be sure, none of this implies damage to earnings expectations in the overall market. Estimated at almost 20 percent, income growth for S&P 500 companies is poised to be among the highest of the bull market.

But it’s another wrinkle to contend with, heading into an earnings season just as measures of equity-market volatility are touching the highest levels since April. Among other worries, executives are cutting guidance at the fastest rate since at least 2010, interest rates and the dollar are rising, and companies are coping with trade tariffs and wage pressure.

“Everyone is looking at the same factor pattern and coming to the same conclusion: that the environment for stocks is good,” said Phil Orlando, chief equity market strategist at Federated Investors Inc. “But there are more stuff going on right now that’s potentially more disconcerting.”

For years corporate earnings have acted as a calming force at times of stress, and the last thing investors need now is that they become a source of volatility. Particularly as 10-year Treasury yields surge to levels not seen since 2011.

Of course, big moves aren’t necessarily bad for the market, especially when they’re up. It’s always possible that volatility confined to single stocks offsets itself and the market ends up just fine.

What’s troubling now is that there are signs the market is geared toward punishment. Stocks are falling even after better-than-expected profits. The evidence is scant -- just 22 S&P 500 companies have reported results -- but even though all but two exceeded forecasts, their stocks lost an average 2.4 percent, data compiled by Bloomberg showed.

And early results showed the size of beat is getting smaller. Maybe as a result of all the downward guidance, companies have topped analyst estimates by 3.9 percent, down from 5.2 percent in the second quarter and 6.6 percent in the first. Should the trend continue, it’s likely to feed into the prevailing fear over peak profits.

To approach the earnings-growth high water mark of 24.4 percent in second quarter, the actual increase in July-to-September profits would need to be 4.9 percentage points higher than what analysts had in their models. Companies beat estimates by an average rate of 3.6 percentage points in the last three years.

“Third quarter earnings season should wrest control of the market narrative away from interest rates and place it back on corporate fundamentals,” said Nicholas Colas, the co-founder of DataTrek Research. “The results will be good, but not as positive as earlier in the year. Thankfully, everyone knows that. We will be watching revenue growth and how analysts tweak their numbers for 2019.”

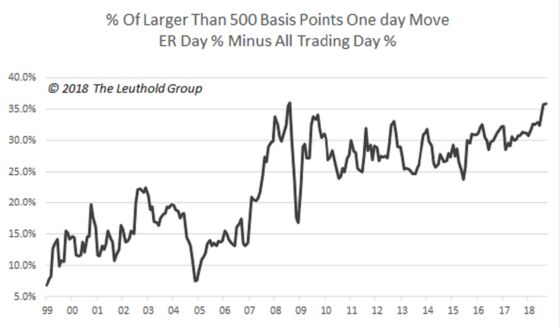

Equity swings around earnings have picked up this year. First-day reactions in individual stocks to financial results were more pronounced last quarter than any time in two years, according to data compiled by Goldman Sachs. While the firm’s strategists attributed the tremor to bad forecasts that resulted from conflicting economic forces and policies, another factor may also have been at play: too much consensus.

Perhaps it’s no coincidence that big earnings-day moves have exploded since the global financial crisis, a period when estimate dispersion has dwindled to one fifth the level seen at the 2009 peak. Over that stretch, the number of stocks swinging 5 percent or more has doubled, hovering near a record, according to Leuthold Group that looked at how shares reacted on earnings days.

“Clustered estimates typically drive a bigger stock reaction from beats and misses,” Savita Subramanian, BofA’s head of equity and quantitative strategy, wrote in an Oct. 8 note. She expects a “modest” 1 percent beat for this reporting season.

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.