It's a ‘Golden Age’ for Short-Volatility Trades

It's a ‘Golden Age’ for Short-Volatility Trades

(Bloomberg) -- Traders going all-in on the U.S. rally may be better off shorting volatility than buying stocks, as the strategy flashes bullish signs evoking the “golden age” of 2017.

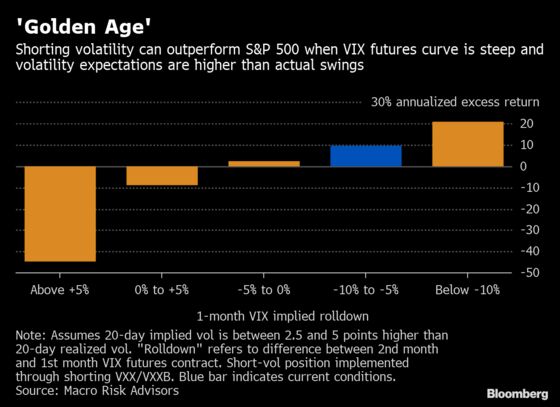

Macro Risk Advisors reckons selling price swings on the S&P 500 in today’s calm markets can now deliver stronger risk-adjusted returns than going long the index -- a reversal of this year’s trend.

After outsize losses for short-vol bets over the past 18 months, it’s not for the faint of heart. But technical factors in the underbelly of the derivatives market are giving the trade extra juice.

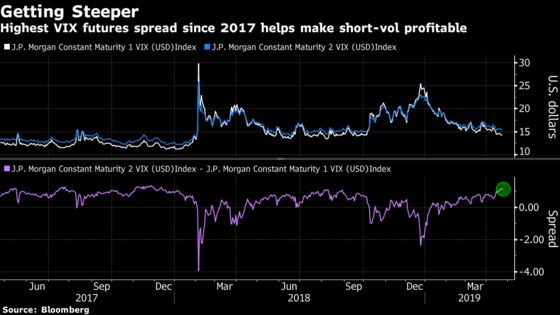

First, the futures curve for the Cboe Volatility Index, or VIX, this month has assumed a shape more favorable for those betting against stock gyrations. And second, an old friend: the persistent gulf between higher expected price swings versus what comes to pass.

Together, it’s enough to spur the fast money to up wagers against volatility, even as Wall Street strategists sound the alarm on illiquidity and late-cycle risks.

“Today, the market and economy look different” from 2016 and 2017, Vinay Viswanathan, MRA strategist, wrote in a recent note. “Metrics, though, are starting to resemble the ‘Golden Age’ of VIX selling.”

A dovish Federal Reserve, agreeable valuations and easing trade tensions have all damped market swings as the S&P 500 flirts with records -- a Goldilocks-like climate for volatility selling. The VIX was trading near 14 at 10:48 a.m. New York time, below its one-year average.

While the benchmark U.S. gauge has managed to produce better returns adjusted for risk so far in 2019, as conditions endure the calculus on paper is poised to flip, according to Viswanathan in New York.

Thanks in part to a slump in the VIX, the futures curve for the gauge of expected U.S. price swings has steepened, in particular at the front-end. “You can think of it like a clothesline -- you pull one end down and the rest goes down with it at a gradient,” Viswanathan said in a message.

Known as the rolldown, it’s one of the traditional engines of the short-volatility trade. Since expectations of price swings are typically higher than current levels, as long as benign conditions endure the contracts look poised to lose value as they converge to the spot price.

According to calculations by MRA, shorting a popular long volatility note, the iPath Series B S&P 500 VIX Short-Term Futures, or VXXB, in current conditions suggests a 9.6 percent annualized outperformance compared with a long position on the S&P 500.

Of course, the returns spitted out in MRA’s model are theoretical, exclude borrowing costs and only battle-ready traders will have the stomach to risk losses if volatility spikes. Short-volatility hedge funds lost 13 percent in their worst-ever performance last year as unexpected moves in February and December blew the lid off these strategies.

Still, the technicals behind MRA’s trading tip helps explain why net short positions in the futures market are a whisker away from record highs.

By one measure, the front end of the curve is now the steepest since 2017. That makes it more expensive for long-vol products like VXXB to maintain exposures, pulling down its price -- and rewarding short-sellers along the way.

Risk Premium

Adding to the tailwind is the so-called volatility risk premium, or the compensation options sellers demand for providing protection against unexpected swings.

As time passes and markets remain calm, those options prices are likely to decrease. Since VIX futures represent a strip of options, they can offer this type of premium -- meaning the contracts tend to reliably lose value, causing VXXB to fall further.

Such trades come with a health warning, of course.

“Most of the time shorting vol works but you want to pick your spots and be careful with the amount of risk you take in the trade,” Pat Hennessy, head trader at IPS Strategic Capital, tweeted.

But as the bull market powers ahead, yield-hungry investors are placing their faith in the twin engines of the short-volatility complex -- the rolldown and the risk premium -- even as recent history underscores the perils of the trade.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.