Is Now a Bargain Hunter’s Moment in the U.K.?: Taking Stock

Is Now a Bargain Hunter’s Moment in the U.K.?: Taking Stock

(Bloomberg) -- Want the lowdown on European markets? In your inbox before the open, every day. Sign up here.

There is still a very understandable mixed sentiment towards U.K. equities. Prime Minister Theresa May was dealt another blow yesterday as she won’t be allowed to present the same deal to Parliament for a third time. A delay increasingly seems the most likely outcome, though it’s anyone’s guess of how long a wait we’re in for.

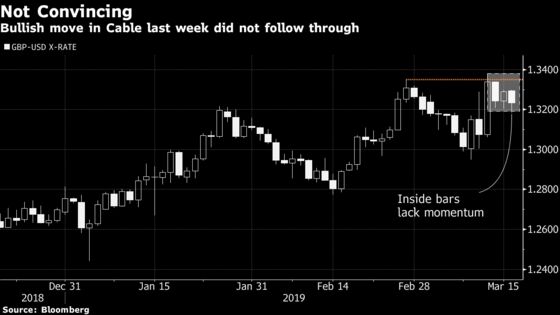

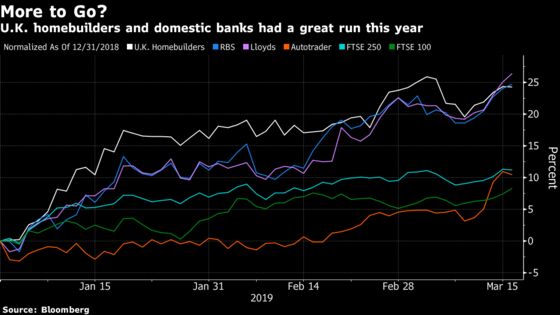

And yet, amid the uncertainty, more voices have been rising in favor of British stocks. With a clear outperformance of domestic shares since January, it’s fair to wonder what’s left to play, especially with the pound lacking momentum.

Generally speaking, investors were receptive to the idea that U.K. tail risks have receded, Berenberg strategists wrote in a note published yesterday, citing the expectations that outcomes including a hard Brexit and a Corbyn government are less likely. Taking into account that the U.K. economy is seen as being fundamentally in good shape, the country can look appealing, they said.

JPMorgan strategists continue to find U.K. domestic names attractive. They base their view on valuation and leverage grounds, highlighting that since 2011, the leverage of their domestic basket has come down by 16%, while FTSE 100 leverage has increased by 43%. They name Lloyds, Persimmon, Land Securities and Barratt as particularly attractive plays.

The view on domestic stocks is shared by Aruna Karunathilake, Fidelity International U.K. Select Fund Portfolio Manager. It’s "time to be brave" and buy undervalued U.K. domestic stocks after investors shunned them because of Brexit, she wrote, listing Autotrader and Lloyds as examples of market leaders trading at a significant discount to international peers. Karunathilake added that the view on U.K. stocks was now close to the point of "maximum fear," and preferred to stick to fundamentals rather than trying to guess the next twists and turns of the macro environment.

By contrast, the view on exporters is still fairly negative. JPMorgan strategists anticipate the pound will rise further this year, which will weigh on the FTSE 100. This relatively bleak picture for exporters is "confirmed" by a lack of technical momentum in the FTSE 100 futures. The contract has been consolidating below its 200-day moving average over the past month and has so far failed to breakout. On the other hand, the cash index broke its 200-day moving average yesterday as the pound dropped.

What’s next then? Citi strategists raise a good point: highlighting that if a deal was to be agreed on within the next few months, the option to reverse Brexit would be gone, but it would be unlikely to lift the uncertainty. In fact, negotiations about long-term trade relations with the EU have not even started, so economic uncertainty and political tensions would remain very high, they concluded.

Ahead of the open, the pound has brushed off yesterday’s news, recouped losses and Euro Stoxx futures are trading up 0.1%.

- Watch the pound and U.K. stocks as Prime Minister Theresa May looked set to seek a long extension to the U.K.’s European Union membership after the House of Commons speaker torpedoed her plan to win Parliamentary approval for her deal to leave the bloc.

- Watch French banks after the country’s high -- and rising -- private debt burden has worried regulators enough that they are forcing banks to put aside more capital to support lending in a downturn.

- Watch IPOs staging a comeback with Ride-hailing giant Lyft aims to raise as much as $2.1 billion in its U.S. listing, while Italian payments firm Nexi is targeting a Milan IPO of up to 2.7 billion euros. Twelve other companies set terms for their offerings Monday, including Precision Biosciences and Tufin Software Technologies, the data show.

COMMENT:

- “Investors in European equities face a short-term tactical decision on the direction of a risk/value trade,” Bernstein strategists write in a note. “There are also a number of significant features of market structure that need to be navigated: factor correlation is high leading to unusually large gross factor exposures; valuation dispersions are unusually wide; despite a market rally sentiment that is subdued (ie traditional investors are not buying the market).”

COMPANY NEWS AND M&A:

- Deutsche Bank Said to Weigh Giving Up Office Space in Hong Kong

- Celyad Sees Updates From Phase 1 Think, Deplethink Trials in 1H

- Wacker Chemie Sees 2019 Ebitda 10%-20% Below Year Ago Levels

- Ferrovial, Acciona Bid for Real Madrid Contract: Expansion

- Iliad Full-Year Revenue 1.0% Below Estimates

- Solidium Acquires 5.1% of Shares in Nokian Renkaat for EU205 Mln

- Iberdrola Mulls Sale of Torre Auditori in Barcelona: Expansion

- Washtec Full-Year Dividend Per Share Misses Estimates

- BKW Full-Year Dividend Per Share Beats Estimates

- FDA Backs Roche’s Tecentriq, Chemotherapy Combo for Lung Cancer

- Vetropack Full-Year Sales Beat Highest Estimate

- Rio Tinto Must Face SEC Suit Over Coal Assets, Judge Rules

- Schaeffler Debt Swaps Whipsaw Amid Concerns Over Financing Units

NOTES FROM THE SELL SIDE:

- Morgan Stanley says Informa can look ahead to a better remainder of 2019, with the UBM merger boosting margins, upgrading shares to overweight from equal-weight, price target 840p. The bank says the company looks lowly rated versus peers.

- Citi upgrades Hikma to buy, saying the FTSE 100 member deserves to trade at a premium to the EU pharma industry and U.S. generics, given its superior growth. Citi’s earnings estimates beyond 2021 are 15%-60% ahead of consensus.

- Morgan Stanley set Experian at underweight, with “punchy” valuation prompting call to take profits. The broker said stock has outperformed peers by about 30% over past year, but EPS is only up 5% on relative basis; “valuation has run ahead of fundamentals” and additional outperformance needs upgrades.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 383 (trend line); 392.7 (July high)

- Support at 379.9 (23.6% Fibo); 369.3 (200-DMA)

- RSI: 73.4

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,466 (23.6% Fibo); 3,596 (May high)

- Support at 3,349 (August low); 3,315 (38.2% Fibo)

- RSI: 75.1

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Baloise upgraded to overweight at JPMorgan; PT 190 Francs

- Deutz upgraded to buy at Kepler Cheuvreux; PT 8 Euros

- Groupe Gorge upgraded to hold at Kepler Cheuvreux; PT 11 Euros

- Grupo Catalana Occidente raised to overweight at JPMorgan

- Hikma upgraded to buy at Citi

- Informa upgraded to overweight at Morgan Stanley; PT 8.40 Pounds

- K+S upgraded to buy at Commerzbank; Price Target 21.50 Euros

- Leonardo upgraded to buy at AlphaValue

- Lufthansa upgraded to add at AlphaValue

- Telekom Austria upgraded to buy at HSBC; PT 8.05 Euros

DOWNGRADES:

- Commerzbank cut to sector perform at RBC; Price Target 8 Euros

- Commerzbank downgraded to sell at Nord/LB; PT 6.35 Euros

- DWS downgraded to hold at DZ Bank; Price Target 28 Euros

- DWS downgraded to hold at Kepler Cheuvreux; PT 29.70 Euros

- Leoni downgraded to underperform at MainFirst; PT 15 Euros

- Marshalls downgraded to hold at Berenberg

- Orsted downgraded to neutral at Goldman; PT 525 Kroner

- Shell downgraded to sector perform at RBC; PT 27.50 Pounds

- Swiss Life cut to neutral at JPMorgan; Price Target 440 Francs

- Swiss Re downgraded to hold at SocGen; PT 100 Francs

- Technotrans cut to hold at Pareto Securities; PT 31.80 Euros

- Wacker Neuson downgraded to hold at Commerzbank; PT 25.80 Euros

INITIATIONS:

- Barry Callebaut reinstated equal-weight at Barclays

- Chr. Hansen rated new overweight at Barclays; PT 800 Kroner

- CompuGroup rated new outperform at MainFirst; PT 63 Euros

- Experian reinstated underweight at Morgan Stanley; PT 18 Pounds

- Vivo Energy rated new buy at Renaissance Capital; PT 1.70 Pounds

MARKETS:

- MSCI Asia Pacific up 0.9%, Nikkei 225 down 0.1%

- S&P 500 up 0.4%, Dow up 0.3%, Nasdaq up 0.3%

- Euro up 0.1% at $1.1348

- Dollar Index down 0.1% at 96.43

- Yen up 0.17% at 111.24

- Brent little changed at $67.6/bbl, WTI down 0.2% to $59/bbl

- LME 3m Copper up 0.5% at $6457.5/MT

- Gold spot up 0.3% at $1307/oz

- US 10Yr yield down 1bps at 2.6%

MAIN MACRO DATA (all times CET):

- 8:30am: (EC) Bloomberg March Eurozone Economic Survey

- 9am: (SP) 4Q Labour Costs YoY, prior 1.9%

- 10am: (IT) Jan. Trade Balance Total, prior 3.66b

- 10am: (IT) Jan. Trade Balance EU, prior -613m

- 10:30am: (UK) Feb. Claimant Count Rate, prior 2.8%

- 10:30am: (UK) Feb. Jobless Claims Change, prior 14,200

- 10:30am: (UK) Jan. Average Weekly Earnings 3M/YoY, est. 3.2%, prior 3.4%

- 10:30am: (UK) Jan. Weekly Earnings ex Bonus 3M/YoY, est. 3.4%, prior 3.4%

- 10:30am: (UK) Jan. ILO Unemployment Rate 3Mths, est. 4.0%, prior 4.0%

- 10:30am: (UK) Jan. Employment Change 3M/3M, est. 120,000, prior 167,000

- 11am: (EC) Jan. Construction Output MoM, prior -0.4%

- 11am: (EC) Jan. Construction Output YoY, prior 0.7%

- 11am: (EC) 4Q Labour Costs YoY, prior 2.5%

- 11am: (GE) March ZEW Survey Current Situation, est. 13, prior 15

- 11am: (GE) March ZEW Survey Expectations, est. -11, prior -13.4

- 11am: (EC) March ZEW Survey Expectations, prior -16.6

--With assistance from Hanna Hoikkala.

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Celeste Perri

©2019 Bloomberg L.P.