Hard as It Is, Frackers Should Ignore Iran

(Bloomberg Opinion) -- Oil has begun pricing in the Middle East’s next explosion (albeit arguably not enough). Even as restraints pop there, though, discipline appears to be holding up in one crucial corner farther away: the shale patch.

The prospect of a conflict-inspired jump in oil prices is, in purely economic terms, like a glass of water in the desert for U.S. energy stocks. The sector closed 2019 as the worst performer of the year and the decade; it has begun 2020 in the green, at least. The short story is that investors have wised up to the benefits of higher oil prices flowing disproportionately to insiders and (by way of drilling budgets) contractors. Hence, exploration and production companies have tried to reset the relationship with investors on a platform of disciplined spending, lower leverage and higher returns. Higher oil prices provide temptation to backslide on this.

Thus far, however — and it is very early days in this current crisis — the message from financial markets is: Backslide at your peril.

Not so long ago, an event like Thursday evening’s assassination of Iranian General Qassem Soleimani would have set off a frenzy in oil prices and the stocks of companies producing the stuff. Yet crude oil is up only a bit more than 4%, while E&P stocks have risen less than 2%. Shares of oilfield services stocks, which would tend to benefit first from any backsliding on drilling budgets, are up even less.

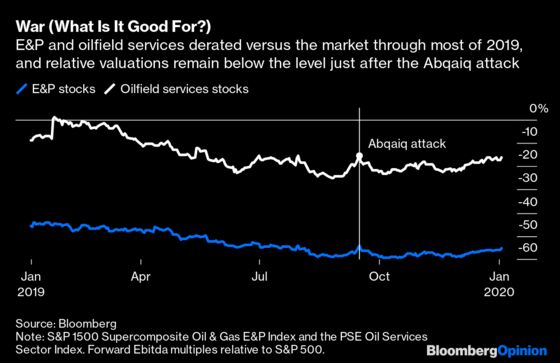

Investors may be cautious about taking a definitive view on how things will play out between the U.S. and Iran. Geopolitical events have a habit of spurring oil-price spikes that fade quickly, not least after the attacks on Saudi Arabia’s critical Abqaiq facility in September. When it comes to E&P stocks, that caution is compounded by the industry’s past performance. Indeed, it is illustrative to look at what has happened to valuation multiples now versus September.

Energy stocks, alongside oil, had already enjoyed gains in the month leading up to Soleimani’s death. This December rally was broad-based, resting largely on hopes of a thaw in another war (the trade one). Hence, despite valuation multiples rising by roughly 0.5-1 turn of Ebitda, on average, for E&P and services stocks, their discounts to the wider market barely changed.

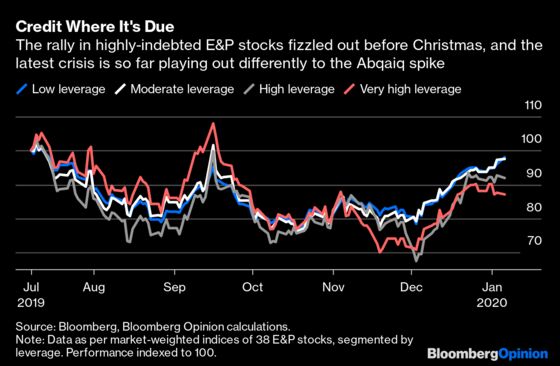

Investors would prefer any geopolitical windfall to go into their own pockets or repairing balance sheets. I wrote in late November about the gap that had opened up between heavily indebted E&P companies and less-levered peers in terms of stock-price performance. While all benefited from the December rally, the lower-leveraged names are performing better so far this year (see the original column for details on these custom indices ):

Similarly, the average spread on energy high-yield bonds had already dropped by roughly 150 basis points from its early December peak. While it tightened a little further on Friday, it remained above 660 points, notably wider than where it went in the immediate aftermath of the Abqaiq attack. It is both telling, and logical, that Occidental Petroleum Corp., which blew a hole in its balance sheet and reputation with last year’s acquisition of Anadarko Petroleum Corp., announced on Monday morning it had taken the opportunity to hedge more of its production (and will deconsolidate the debt of its pipeline subsidiary, to boot).

Even if our worst (or semi-worst) fears concerning the Middle East are realized over the next several weeks, by the time quarterly calls begin, E&P firms would do best to mostly ignore the oil market’s gyrations. Investors, like most of us, would prefer to focus on stability and the stuff we can control.

The four groups in the chart areas follows. Very high leverage (net debt >3x Ebitda) comprising Antero Resources, Chesapeake Energy, Comstock Resources, EQT, Laredo Petroleum, Noble Energy, Oasis Petroleum, Range Resources. High leverage (2-3 x Ebitda) comprising Apache, Callon Petroleum, Carrizo Oil & Gas, CNX Resources, Matador Resources, QEP Resources, Southwestern Energy. Moderate leverage (1-2x Ebitda) comprising Berry Petroleum, Centennial Resource Development, Cimarex Energy, Continental Resources, Diamondback Energy, Diversified Oil & Gas, Jagged Peak Energy, Marathon Oil, Murphy Oil, Northern Oil and Gas, Parsley Energy, PDC Energy, SM Energy, SRC Energy, Talos Energy, W&T Offshore, WPX Energy. Low leverage (<1x Ebitda) comprising Cabot Oil & Gas, Devon Energy, EOG Resources, Magnolia Oil & Gas, Pioneer Natural Resources, Riviera Resources.The aggregate data presented are weighted by market cap in each group. Four companies (one in each group) have been removed due to their outsized weighting. They are (in order of leverage from high to low): Occidental Petroleum, Concho Resources, Hess, ConocoPhillips.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.