IPO Mania Sweeps Over Robinhood Crowd and Stokes a 111% Rally

IPO Mania Sweeps Over Robinhood Crowd and Stokes a 111% Rally

(Bloomberg) -- An interesting thing keeps happening in the American stock market. Lately, when ownership of young companies passes from the institutions who nurtured them into the much broader arms of the investing public, their valuations double.

It happens fast. After its price was set with professional fund managers the night before, food-delivery service DoorDash Inc. surged 86% in its public debut Wednesday. Software firm C3.ai Inc. jumped 120%. Airbnb Inc. more than doubled a day later, the home-rental company seeing its value surpass $100 billion. The 2020 return in an index of IPO stocks? 111%.

While initial offerings are often occasions for appreciation, this year has been different, with first-day rallies almost three times bigger than the average of the last 40 years. While Federal Reserve stimulus may explain some of the frenzy, it’s hard not to also consider who rules public exchanges these days: the Robinhood posse.

“There is no doubt that the emergence of a much larger cohort of retail investors-slash-traders are moving markets,” said Art Hogan, chief market strategist at National Securities Corp. “There seems to be an entire subculture of people that sort of follow the same things, talk to each other on social media and drive enthusiasm for individual issues. And sometimes it makes no fundamental sense to anybody.”

In looking for comparisons to similar market episodes, some Wall Street veterans point to the last time individuals took over from institutions in setting the price for newly public companies: the dot-com bubble of the late 1990s. While plenty of them got rich in that episode, many more were burned by the bursting of that bubble and a bear market that lasted years. It raises the question in many minds: Is a similar phenomenon occurring today? Phrased differently: who’s got the valuation call right, the amateurs or the pros?

These days, individual investors make up a fifth of equity trading volume, second only to infrastructure providers like market makers and high-frequency traders, according to Bloomberg Intelligence. Stuck inside, their obsessions in 2020 have been many and varied, everything from airlines and cruise stocks to bankrupt companies and bullish options. Now it’s IPOs, with new issues the hot new get-rich ticket.

Retail investors drove a large portion of the early activity around Airbnb, according to people familiar with the matter. Less than 24 hours after beginning to trade on public exchanges, the company had already cracked a list of users’ 100 most popular stocks on the Robinhood app. Shares of DoorDash and Airbnb immediately landed on the leader board of top orders among online traders tracked by Fidelity Investments.

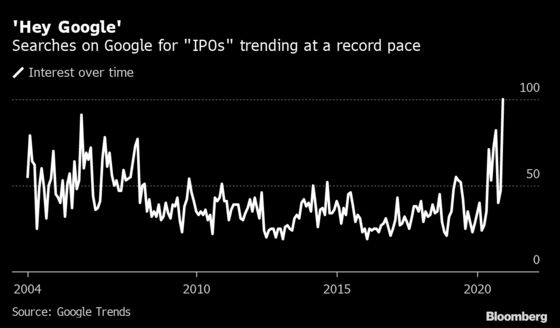

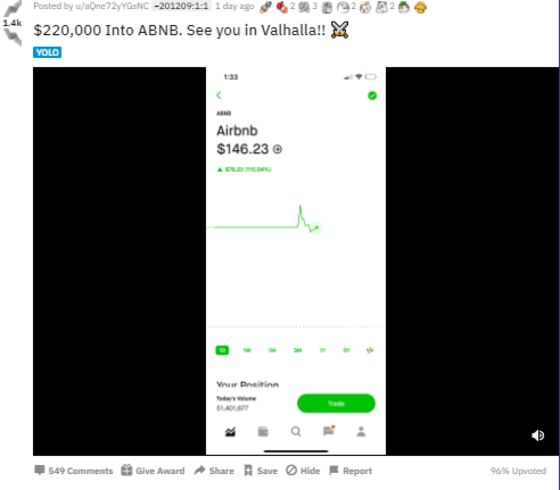

The number of searches for “IPOs” on Google spiked to the highest level in at least 16 years. Meanwhile, investors poured a record amount of cash into an exchange-traded fund tracking newly public companies and a post on Reddit’s Wall Street Bets forum read “$220,000 Into ABNB. See you in Valhalla!!”

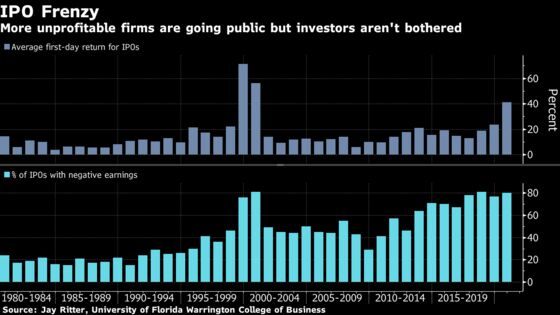

The average first-day return for operating-company IPOs was 41% in 2020, according to Jay Ritter, professor of finance at the University of Florida’s Warrington College of Business.

Among some 50 companies that had been backed by private equity and went public this year, their total worth jumped 660% on the first day of trading from levels indicated in their latest round of private funding, according to data compiled by PrivCo and Bloomberg.

Pricing Versus Promise

Consider Airbnb. Now with a market capitalization around $100 billion, Airbnb’s value is more than five times as high as its worth was implied in a debt funding round at the height of the pandemic.

There’s reason institutions such as venture capital firms and private equity investors might have different views than the masses on valuation these days, as well as the investment bankers who set the IPO price. One factor is the liquidity premium, or the ease with which shares can be bought and sold after a public listing. Another is that when pricing an IPO, long-term investors may be more inclined to consider earnings and competition -- standards that haven’t always seemed to govern the “stocks always go up” retail crowd.

“Some investors are deciding to hold based on fundamental analysis, trying to figure out how much Airbnb is really worth,” said Ritter. “And others are paying attention to that, but also playing momentum strategies. They might say, ‘I think they’re overvalued but I believe in the great fool’s theory. I think it’s going to go up even higher and I can sell my shares by waiting to sell to a greater fool later on.’”

Still, it can be hard in stodgier corners of Wall Street to understand why DoorDash, for example, a seven-year-old, unprofitable food delivery company with established competitors should see its market-cap balloon to $60 billion with an IPO trading pop -- almost four times more than its last private-funding round and more valuable than companies including Kraft Heinz Co., Marriott International Inc., and Twitter Inc.

“Is there a bubble going on? It’s difficult to come up with a plausible valuation today that should be much higher in public markets than it had recently in the private market,” Ritter added. “There is a mistake going on right now with the valuations and some of these companies.”

‘Use Common Sense’

That’s why Michael Holland, chairman at Holland & Co., wants no part in the action, saying that investors who piled into DoorDash and Airbnb are bound to lose their money.

“You simply have to use common sense and step in and say, ‘we’re not going to participate in this craziness,’” he said in an interview on Bloomberg Radio and Television.

Unlike in dot-com days, when companies with less than a year of operating history sometimes went public, the single-second booms of today are occurring in relatively mature firms whose sponsors have had years to arrive at a valuation. Then again, there’s something similar to those days, too: many are losing money.

Some 80% of companies that went public this year were unprofitable in the 12 months prior to the IPO, according to University of Florida’s Ritter. That’s more than any time in the past four decades, except for 2000 and 2018. In those two years, 81% of IPOs came out with negative earnings.

National Securities’ Hogan remembers the Internet bubble well, and while he says it’s almost too easy to draw a comparison between then and now, valuations of today and the number of new issues still pale in comparison. Still, it’s likely the stampede of risk-taking individual investors bidding share prices into the stratosphere ends in a similar way.

“That doesn’t tend to end well historically, but for the time being it’s the nature of the beast,” he said. “But it didn’t take long after 2000 to see that cohort of day trader types fade into the sunset, not really come back until really March and April of this year when things exploded again.”

©2020 Bloomberg L.P.