Investors Suing JPMorgan May Redefine the Leveraged Loan Market

Investors Suing JPMorgan May Redefine the Leveraged Loan Market

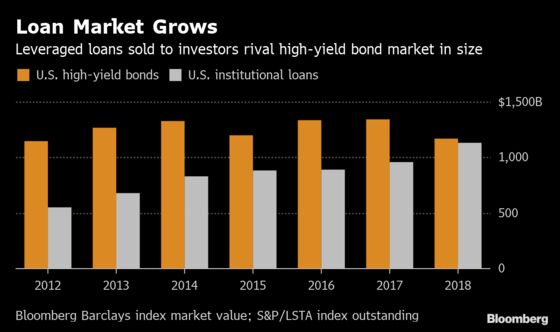

(Bloomberg) -- A group suing JPMorgan Chase & Co. and other Wall Street banks over a loan that went sour four years ago is alleging the underwriters engaged in securities fraud. If successful, the lawsuit could radically transform the $1.2 trillion leveraged lending market.

The defendants say there’s one key problem -- unlike bonds, loans aren’t securities. As a result, they’ve filed a petition asking the court to dismiss the suit on those exact grounds.

The debate strikes at the heart of the leveraged loan market, which in recent years has come to look markedly similar to the higher-profile one for junk-rated bonds. The standardization of loan terms, the deterioration of covenants and the growth of secondary trading continue to blur the lines between the two. Should the plaintiff ultimately prevail, it would dramatically alter how American companies raise debt, according to two industry groups that filed a brief supporting the defendants’ argument last week.

“There are absolutely enormous market consequences if a court determines that leveraged loans are securities,” said J. Paul Forrester, a partner at law firm Mayer Brown who’s not involved in the litigation. “Leveraged loans and lenders would be potentially subject to the same offering and disclosure requirements as securities and would face the same regulatory oversight and enforcement consequences.”

The suit stems from a $1.8 billion loan that JPMorgan and others arranged for Millennium Health LLC -- then owned by private-equity firm TA Associates -- and sold to investors in 2014. Within a matter of months, lenders saw the value of their loan plunge as the company disclosed that federal authorities were investigating their billing practices. Millennium agreed to pay $256 million to resolve the probe, and would go on to file for bankruptcy.

JPMorgan knew U.S. officials were investigating Millennium when it sold the loan, but didn’t tell investors who were about to buy the debt, Bloomberg reported in 2015. The bankers did not provide the information because Millennium told them it wasn’t material at the time.

“Styled as ‘leveraged loans,’ the debt obligations that defendants sold to the investors back in April 2014 have all the attributes of and, in fact, constituted credit agency-rated and tradeable debt ‘securities,’” the lender trustee wrote in the 2017 suit. As such, the defendants are liable “for sponsoring the materially false presentation of Millennium’s financial condition and business practices.”

Units of Bank of Montreal, Citigroup Inc. and SunTrust Banks Inc. are also listed as defendants in the suit. Bank of Montreal didn’t respond to requests seeking comment on the lawsuit, while the other two declined to comment, as did JPMorgan and a representative for the lenders’ trustee.

“The sophisticated entities that lent Millennium money now try to classify the loan as a ‘security’ and the loan syndication as a ‘securities distribution’ in an attempt to manufacture a securities fraud claim where none is viable, and to avoid the express language of the contracts into which they willingly entered,” JPMorgan and Citigroup wrote in a memorandum last month.

CLO Chaos

No one is saying that a fundamental transformation of the leveraged loan market is imminent. A court ruling in favor of the plaintiff would likely face numerous appeals as the decision works its way through the courts.

Yet if the courts ultimately decide that syndicated term loans are in fact securities, the repercussions would be significant and widespread, according to the Loan Syndications and Trading Association and the Bank Policy institute.

First off, arranging loans would become more cumbersome and costly amid more stringent disclosure requirements. A slower process would deprive borrowers of quick access to capital, while some may shy away from obtaining financing rather than make public confidential information, according to their brief.

And the market for collateralized loan obligations -- which provide the bulk of leveraged loan funding -- would be thrown into chaos, they wrote. Banks are key buyers of CLOs, but Volcker Rule restrictions bar them from investing in CLOs that own securities. Were loans deemed securities, banks could be forced to offload about $86 billion in existing CLO holdings in the absence of regulatory relief.

“A major disruption in the CLO market would risk reducing that flow of capital -- which is a vital resource for a wide spectrum of American businesses -- to a trickle,” the industry groups wrote. “Cutting off an important source of capital could have serious consequences for leveraged companies, as well as significant ripple effects throughout the economy.”

‘Wreak Havoc’

Still, there’s a growing chorus warning that the loan market is becoming too risky amid little oversight. The Federal Reserve addressed the perils of leveraged lending in its bi-annual financial stability report this week, echoing the International Monetary Fund, the Bank of England, and others. The Securities and Exchange Commission’s Robert Jackson Jr. said last month the regulator may need more power from Congress to police hazards manifesting in the market.

Despite growing similarities between leveraged loans and junk bonds, the two markets maintain notable distinctions.

Syndicated loans are only marketed to qualified, accredited investors, for starters. They’re typically secured by a lien on assets, making them less risky and lower yielding than a comparable bond. They almost always pay a floating coupon, and have more flexible prepayment options than bonds.

Most notably, offering memorandums don’t provide the same level of financial disclosure as found in bond prospectuses, and syndicate participants have historically relied on confidential, non-public information when determining whether to lend.

The defendants argue the investors knew this going into the transaction.

“A lender that becomes part of a syndicate does so on the express understanding that it is responsible for conducting its own due diligence,” the industry groups wrote in the brief. “Declaring syndicated term loans to be securities would upend the expectations of borrowers and lenders and wreak havoc in the large, and vitally important, market for those loans.”

The plaintiff must file its opposition to the motion to dismiss by May 31.

The case is Kirschner, v. JP Morgan Chase Bank, N.A. et al, 1:17-cv-06334-PGG, U.S. District Court in the Southern District of New York.

To contact the reporter on this story: Lisa Lee in New York at llee299@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Boris Korby, Steve Stroth

©2019 Bloomberg L.P.