Investors Expect No Relief on the Other Side of U.S. Midterms

Investors warn that the widely expected outcome of a divided Congress may not be fully baked into asset prices.

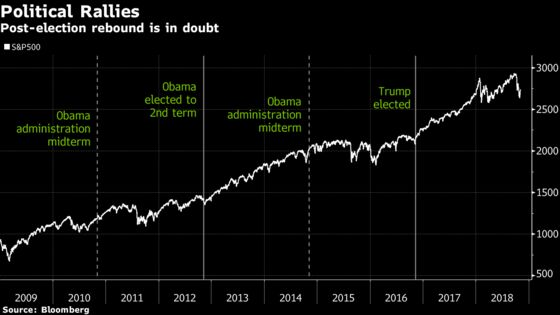

(Bloomberg) -- After the U.S. midterm elections, campaign rallies will take a welcome hiatus. Risk-asset rallies could also be harder to come by.

Investors warn that the widely expected outcome of a divided Congress may not be fully baked into asset prices. But their views on the potential impact differ depending on where they’re sitting.

For those outside the U.S., trade is front and center. China’s yuan is particularly exposed, as shown by its latest surge on talk of progress toward a deal. American investors are more focused on the chances of increased government spending, which could push the economy into overdrive, boost Treasury yields and in turn sink stocks. No matter where they are, few expect the recovery in risk appetite that typically follows midterm elections.

The consensus view -- that Democrats will flip the House and Republicans retain the Senate -- is seen as ushering in political gridlock that could slow growth. But even with what some view as the most favorable outcome for risk assets -- a GOP sweep -- investors such as Rich Weiss at American Century Investments don’t expect a repeat of the lift-off that followed the 2016 U.S. election.

“I can’t believe you’d see the same magnitude of the upswing in stocks or the longevity,” said Weiss, chief investment officer of multi-asset strategies. “We’re in a much different environment two years later, with the monetary environment, the spending we’ve already done on the tax cuts, and the effect potentially of the tariffs -- and the specter of inflation looms.”

The risk of inflation amid record supply is why his fixed-income colleagues see long-term U.S. yields rising. They favor inflation-linked securities and international credit markets. For his part, Weiss switched to value from growth stocks earlier this year, on the view that fiscal stimulus was focused too narrowly on corporate tax cuts and couldn’t sustain the rally in shares.

Trading Places

International investors are more attuned to what the midterms mean for trade, as the U.S. president focuses on China as the centerpiece of a global renegotiation that’s weighed on export-dependent economies.

“There is a school of thought that if the Democrats do well in the midterms, then markets may reprice the risk around China and also emerging markets,” said Ilan Dekell, Sydney-based head of macro for global fixed income at AMP Capital Investors Ltd.

The onshore yuan just had its biggest rally since 2007 on news that President Donald Trump wants to reach a trade deal with China this month, though for some FX strategists it was too early to call a turning point.

Many market participants see a divided Congress benefiting the yuan, according to a survey by Standard Chartered. But those closer to the action in Asia aren’t convinced this scenario would curb Trump’s protectionist impulses.

Bipartisan Push

Dekell considers the pressure on China to be bipartisan.

“Either way, I don’t think those problems go away even over a one-year time frame,” he said.

Investors should be wary of overemphasizing U.S. politics as a catalyst, said Hannah Anderson, a global market strategist at JPMorgan Asset Management in Hong Kong. For her, China’s economy and trade with non-U.S. partners are key drivers of the yuan, along with U.S.-China interest-rate differentials.

“A lot of investors here seem to be treating the U.S. midterm election results as a bellwether of what’s going to happen to U.S.-China trade -- which it is not,” she said.

Tension Sustained

In London, money manager James Athey at Aberdeen Standard Investments is positioned for trade tensions to continue supporting the dollar versus the euro and some commodity-linked currencies. The greenback is up about 5 percent versus the euro in 2018.

Even with a Democrat-led House, “much can be done via executive order,” Athey said in an email interview.

One overarching question is how Treasuries will fare in the new political landscape. Even as the Fed signals further rate hikes, many investors, including Dekell’s AMP, are using Treasuries to hedge against any weakness in global growth and assets such as stocks and emerging-market debt.

Akira Takei, a global fixed-income fund manager at Asset Management One Co. in Tokyo, expects more equities declines, and U.S.-China trade tensions are turning him back to U.S. government bond markets.

“There’s a chance of a turnaround in Treasuries,” he said. “So I’m taking more duration risks,” focusing on five- to 10-year maturities.

Haven assets are also subject to policy risks. Any increase in government spending after the midterms could make it harder for the Fed to restrain inflation. And Greg Staples, co-head of fixed income at DWS, says the expanding federal deficit is a concern for debt investors, especially should growth cool.

Deficit Fear

“If we see a bit of a slowdown in the economy I suppose that revenues are going to decline a bit more,” he said. “So that deficit I think will potentially spook the markets.’’

Weiss at American Century sees a broader risk -- to the economy and risk assets -- from a midterm result that pushes up benchmark borrowing costs.

This election stands out for him because he sees the fiscal debate upending traditional market behavior. While a divided Congress has historically supported risk assets -- bringing gridlock that adds to certainty around the investment landscape -- this time it could wind up depressing stocks.

Investors may have to adjust to “the possibility that there’s no more candy being passed out from the White House,” Weiss said.

--With assistance from Benjamin Purvis and Masaki Kondo.

To contact the reporters on this story: Emily Barrett in New York at ebarrett25@bloomberg.net;Ruth Carson in Sydney at rliew6@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Jenny Paris

©2018 Bloomberg L.P.