Investors Dump Hedges on Junk Bonds Even as Europe Defaults Loom

Investors Dump Hedges on Junk Bonds Even as Europe Defaults Loom

(Bloomberg) -- Investors are sitting astride the largest junk bond market in Europe’s history without a rainy-day fund. Even credit bulls worry that may not be such a good idea.

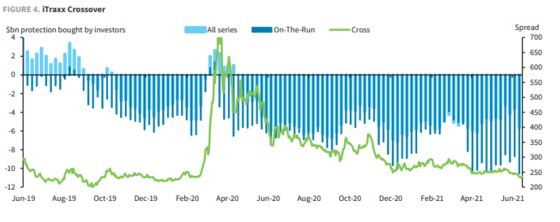

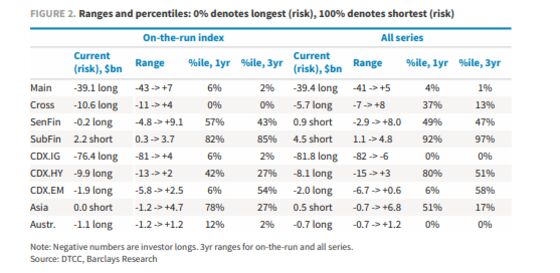

Hedges on the Markit iTraxx Crossover index were effectively neutralized after investors jettisoned $1.8 billion of credit-default insurance in the week ending June 11, according to analysis by Barclays Plc. That makes positioning the most bullish -- and exposed to risks -- as it’s been in a year.

There are many reasons to be optimistic about bonds of risky companies. Central banks continue to prop them up by ensuring easy and cheap access to credit markets while a global growth rebound will feed corporate revenues, making it easier to carry large debt loads.

But there are just as many reasons to worry. Rates are headed up as inflation comes roaring back, leverage is at an 11-year high and compensation for these risks is the slimmest in three years.

“The market is long because it has loads of cash to deploy and fundamentals are quite strong,” said Vincent Benguigui, a portfolio manager at Federated Hermes, which oversees $625 billion. “It’s not a comfortable long though.”

That cash is on display in the size of the high-yield market: it just notched a record 461 billion euros ($550 billion), thanks to the pandemic-induced borrowing binge and a wave of fallen-angel downgrades of companies into junk. It’s dwarfed by some $1.5 trillion of speculative-grade bonds traded in the U.S., but has grown from zero in 1998.

Not everyone is dumping short positions. BlueBay Asset Management fund manager Geraud Charpin has been adding to bearish bets through credit indexes. “I think the market should be taking bigger short positions in fact,” Charpin said in an interview. “It misses a view.”

While he’s in the minority, even credit bulls are cautioning against running unhedged positions while pricing is so tight. Bank of America Corp. strategists advised clients to hedge credit portfolios at the start of June.

For now, there are few signs of stress. Default forecasts for high-yield companies remain low, with a 2% to 3% range expected in 2021 compared to 3.3% last year, yet that may change once central banks taper asset-purchase programs that kept shaky borrowers afloat during the pandemic.

Already, high-yield defaults in Europe have overtaken the U.S., according to S&P Global, and the gap is forecast to widen by the first quarter of 2022 with Europe’s default rates reaching 5.25%.

“The next downturn will hit the market much harder as we have more leverage in the system and higher chances of mass defaults due to inflation risks sending rates higher,” said Jochen Felsenheimer, managing director at XAIA Investment in Munich.

Europe

The European Union sent a Request for Proposal to banks for its second bond offering under its NextGenerationEU program to help fund the region’s recovery from the pandemic. Its first sale under the program -- a 20 billion euros offering on Tuesday -- amassed more than 142 billion euros of investor orders.

- The EU is also expected to unveil its green bond standard, a rulebook for the debt, later in the summer, with its first green bond sale coming as soon as September

- Five borrowers including Punch Taverns and Ceconomy are offering new bonds on Friday, boosting weekly issuance to around 50 billion euros

- Spreads across asset-backed securities in Europe should continue to grind tighter across most sectors, after reaching post-global financial crisis levels, according to Barclays analysts

Asia

Weekly sales of Asia-ex Japan dollar bonds slumped to the lowest in a month amid comments from Federal Reserve officials pointing to earlier-than-expected policy tightening.

- Issuance declined for a second week, to $2.8b from $5.2b a week earlier, according to Bloomberg-compiled data

- Spreads on Asia’s high-grade bonds, excluding Japan, are headed for a fourth straight week of tightening and the longest streak since March

U.S.

Activity in the U.S. primary market is likely to be largely subdued on Friday, with high-grade issuance for the week reaching $22 billion so far.

- Enbridge Inc. released a framework for the issuance of sustainability-linked bonds -- the first for a North American pipeline company -- as it pushes to improve its environmental credentials

©2021 Bloomberg L.P.