FOMO Overwhelms Stock Traders Who Have Begun Ignoring the Risks

Investors Are Chasing the Rally Into the Jaws of Economic Crisis

(Bloomberg) -- There hasn’t been much of a consensus on Wall Street lately but all of a sudden it looks like investors agree on two things: This rally has legs, and the economic crisis might be the worst in living memory.

That those two views can coexist speaks to the strength of this stock rebound and the mindset of traders conditioned by more than a decade of gains. Everyone knows tough times are ahead; no one wants to miss the buying opportunity of a lifetime.

All that means the S&P 500 could re-enter a bull market in one of the quickest times on record -- even as dismal news for the world’s largest economy piles up. Just hours ahead of the U.S. open, sentiment among small businesses collapsed by the most on record.

“Investors are torn between greed and fear,” said Daniel Murray, deputy chief investment officer at EFG Asset Management. “The risks are huge simply because we’ve never experienced anything like this before. But at the same time because markets have sold off so far and so quickly that means some high-quality assets have been dragged down.”

The market rebound lies in the coronavirus data over the past few days, which show rates of new deaths and infections apparently easing in several major economies.

After weeks of gloomy headlines it’s a welcome reprieve, but a prolonged economic shutdown is still needed to contain the outbreak -- and that has many market watchers fretting over how sustainable the rebound is.

“It makes sense that near-term catalysts like slowing hospital admissions or bending infection curves in Europe resulted in higher stock prices,” the equity team at Bespoke Investment Group LLC wrote in a note. “But that optimism has to be balanced against what could easily be additional outbreaks, re-outbreaks, and the lack of complete normalcy that will likely persist until a vaccine can be developed.”

The disconnects aren’t just between assets and economics. They’re cropping up within the market itself.

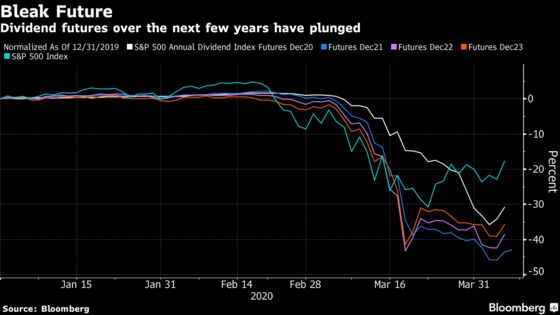

Dividend futures for the S&P 500 -- contracts tied to future shareholder payouts for the biggest U.S. companies -- have all plunged more than 27% so far this year across a range of tenors as the pandemic sweeps the country, forcing people into quarantine and shuttering businesses.

Yet thanks to its rally of the past few weeks, the S&P 500 itself is down only about 15% this year. Put simply, pessimism over growth currently looks a lot worse than the cash market for stocks is pricing.

Strikingly, during a surge for the S&P 500 on Monday, the leading stocks were those whose earnings estimates for 2021 had fallen the most, according to Bespoke. The analysts reckon this is in large part because those businesses were hit particularly hard and have seen their valuations crater along the way. Yesterday’s rally could therefore be dubbed a dash for the cheap stuff rather than something powered by economic conviction.

And those awful economic readings are piling up. The collapse in small business confidence follows data showing unemployment surging at an unprecedented rate and orders contracting at U.S. factories at the fastest since 2009.

For some, the divergence between equities and the economy is purely a function of the extraordinary response from policy and law makers to the crisis. The flood of dollars unleashed by the Federal Reserve floats all asset boats, while its Treasury buying suppresses rates volatility which has a knock-on effect into credit and then stocks.

“DM economic indicators continue to fall short of expectations, and government economic policies are causing quite a bit of noise,” Masanari Takada, a quantitative strategist at Nomura Holdings Inc., wrote in a note. “We therefore think a basic approach to short-term DM equity trading should view this as a mere spontaneous technical rebound.”

All the doubts mean much of the big money remains on the sidelines, potentially limiting this updraft. Takada argues it will be “some time” before macro hedge funds and long-term investors are persuaded to start buying again.

Read more: Blackstone’s Schwarzman Sees Virus Wiping $5 Trillion From GDP

That chimes with the response of smart-money investors surveyed by Evercore ISI. They found a distinctly bearish picture, with hedge funds net short across benchmarks as they prep for the S&P 500 to fall to as low as 2,000 by June amid the ongoing turmoil caused by the virus.

“Investors are starting to form a central case for the near/medium term economic outlook,” strategists led by Dennis Debusschere wrote in a note. “But the bearish case -- which most investors seem to agree with -- is the threat of virus rebound that continues to weigh on the outlook for growth and equities.”

©2020 Bloomberg L.P.