Inverted Yield Curve: Is It Time to Worry Yet?

Inverted Yield Curve: Is It Time to Worry Yet?

(Bloomberg) -- Last year, U.S. 10-year yields weren’t low enough to really boost the equity market’s appeal. This summer, the inversion of the yield curve is suddenly triggering worries of a U.S. recession, while bund yields are deep into negative territory as Germany seems heading for an economic downturn. Yet there’s few signs of panic among equity traders.

Many in the market agree that a U.S. recession isn’t imminent. UBS strategists see the inverted yield curve more as “a statement on lackluster growth in the rest of the world,” and suggest a slowdown would take some time to materialize.

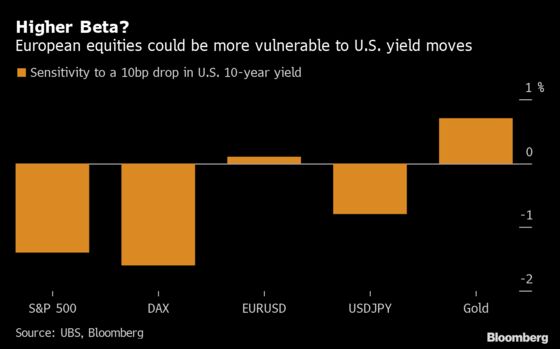

One interesting point they note is that European equities seem to have been more vulnerable than U.S. stocks to the gyration of the U.S. 10-year bond yield over the past six months.

The U.S. 10-year yield has only fallen below 1.6% on two previous occasions: mid-2012 and mid-2016. According to Citi strategist Jonathan Stubbs, it has worked well as a buy signal for European equities both times, with the DAX returning 23% on average over the next 12 months, the CAC 24%, and the FTSE 17%. Of course, with Fed cuts, ECB QE and trade concerns, things may be different this time, he says.

So, should we be worried? Not yet, according to JPMorgan strategists including Mislav Matejka. Over the past six historical episodes, yield-curve inversion preceded recessions by 17 months on average, while the equity market peaked about 11 months after the inversion, they write. Even if the risk of a downturn next year is increasing, much can happen in the meantime. They still expect equities to make all-time highs into the first half of 2020 and see the current pull-back not lasting beyond early September as the ECB will start quantitative easing and the second Fed rate cut might be bigger than the first.

The bounce in the U.S. 10-year yield over the past couple of days may have also provided some relief. Indeed, Bank of America technical analysts note that extreme momentum has pushed the monthly Relative Strength Index (RSI) of the U.S. 10- and 30-year bonds into their fourth and fifth-most overbought level ever. This may signal an imminent “key low” or “pivot low.”

And not all is bad about negative yields anyway. The more bond yields move deep into negative territory, the more stocks are seen by many as the only attractive asset. Why buy a bond on which you’re guaranteed to lose money while you can buy stocks with lofty dividend yields of 5% or more?

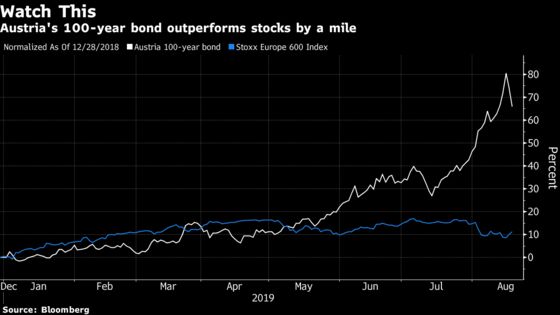

True, if held until maturity, government bond yields don’t look appealing. But on an absolute-return basis, some long-duration securities beat stocks. Notably this year, Austria’s 100-year note has delivered investors as much as an 80% return so far. Granted, the timing must be right and liquidity could be an issue.

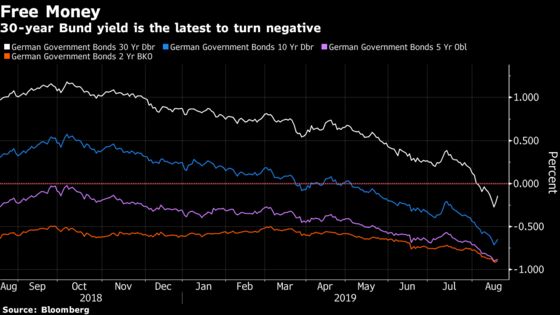

Finally, let’s not forget about another silver lining. With Germany facing the danger of a recession, the government has signaled it stands ready to inject stimulus if things turn sour. Since the bund curve has turned negative across all maturities, financing those fiscal measures in the long-term is even more appealing.

In the meantime, Euro Stoxx 50 futures are trading little changed ahead of the open, while S&P 500 contracts are up 0.2%.

- Watch the dollar after President Trump called for the Federal Reserve to cut rates by at least a full percentage point in order to weaken the U.S. currency. Fed Chairman Powell is expected to signal the potential for another cut on Friday, though some of his colleagues are not convinced.

- Watch the pound and U.K. stocks after U.K. Prime Minister Boris Johnson reiterated the country will be ready to leave the European Union without a deal by the current deadline at the end of October and is planning a September publicity blitz to prepare the public for a so-called hard Brexit. Meanwhile, the Labour party is gearing up for an election.

COMMENT:

- “The flattening of the yield curve was pretty extreme and not what we would naturally expect with the Fed cutting rates, as news should generally affect near-term pricing more than the pricing of bonds maturing in 2040," Emiel Van Den Heiligenberg, head of asset allocation at LGIM, writes in a note. "We therefore aren’t convinced the current situation is sustainable, as the more the curve flattens, the more vocal some members of the Federal Open Market Committee will be in calling for rapid rate cuts.”

NOTES FROM THE SELL SIDE:

- Peel Hunt initiates Playtech with an add rating, as the broker says that although the company is a “strategic muddle,” there is a will to sort out its issues which are “now exposed to daylight.”

- Jefferies says the biggest potential Brexit risks to the paper & pulp sector are goods-trade disruptions across U.K.-Europe borders as well as a potential macro slowdown next year in those markets. Mondi is seen as least exposed to U.K., SCA has the most U.K. sales exposure while DS Smith will see biggest FX sensitivity to earnings as a co. reporting in GBP with most profits coming from outside the U.K.

- European insurers have been surprisingly strong in the past 12 months but falling investment yields turns Bankhaus Lampe more cautious on the sector in a note downgrading its rating on Zurich to sell. Separately, Jefferies upgraded its rating on Zurich to buy.

COMPANY NEWS AND M&A:

- BHP Gives Investors Bonanza Returns And a Trade Spat Warning (1)

- BHP CEO Says Top Miner Can Still Profit In Any Global Downturn

- Bain, Carlyle Said to Weigh Raising Osram Bid to Counter AMS

- Casino Identifies New Asset Diposals Worth EU2b

- BNY Mellon, Societe Generale to Join German Cum-Ex Trial (1)

- Pandora Second Quarter Revenue 1.3% Above Estimates

- Basilea Narrows FY Operating Loss View, Midpoint Wider Than Est.

- Seadrill Ltd 2Q Adjusted Ebitda Beats Highest Est.

- South Korea May Fine Audi, Porsche over Alleged Emission-Rigging

- Coloplast Chairman Lars Rasmussen Sells Shares Using Options

- Ambea Second-Quarter Net Sales Beat Highest Estimate

- Anglo American Pledges $30m for Peru Projects to End Protests

- Greene King Banishes Brexit Blues With Some Help From Hong Kong

- Carige Calls Investor Meeting to Back $1 Billion Rescue Plan

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 374.5 (61.8% Fibo); ~386 (uptrend); 395.1 (July high)

- Support at 370.9 (200-DMA); 365.5 (50% Fibo, May low)

- RSI: 45.5

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at ~3,400 (uptrend) 3,403 (61.8% Fibo); 3,443 (50-DMA)

- Support at 3,249 (June/August low); 3,301 (200-DMA)

- RSI: 46.8

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Alstria Office upgraded to overweight at JPMorgan; PT 18 Euros

- Antofagasta upgraded to neutral at Goldman; PT 8.50 Pounds

- FLSmidth upgraded to overweight at JPMorgan; PT 360 Kroner

- Glencore upgraded to neutral at Goldman; PT 2.20 Pounds

- Humana upgraded to buy at Handelsbanken; PT 57 Kronor

- Zurich Ins. upgraded to buy at Jefferies; PT 380 Francs

DOWNGRADES:

- Continental cut to hold at Deutsche Bank; PT Set to 120 Euros

- Greene King cut to equal-weight at Morgan Stanley

- Metrovacesa downgraded to sell at Goldman; PT 8.12 Euros

- Proximus downgraded to sell at Goldman; PT 21 Euros

- Rentokil downgraded to sector perform at RBC; PT 4.70 Pounds

- Repsol downgraded to underweight at Barclays; PT 16 Euros

- Zurich Ins. downgraded to sell at Bankhaus Lampe

INITIATIONS:

- Addiko rated new buy at Goldman; PT 27 Euros

- Olvi Oyj rated new buy at SEB Equities; PT 41 Euros

- Playtech rated new add at Peel Hunt; PT 4.25 Pounds

- Stobart rated new outperform at Macquarie

MARKETS:

- MSCI Asia Pacific up 1%, Nikkei 225 up 0.5%

- S&P 500 up 1.2%, Dow up 1%, Nasdaq up 1.4%

- Euro up 0.05% at $1.1084

- Dollar Index down 0.01% at 98.34

- Yen up 0.11% at 106.52

- Brent up 0.1% at $59.8/bbl, WTI little changed at $56.2/bbl

- LME 3m Copper down 0.1% at $5768/MT

- Gold spot up 0.1% at $1497.4/oz

- US 10Yr yield down 2bps at 1.59%

ECONOMIC DATA (All times CET):

- 11am: (EC) June Construction Output MoM, prior -0.3%

- 11am: (EC) June Construction Output YoY, prior 2.0%

- 12pm: (UK) Aug. CBI Trends Total Orders, est. -25, prior -34

- 12pm: (UK) Aug. CBI Trends Selling Prices, prior 12

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.