Inflation Believers Playing Long Game Are Winning as They Wait

Inflation Believers Playing Long Game Are Winning as They Wait

(Bloomberg) -- Investors shuffling trades amid a sputtering reflation narrative may have overlooked a little fact: Bond managers who’ve been bullish on inflation prospects this year have been winning.

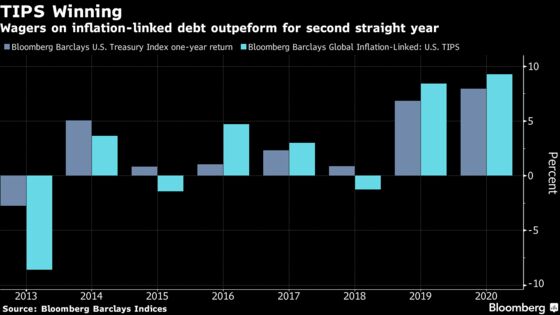

Inflation-linked U.S. Treasuries -- known as TIPS -- are on pace to outperform their regular counterparts for the second straight year, and some of the world’s biggest investors see scope for further gains. Vanguard Group Inc., which reaped profits on inflation-protected bonds it bought in March when the outlook was at its most dire, is looking for a re-entry point. And both BlackRock Inc. and Ardea Investment Management are wagering that the market is underestimating gains in consumer prices over the next few decades.

The triumph of TIPS is more than a little ironic, given the absence of a significant acceleration in inflation this year. Even after roaring back from an 11-year low when the pandemic shuttered the world in March, expectations for price pressures remain relatively tame. But with vaccine hopes now building, some investors see these securities as a cheap way to bet on a rejuvenated global economy. The added impetus is that this is a category of debt that typically offers outsized gains when yields are stable or falling.

“TIPS perform best in a modest growth and rising-inflation-expectations environment, which is right where we are now,” said Elaine Kan, who co-manages Loomis Sayles & Co.’s Inflation Protected Securities Fund. “And nominal yields aren’t likely to go much higher at least for the next few months, which is a positive for those investing in TIPS -- who also will benefit from the inflation protection if expectations go up more.”

No Bottom

The Federal Reserve somewhat put a floor under so-called nominal yields when signaling that it doesn’t want to push policy rates below zero, and may have limited the prospects for additional gains in Treasuries. Not so with TIPS, where yields can, and do, go negative; the 10-year U.S. maturity currently yields around minus 0.95%.

To be clear, that means investors are basically paying to hold this debt on the assumption they get a windfall as inflation rebounds -- not a strategy for everyone. But like nominal Treasuries, TIPS benefit from demand for havens, and the additional potential for yields to decline opens up the door to greater price appreciation.

BI Primer: Treasury Inflation-Protected Securities

Further adding to their appeal is the longer duration that these securities generally have compared to their nominal counterparts, meaning they tend to deliver larger price gains when rates are steady or declining as they are now. TIPS have proved a stellar bet this year, earning more than 9% compared with about 8% for regular Treasuries, according to Bloomberg Barclays index data.

The bond market’s main measure of inflation expectations -- dubbed the breakeven rate -- has bounced back to where it was at the start of 2020 thanks to the Fed’s ultra-loose policy and massive government stimulus. But doubts remain about the Fed’s ability to boost it further and achieve officials’ 2% target for annual growth in consumer prices. The breakeven rate is the CPI level needed over life of the security for the TIPS holders’ return to roughly match that of a nominal Treasury.

‘Asymmetric Opportunity’

For Ardea Investment, it boils down to a risk-reward tradeoff. Inflation may not be about to suddenly lurch higher, but the firm sees more bang for the buck in betting on an upside surprise when the market is so skewed toward inflation staying low for a long time.

This offers what Gopi Karunakaran, co-chief investment officer at Ardea, called an “asymmetric opportunity.” The limited supply of inflation bonds also helps, he said.

“One of the biggest themes over the past decade is that we’ve been entrenched for such a long time in this world of low inflation and low inflation expectations,” Karunakaran said. “Few people are prepared for that upside surprise.”

It’s hard to blame the naysayers, given how stubbornly low inflation levels have persisted for years in the world’s largest economy. The Fed’s preferred measure of inflation has been below its target for most of the last five years.

And even for inflation believers, TIPS have their drawbacks: They’ve only been around since 1997 and remain relatively illiquid versus nominals. TIPS were among the hardest-to-trade government securities when the pandemic roiled markets in March, in part because they account for just $1.5 trillion of the $20.4 trillion Treasuries universe and tend to be favored by long-term, buy-and-hold investors.

But the narrative around inflation debt may start to change should distribution of a vaccine begin, according to Mark Nash, head of fixed-income alternatives at Jupiter Asset Management.

“We are still into inflation bonds in a big way,” he said. “If you have a Q1 rollout for the vaccine, and central banks as well as governments staying generous with their policies, then boom, we’ll get some confidence back. These bonds will be a must-own when things clear up.”

Headwinds Abound

Not everyone shares that view. There are immediate headwinds to consider, with surging coronavirus cases spurring another round of lockdowns in many countries, millions of people still out of work and a range of pandemic-relief programs set to expire in the U.S.

For Jason Bloom, a global strategist at Invesco Advisers, the market is ahead of itself in expecting stronger growth right away.

“You likely wouldn’t start to see economic activity pick up to the point of generating inflation until we get into the end of 2022,” he said. “The vaccine news absolutely didn’t change anything regarding our inflation outlook.”

Winning Bets

Those investors who are convinced the stage is set for the next step in the economic recovery are sticking with their winning bets.

Gemma Wright-Casparius, a senior portfolio manager at Vanguard, which oversees about $6.2 trillion, scaled back TIPS wagers last quarter after the rebound in breakevens. She expects to add more ahead.

“We’re looking for opportunities to re-engage because we do think the vaccine is a game changer,” she said. “Depending on how widespread its adoption and durability is in terms of immunity, we could close the output gap faster than is now expected.”

Inflation expectations got a jolt this year from the Fed’s pledge to keep supporting the economy until inflation measures are consistent with an average of 2% over time. And with talks over additional fiscal stimulus stalled out, most see the Fed doing more, even as soon as December.

Bob Miller, head of Americas fundamental fixed income at BlackRock, which manages over $7 trillion as the world’s biggest asset manager, says the firm came into the year long TIPS, in the 5- to 10-year sector, and added more when the securities got crushed during the March-April period.

Miller helps oversee the Total Return Fund, which has gained around 8% this year to beat about 80% of its peers, according to data compiled by Bloomberg. He took profits on intermediate-maturity TIPS and is now long the 30-year security.

The 30-year breakeven at about 1.91% signals too much pessimism for Miller. That’s because TIPS are tied to consumer prices, and CPI has historically exceeded the inflation gauge the Fed targets by about 40 basis points. So the current breakeven rate implies the Fed will miss its 2% target by about half a percentage point on average over the next 30 years. As Miller sees it, such a big miss seems unlikely.

“I share some modest skepticism about the Fed’s ability to pin the tail on the donkey at 2% for a long period of time,” he said. “But I would not underestimate their willingness to try.”

©2020 Bloomberg L.P.