Indonesian Bonds Have What It Takes to Beat Southeast Asia Peers

Indonesian Bonds Have What It Takes to Beat Southeast Asia Peers

(Bloomberg) -- Follow Bloomberg on LINE messenger for all the business news and analysis you need.

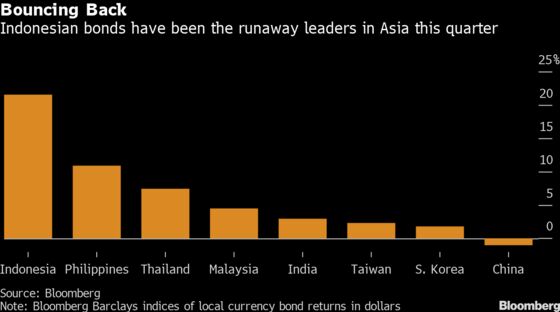

Indonesia’s bonds have been the star performers in Asia this quarter, and the second half of the year may bring further joy to investors.

Factors likely to support the debt of Southeast Asia’s largest economy include a pro-active central bank, and the apparent underweight positioning of global funds following the coronavirus sell-off. These should outweigh concerns about rising debt supply and a widening fiscal deficit.

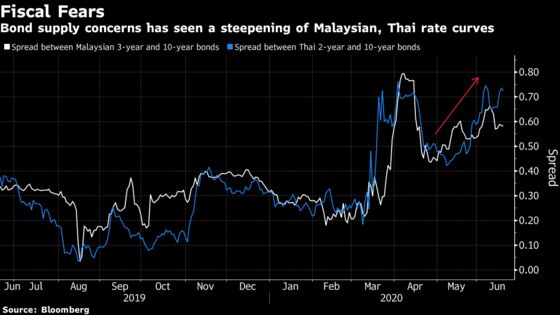

Elsewhere in the region, the rally in Philippine bonds may be approaching its end, given that the central bank has damped down speculation about further interest-rate cuts. Sovereign securities in Thailand and Malaysia may also find the going difficult as rising supply and policy makers’ reluctance to intervene heavily in the market will see yield curves continue to steepen.

Here is a quick run around the bases of Southeast Asia’s four-major debt markets as we approach the start of the second half:

Indonesia

The nation’s sovereign bonds have returned more than 20% since the start of April as investors bought risk assets amid signs the pandemic was being brought under control. Bank Indonesia has arguably been the most interventionist in the region, certainly the only one to announce direct bidding at government auctions. Liquidity-easing measures have also helped shore up demand from local investors at primary auctions, as was demonstrated by bidding at this month’s debt sales.

Foreign ownership of total government debt slumped during the virus sell-off and is currently only about 30%. This leaves plenty of upside as the level was as high as 39% in January. Any further improvement in the global outlook may spur a return of overseas funds, driving additional bond gains.

There are some negatives too. The government is boosting bond sales to finance a budget deficit that is expected to swell to 6.34% of gross domestic product this year, the widest in more than two decades. Bank Indonesia may even have to fund a larger portion of the virus stimulus, if some lawmakers have their way. At present though, demand from local funds appears sufficient to absorb the increased supply.

Philippines

Philippine bonds have been the region’s second-best performers this quarter despite the government warning that the fiscal deficit may expand to a record 9% of GDP. Returns have largely been driven by the central bank’s aggressive rate cuts -- 125 basis points already this year -- the most in the region.

The rally in bonds may be nearing its end though, given the diminishing appetite for further easing. Central bank Governor Benjamin Diokno said earlier this month he was “happy” with the current level of the benchmark rate.

While bond gains are likely to stall, the monetary authority’s proactive response to the crisis should put a floor under prices even as debt supply increases. Current regulations allow Bangko Sentral Ng Pilipinas to buy an additional 240 billion pesos ($4.8 billion) of bonds under a repurchase agreement with the Treasury, and there’s a prospect that threshold may even be increased. Traders have also noticed the BSP has been buying bonds in the secondary market.

Thailand

The Bank of Thailand seems to have avoided any heavy intervention in the government bond market in recent months, preferring instead to channel support via corporate debt. Policy makers introduced a $30.6 billion program in March under which commercial banks could buy high-quality money-market or fixed-income funds to use as collateral.

Without a step up in central bank intervention, there’s a risk that longer-maturity bond yields will rise further in the second half as bond supply accelerates. The spread between two- and 10-year yields has already jumped from a low of 18 basis points in March to more than 70 basis points. The prospect of another rate cut has also dimmed, with economists expecting the benchmark to stay at its current level through year-end.

Malaysia

Malaysian bonds rallied earlier this year when the central bank cut interest rates by a combined 100 basis points and introduced new measures to boost liquidity. The market is currently under pressure, however, after the government widened its 2020 fiscal deficit target again, this time to 5.8% to 6% of GDP.

The spread between Malaysia’s benchmark 10-year bond and the policy rate is approaching the highs seen at the peak of the virus turmoil in March. Unless Bank Negara Malaysia takes further measures or actively intervenes, bond yields may climb further in the second half.

Political turmoil may add an extra level of uncertainty, and the threat of a potential downgrade. Rating agencies may look to reappraise the nation if the new government calls a snap election in an attempt to counter claims it doesn’t command a parliamentary majority.

What to Watch

- Bank of Thailand meets Wednesday with swap rates suggesting policy will stay on hold. Traders will be waiting to see if the central bank announces any measures to restrain baht gains following its recent comments. Thailand will also release trade data on the same day

- The Philippine government will auction five-year bonds on Tuesday, while the central bank will review policy on Thursday

- Malaysia will release headline inflation data on Wednesday after reporting a decline in prices for the two previous months

©2020 Bloomberg L.P.