In Trade War Worst-Case Scenario, These Strategies Can Win

In Trade War Worst-Case Scenario, These Strategies Can Prosper

(Bloomberg) -- State Street Global Markets likes the dollar. Mizuho Bank Ltd. says buy Treasuries and go short on South Korea and Taiwan. Deutsche Bank AG reckons the yuan may weaken.

These are some of the investment ideas strategists and money managers are favoring in case U.S.-China negotiations break down and the trade war spills over to next year. The odds of a deal have been fading in recent weeks, with President Donald Trump threatening to raise tariffs on $300 billion of Chinese goods, and China’s government saying it will “fight to the end.”

“We’d be surprised” if there’s a deal at the end of the month, Adam Margolis, head of South Asia FX advisory at Citi Private Bank in Singapore, said of Trump’s potential meeting with China President Xi Jinping at June’s Group-of-20 summit. “Some of the differences between the two sides are clearly hard to mend.”

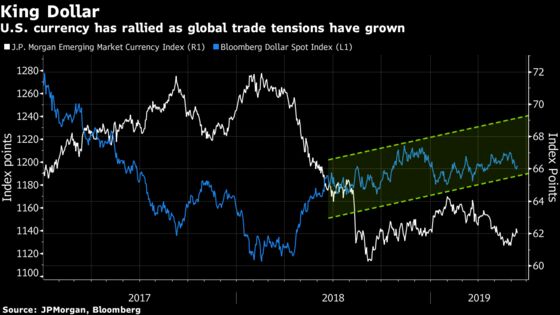

Rising tensions between the world’s two-largest economies over recent months have boosted the dollar and U.S. Treasuries. The Bloomberg Dollar Spot Index touched a five-month high at the end of May, while U.S. 10-year yields have plummeted to the lowest levels since 2017. Traders are betting global trade frictions will help convince the Federal Reserve to cut interest rates.

Citi’s Margolis, who advises investors that control a minimum of $10 million, is expecting currency volatility to spike as optimism Trump clinching a working trade deal with Xi at the G-20 summit wanes. He’s been advising private wealth clients, who tend to be short currency volatility, to reconsider their positions.

Here’s what other market participants are saying:

Deutsche Bank (Falling yuan)

“The nature of the breakdown in talks is severe enough that the hurdle to patch up is also likely to be correspondingly high,” said Sameer Goel, head of Asia macro strategy in Singapore.

“I can see the yuan breaking seven per dollar even in a scenario where there is not necessarily a constructive deal. Seven is not the red line for Chinese authorities the markets believe it to be.”

“If easier financial conditions are required as a policy response in a bad case scenario, then the authorities would be willing to let that happen –- but they would want to manage it, no government wants a disorderly depreciation.”

State Street Global Markets (Prefer the dollar)

Dwyfor Evans, head of APAC macro strategy, is overweight the dollar and expects regional currencies to weaken if trade frictions persist.

“The role of the onshore yuan here is crucial, as correlations between the yuan and regional currencies have risen in recent years. That said, the Chinese authorities will be determined to ensure that the yuan is not a one-way move, and there are limits to its tolerance on weakness. We are not convinced that Beijing would encourage yuan through 7, for example.”

Unigestion SA (Greenback haven)

“We believe that the risk of further escalation is now significantly higher and the impact of this is worrying,” said Jeremy Gatto, portfolio manager of the Multi-Asset Navigator Fund in Geneva. “Under such a scenario, heightened market stress will prevail and the USD will be the safe haven currency of choice.”

“We believe an underweight in Asian currencies -- to the exception of the JPY -- is warranted until we witness a clear improvement in trade war negotiations or a material shift from a macro perspective which is unlikely at this stage.”

Western Asset Management Co. (Favor Asia bonds)

“It remains highly plausible that if economic dynamics do not shift materially, the U.S. dollar will maintain its strength,” said Desmond Soon, head of investment management for Asia ex-Japan. “China, Korea and to a lesser extent, Japan, will likely be adversely affected by the escalation of Trump administration’s trade tariffs.”

Western favors India and Indonesia government bonds, because with elections in both countries over “and political continuity secured, we are constructive about their domestic fixed income, which have high attractive yields.”

Mizuho Bank (Treasuries bull)

“Piling into the two-year part of the Treasuries curve is an easy but crowded trade,” said Vishnu Varathan, head of economics and strategy at Mizuho Bank in Singapore. “Bucking it too early would be tempting pain thresholds though, especially if the trade war gets worse.”

“I’d also be looking to short the likes of Korea and Taiwan -- countries that are sensitive to global trade and suffer in broad risk-off moves in markets.”

To contact the reporter on this story: Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Joanna Ossinger, Nicholas Reynolds

©2019 Bloomberg L.P.