Central Bank Is Offering a ‘Passive Put’ to India Bond Traders

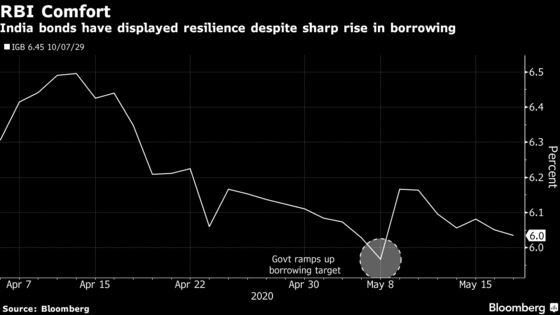

India’s benchmark bond yield has fallen back to levels seen before the administration ramped up its annual borrowing target.

(Bloomberg) -- India’s benchmark bond yield has fallen back to levels seen before the administration ramped up its annual borrowing target by more than half, as investors bet that the nation’s central bank has more tricks up its sleeve.

Apart from a 40 basis point cut in interest rates on May 22 -- one that didn’t leave markets too enthused -- the Reserve Bank of India hasn’t actively intervened to tamp down yields since the enhanced 12-trillion rupee borrowing was unveiled May 8. It hasn’t made any purchases of primary or secondary market debt or launched more of Operation Twist, where it buys long-end bonds while simultaneously selling short-term notes.

Yet, the most-traded 6.45% 2029 bond yield has drifted back and was trading at 6.03% on Thursday after briefly rising by the most in three years in reaction to the new borrowing. It was at 5.97% before the higher borrowing was announced.

“One can argue that the RBI understands it has to play a long game,” Suyash Choudhary, head of fixed income at IDFC Asset Management Ltd., wrote in a note. “What it is offering to the market is in the nature of a passive put.”

Bond investors must stop expecting the central bank to play an active role at pulling down yields, according to the note. The RBI may opt for extending passive support that still puts a lid on yields while providing incentives to buy debt by keeping overnight rates very low and liquidity abundant, Choudhary wrote.

Bank of America expects the RBI to make $88.5 billion of bond purchases, while several other economists have said that the central bank could end up buying government debt directly.

The RBI may well be keeping its gunpowder dry as it sees itself continuing to do the heavy lifting in supporting an economy that’s set for its first full year of contraction in four decades.

“There’s very strong expectation in the market that eventually a large part of the supply, whether it is coming from the central or state governments, will get absorbed by RBI,” Neeraj Gambhir, president and head of treasury and markets at Axis Bank Ltd. told Bloomberg Quint.

©2020 Bloomberg L.P.